An abundance of cash in US funding markets appears to be driven by deeper structural shifts that are unlocking billions of dollars in balance-sheet capacity at the biggest banks, Wall Street strategists say.

Some $120 billion have poured into money market funds this month alone, adding to a buildup in liquidity in recent weeks. It’s a reversal of fortunes from last year’s funding strains that sent ultra-short term interest rates soaring and forced the Federal Reserve to end its portfolio runoff.

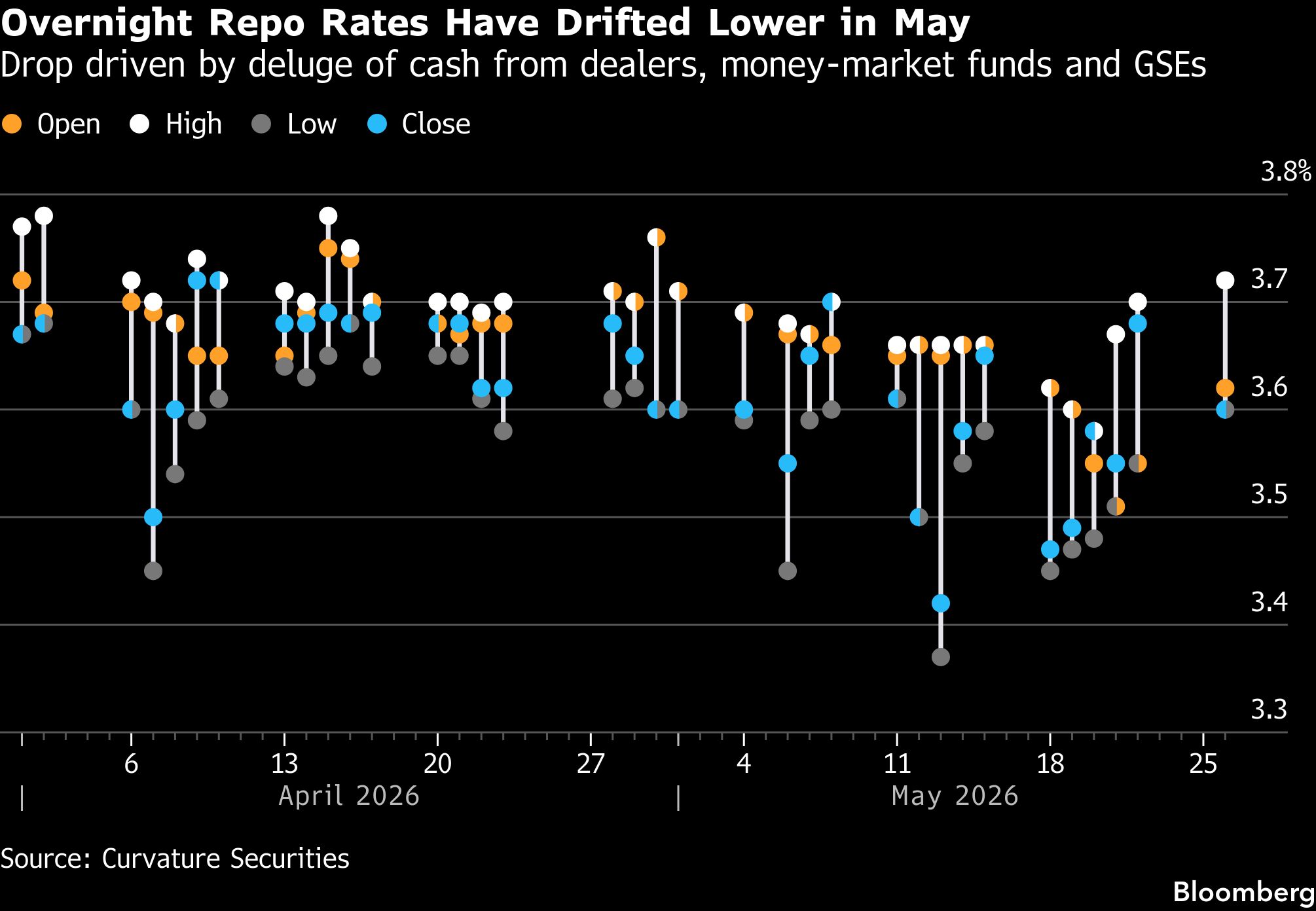

The flow of money has pushed rates in the market for repurchase agreements, where cash is borrowed and lent overnight against Treasuries, below the bottom of the Fed’s target range for its policy benchmark.

