Gold’s Bull Market Has Ended and Now All Eyes Are on Bears

Membership required

Membership is now required to use this feature. To learn more:

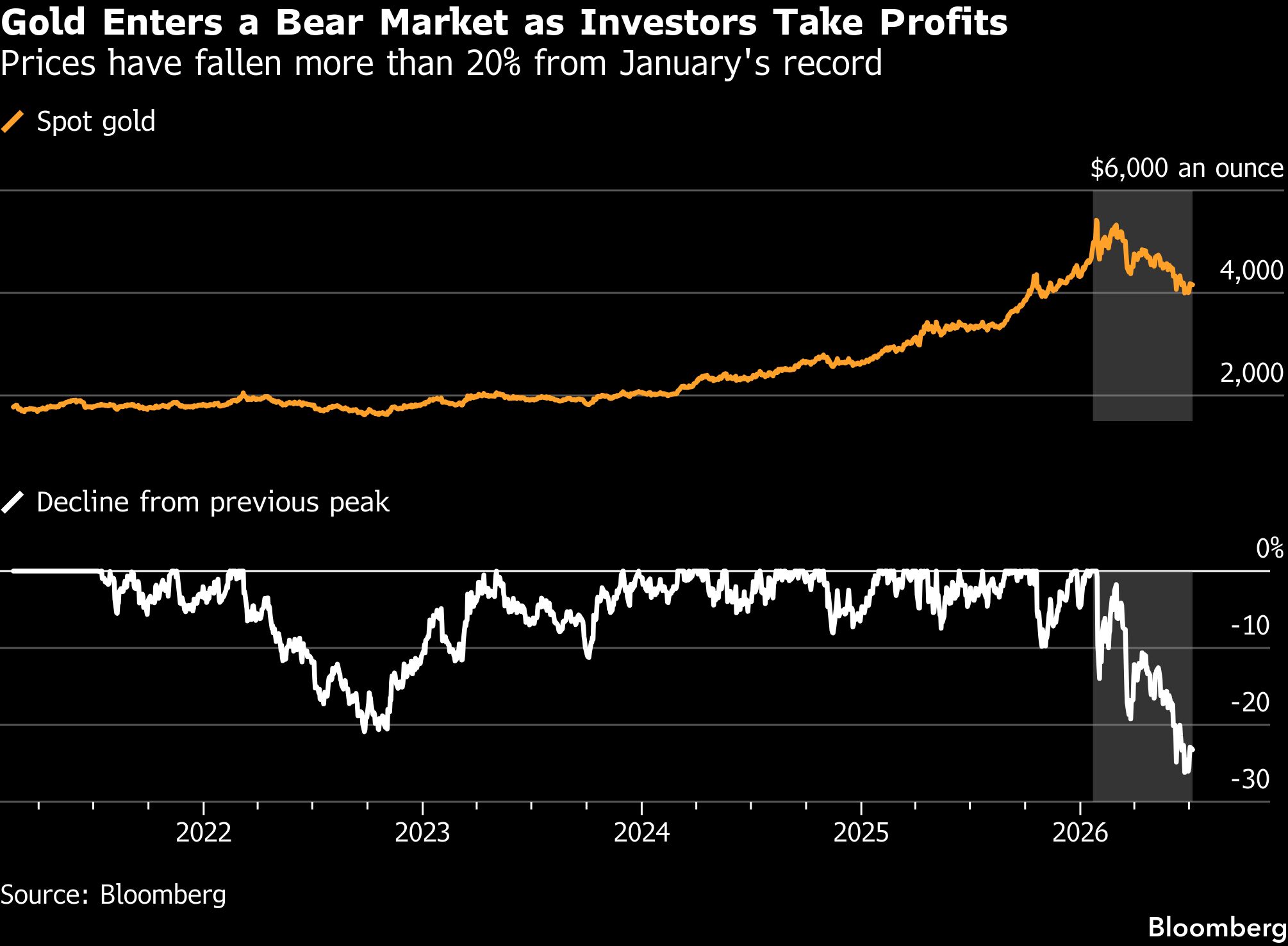

View Membership BenefitsA wave of profit taking in the gold market has brought a three-year bull run to an end, but there’s little evidence yet that investors are putting on large-scale short positions in anticipation of further declines.

Investors have pulled nearly $18 billion of gold out of exchange-traded funds tracked by Bloomberg since prices topped out at all-time highs near $5,600 an ounce in January. The exodus helped to precipitate a rout that pushed gold into a bear market last month, with prices breaching $4,000 an ounce on multiple occasions.

The outflows were part of a broader unwind of bullish positioning that’s also sent a chill through futures markets and retail bazaars from Shanghai to New York. Bulls have pulled huge sums off the table, and while many are still optimistic about gold’s longer-term outlook, they’re on watch for a further deterioration in sentiment that could drive prices even lower.

From the fleet-footed traders who dominate New York’s futures market to the central bankers whose steady purchases underpinned gold’s record-breaking rally, these are the investors to watch for signs that a more decisively bearish mood is taking hold.

