Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

When currencies are printed without limit, the role of gold becomes simple: Protect purchasing power. The challenge is that most investors do not fully grasp what that means. A simple illustration helps.

Imagine a closed system with 100 individuals and 100 apples. Each person also holds one gold coin and one dollar, each of which has the same value: Each coin or dollar can buy a single apple. Now, magically, double the number of dollars. At first, everyone feels richer, but nothing real has changed. There are still only 100 apples.

Over time, due to this printing of dollars, behavior adjusts and prices rise. An apple that once cost one dollar now costs two. Wealth was not created. The value of each dollar was simply reduced. The gold coin, unchanged in supply, can still only buy a single apple — but is now worth two dollars. Gold maintains its purchasing power while the dollar has deteriorated in value. This is what gold is signaling today.

The Flaw in Measuring Wealth

Most investors measure their wealth in dollars, which is a flawed metric. A dollar is not a fixed unit of measurement; it changes over time. The data is clear: The U.S. money supply has grown from roughly $5.5 trillion in 2002 to $11 trillion in 2014, and now exceeds $22 trillion. It has doubled roughly every decade. The more dollars in existence, the less those dollars are worth over time. Yet portfolios, financial plans, and perceptions of wealth are still anchored to that moving target.

The Illusion of Growth

If a portfolio grows from $1 million to $2 million, it appears to have doubled. But if purchasing power has declined, the reality is very different. The true growth may be far less meaningful than it seems.

Official inflation measures suggest modest annual increases in the 2% to 3% range. But tracking money supply points elsewhere. The value of our dollars degrades by the annual increase in the money supply, roughly 6% each year.

What Gold Actually Does

Gold is often misunderstood. It is not a growth asset, and it produces no cash flow. Its role is to maintain purchasing power — not outperform. It reflects the currency’s declining value.

Has Gold Gone Up Too Much?

Gold’s recent strength raises a natural question: Has it gone too far? In the short term, perhaps. At roughly $4,500 an ounce, it is fair to ask whether gold has temporarily exceeded its role as a store of value.

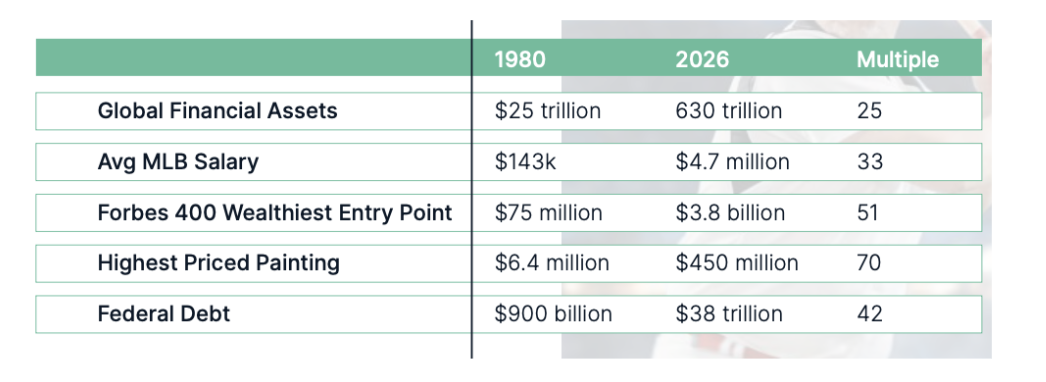

Gold moves in cycles. Sharp advances can lead to periods of consolidation. That is normal. Specifically, the near-vertical rise in gold in the last year or two does give us pause. But zooming out tells a different story. Since 1980, financial assets have increased more than 25x, federal debt has increased more than 40x, and wealth thresholds have expanded dramatically.

Gold’s rise, while significant, has not exceeded the broader expansion of the financial system. Even at roughly $4,500 an ounce, gold lags many other assets in dollar terms.

The Bigger Driver: Policy, Not Price

The long-term case for gold is about structure, not momentum. Federal debt levels continue to rise, and the path of least resistance is for policymakers to debase our currency, which means paying off obligations over time with cheaper dollars. Gradual, persistent expansion of the money supply lowers the real burden of debt over time. Gold functions as the counterweight to that process. It is, effectively, the inverse of currency stability.