The effective federal funds rate, the central bank’s benchmark which rarely moves between policy meetings, has dropped twice in the past month. Meanwhile, the Secured Overnight Financing Rate, which is based on the cost of borrowing against Treasury securities, is just above 3.50% after averaging around 3.65% in April.

Strategists from Barclays PLC, RBC Capital Markets, and Bank of America Corp. say the softness in the market has gone well beyond the usual seasonal drivers, turning into something more durable.

“I don’t think there is a single ‘smoking gun’ and that this continues to be a perfect ‘anti-storm’ of multiple calming factors coming together in the same direction,” said Blake Gwinn, head of US interest rate strategy at RBC.

A persistent drop in funding rates changes how liquidity moves through the financial system. Softer conditions free up cash during periods of high demand, which can shape the Fed’s balance-sheet decisions, influence Treasury’s short-term debt issuance and give banks more room to deploy money rather than sit on reserves at the central bank.

The cash is coming from a variety of sources ranging from the central bank’s monthly Treasury bill purchases launched at the beginning of the year to the relaxation of financial crisis-era rules that freed up capital after taking effect last month.

Seasonal forces have added fuel, too: the reduction of Treasury bill supply by more than $270 billion around the April tax season and Treasury’s cash‑management buybacks contributed to an imbalance between cash and collateral.

Gwinn said recent changes to the enhanced supplementary leverage ratio have helped remove a constraint that would have tightened conditions over time.

The tweak — which expanded how much cash major lenders can intermediate in the Treasuries market during times of stress — should be seen as a “loosening of the handcuffs,” making it easier for dealers to absorb flows and hold larger Treasury inventories as balance sheets expand, he said.

Banks were allowed to adopt the rule change even before the April 1 deadline, helping ease conditions even as dealer holdings of Treasuries peaked at an all-time high of $557 billion at the end of March.

Wells Fargo & Co.’s expansion has also enhanced liquidity. Since the lifting of its asset cap in June 2025, the bank has become one of the largest marginal providers of repo financing, adding tens of billions in balance‑sheet capacity and stepping into flows that previously would have strained the system. Strategists say its increased presence has been a major factor in keeping conditions benign.

