This month’s rally in the dollar, as traders priced in the prospect of higher US interest rates, is leaving Wall Street strategists wary of further gains.

The Bloomberg Dollar Spot Index is up 0.7% so far in May, as investors ramped up bets that the Federal Reserve will raise rates by early 2027, boosting the appeal of US assets. The gauge is on track for only its fourth monthly gain since the greenback’s 2025 downtrend began.

To strategists from Morgan Stanley to Wells Fargo, focus is now shifting to the likelihood that other major central banks will hike even more aggressively, just as optimism for a US-Iran peace deal dents the US currency’s haven demand. The consensus view on Wall Street is for a key gauge of the dollar to tumble more than 1% by the third quarter and 2% by the fourth, according to forecaster data compiled by Bloomberg.

“We are not chasing the dollar rally right now,” said Erik Nelson, a macro strategist at Wells Fargo Securities LLC in New York. “US exceptionalism might have reached another peak and that will limit the dollar’s ability to follow through and break well-established ranges.”

Nelson expects the crowded positions in American AI/semiconductor stocks to “expose the dollar to fresh downside risks.”

The Bloomberg gauge of the dollar has failed to close above its 200-day moving average since April — around the time US President Donald Trump announced a ceasefire with Iran. The moving average has capped the dollar’s upside for more than a year, with the gauge briefly trading above the key level in March during the height of the Middle East conflict before retreating.

American outperformance versus the rest of the world, in terms of economic growth and equity market gains, has reached “rather extreme levels” and is prone to a correction, according to Nelson. Aside from the 2020-21 pandemic, the real gap in gross domestic product between US and its 10 major peers on a weighted average basis has not been this big in a quarter century, he said.

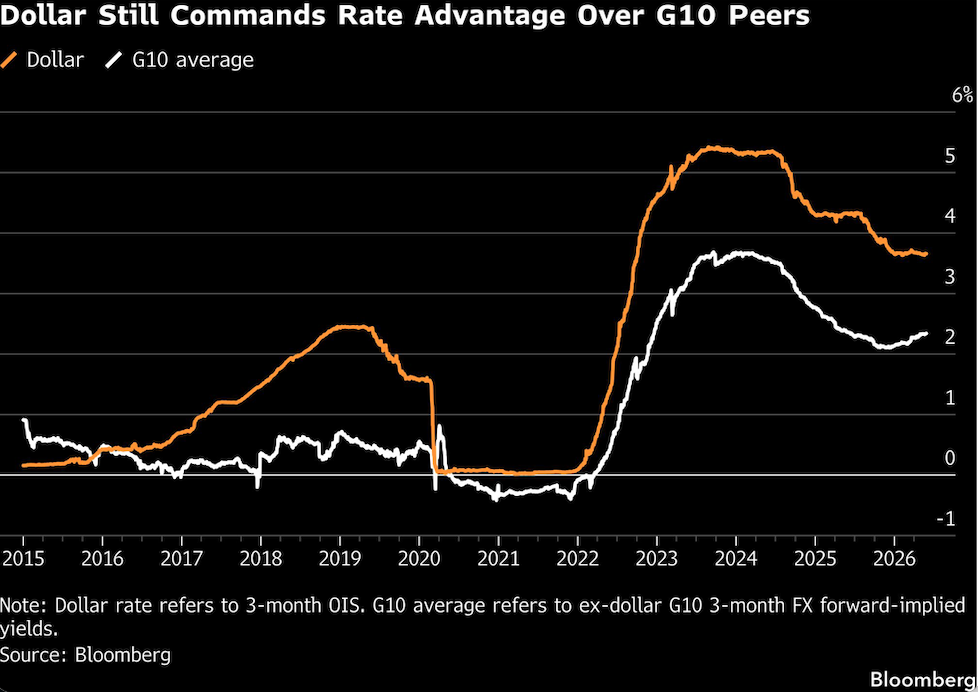

Meanwhile, a narrowing gap in rate differentials between the US and the rest of the world will likely support major currencies versus the greenback. The European Central Bank and Bank of Japan are expected to hike closer to the federal-funds rate in the coming months, continuing the trend of convergence between the US and rest of the world, according to Matthew Hornbach, Morgan Stanley’s global head of macro strategy.

“The macro backdrop supports a softer dollar,” he said.

Options markets suggest traders remain undecided on the near-term outlook, while longer-dated contracts still demand a premium to hedge further gains.

Financial markets are pricing about 30 basis points of Fed hikes by March 2027, compared with 60 basis points for the ECB and about 40 basis points for the Bank of England. Swaps signal a BOJ rate increase of 40 basis points by the year-end.

“The market isn’t confident the Fed could out-hawk other central banks like it did in the post-pandemic hiking cycle that started in late 2021 and mostly ended by 2023,” said Howard Du, a currency strategist at TD Securities USA, which maintains its bearish dollar bias.

What Bloomberg’s Strategists Say...

It is only a matter of time before stubborn dollar bulls capitulate and give in to what seems to be a very high bar for restoring a broad USD advance. Especially with a seasonally weak period approaching. Over the past two decades the June-July period has been a consistent source of pain for USD longs.

— Mark Cranfield, MLIV macro strategist

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by George Lei