The Role of Gold in a Portfolio

Gold is often criticized for its modest return expectations. That criticism misses the point: Its role is to preserve wealth, not create it. Gold serves as insurance against dollar debasement, helping offset the erosion of purchasing power.

If purchasing power declines by 2% to 3% annually, in line with reported inflation, gold should roughly match that. If the dollar’s purchasing power declines closer to 5% to 6%, in line with the growth in our money supply, gold should reflect that instead. It is not a growth engine; it is a stabilizer. That creates a paradox. If gold performs poorly, it suggests currency stability. If it performs well, it often signals underlying stress.

Gold Is Not the Signal of the Problem. It Is the Response to It

Despite recent performance, many investors — particularly in Western markets — remain underexposed to gold. If sentiment shifts from one of seeking growth towards one of capital preservation, investors may flock to gold. That shift in sentiment may have begun.

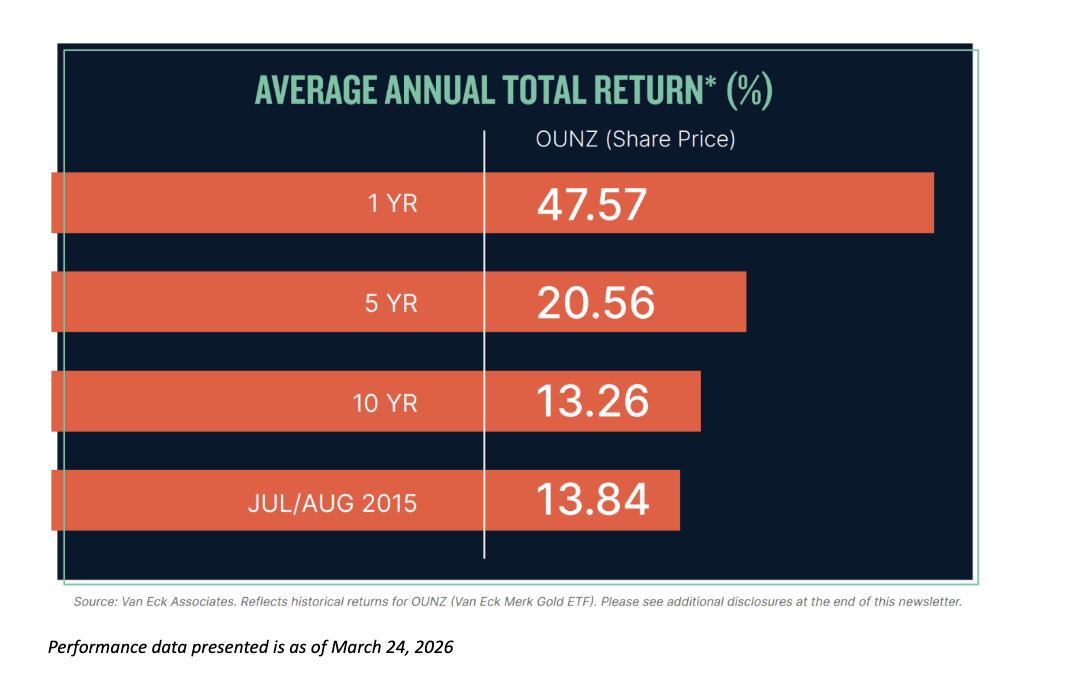

Gold is not simply moving higher. It is reflecting something deeper: The expansion of money supply, the erosion of purchasing power, and the long-term consequences of policy decisions. It does not change that reality; it makes it visible.The views expressed are those of the author and should not be relied upon for investment advice. Performance data presented is as of March 24, 2026. Past performance is no guarantee of future results. Clients of Morton Wealth may hold positions in gold or related securities.

Jeff Sarti is the chief executive officer of Morton Wealth. Morton Wealth is a Southern California-based investment advisory firm managing over $3 billion in assets as of May 31, 2026.. With a commitment to providing independent, thoughtful advice, Morton Wealth helps clients build wealth and create resilient financial plans tailored to their individual goals.

Sarti authors a quarterly newsletter series titled “The Healthy Skeptic,” which explores his perspectives on why challenging the status quo is crucial when navigating the financial markets.

More Closed End Funds Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.