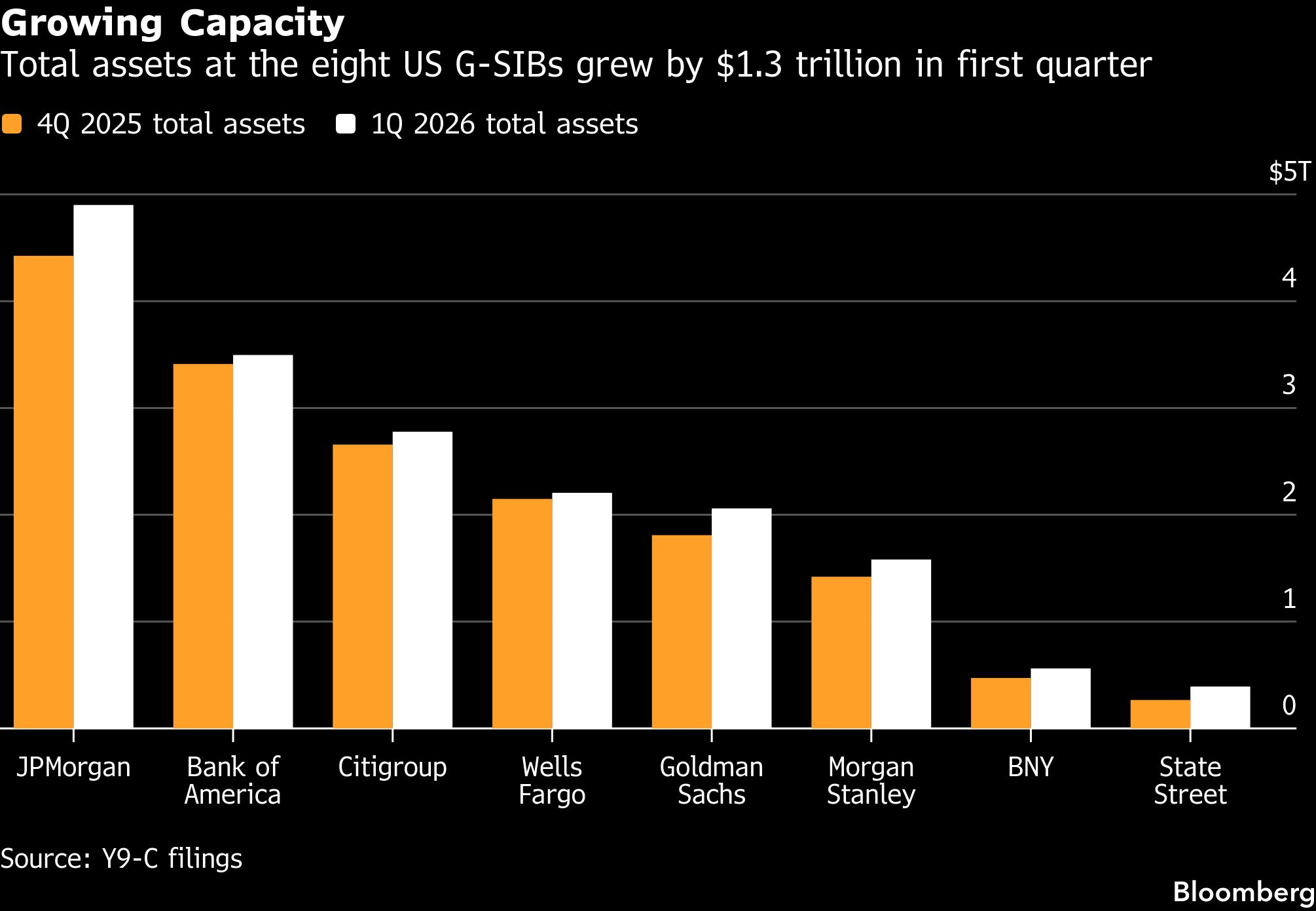

In the first quarter, total assets of the eight global systemically important banks based in the US swelled by a combined $1.3 trillion, $300 billion of which was in reverse repo transactions, according to filings. Securities holdings rose by about $400 billion, including $100 billion in Treasury trading books, according to Barclays.

“Taken together, this points to a meaningful expansion in intermediation capacity across cash and repo markets, the outcome regulators were aiming for in relaxing the SLR requirement,” Barclays strategist Samuel Earl wrote in a note.

One immediate implication could be a pause in the Fed’s monthly bill purchases. The New York Fed’s Roberto Perli said last week that reserve management purchases could be adjusted depending on market conditions.

Earlier this month, Fed officials announced they would further slow the monthly pace of their Treasury bills purchases to about $10 billion, gradually reducing them from $40 billion through April and $25 billion in May.

A pause “could certainly be on the table if funding conditions remain very loose, but at $10 billion a month the pace is already extremely slow,” said Gennadiy Goldberg, head of US interest rate strategy at TD Securities.

While some repo rates have begun to normalize this week after Treasury auction settlements and the removal of monthly cash from government sponsored enterprises, traders expect easing to continue.

Even after an increase in bill issuance this month, trading desks say that the cash-collateral imbalance has persisted. Dealers at a trading desk flush with cash were willing to do transactions even as rates briefly dropped to as low as 3.40%, according to Tradition Securities.

Federal Home Loan Banks, which are the biggest lenders in the fed funds market, are likely to continue to invest a rolling amount of cash into the market taking advantage of attractive rates and adding to liquidity, according to Bank of America.

“Our guess at this point is that market conditions will keep the trading range for overnight repo rates somewhat below their Q1 equilibrium,” said Wrightson ICAP economist Lou Crandall.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.