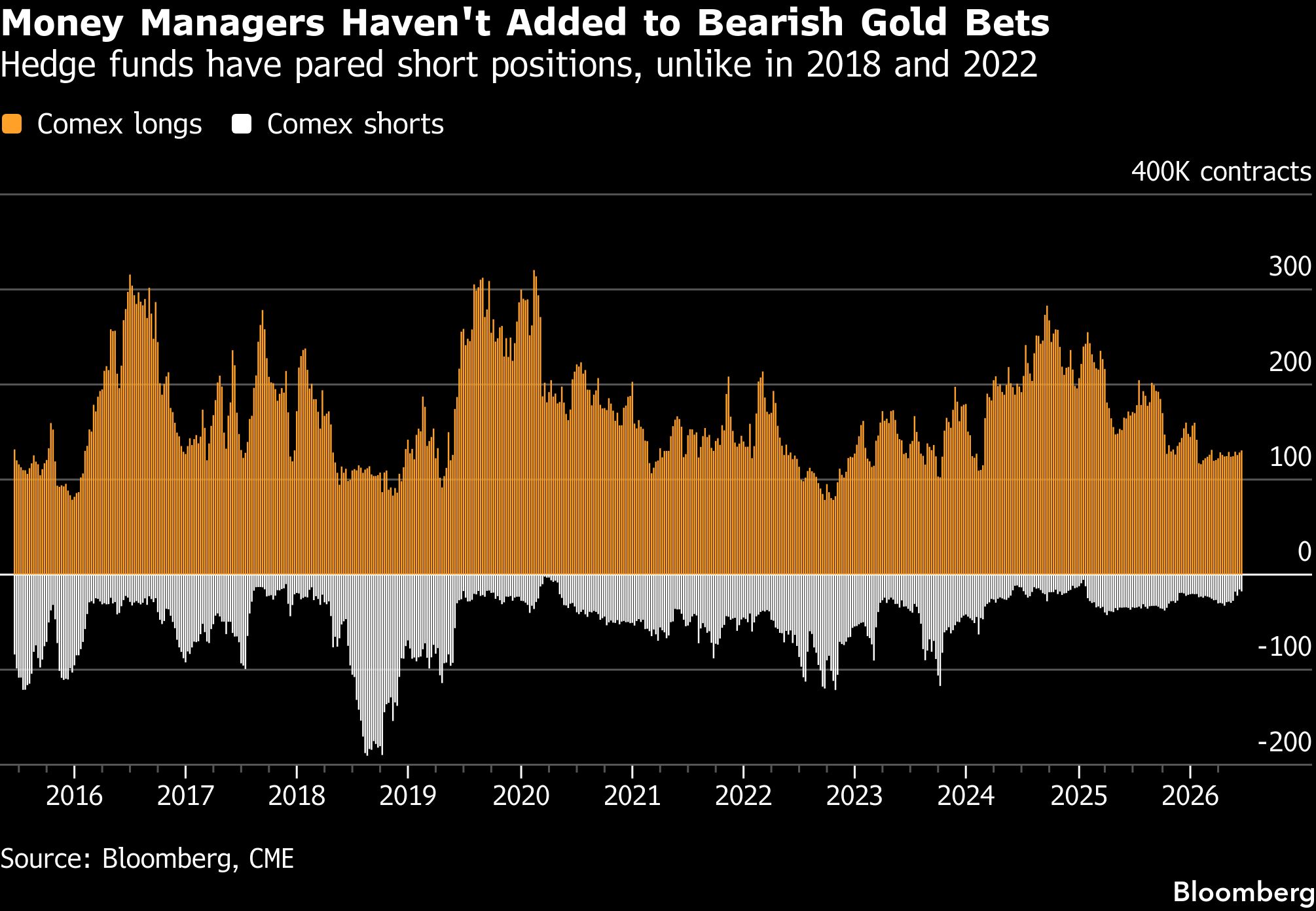

Money Managers

Investor flows in some corners of the market are hard to track, including the over-the-counter bullion-trading hub in London that’s the epicenter of the global industry.

But in New York’s futures market — where funds’ holdings are reported to regulators — bearish positions held by money managers are still hovering near historic lows. The selling pressure that’s pushed prices lower has instead come from an unwinding of bullish positions, trading data indicate.

That leaves room for fast-moving quantitative funds and other speculative investors to add short positions if the macro backdrop worsens, particularly if the dollar and yields stay elevated or inflation keeps the Federal Reserve hawkish, said Bart Melek, head of commodity strategy at TD Securities.

Much of the trading in New York is dominated by short-term investors known as commodity-trading advisors, which tend to trade based on technical dynamics rather than fundamental factors like supply and demand. Analysis by TD shows they’ve been taking profits on long positions over much of the past year, but on a net basis have only turned bearish to a marginal degree over the past few weeks, Melek said.

“Most of gold’s correction seems to be long liquidations as opposed to people taking on short exposure,” he said. “At this point, we just don’t have a lot of shorts in there. So there’s a lot of room to expand, and still a lot of room to cut long exposure.”

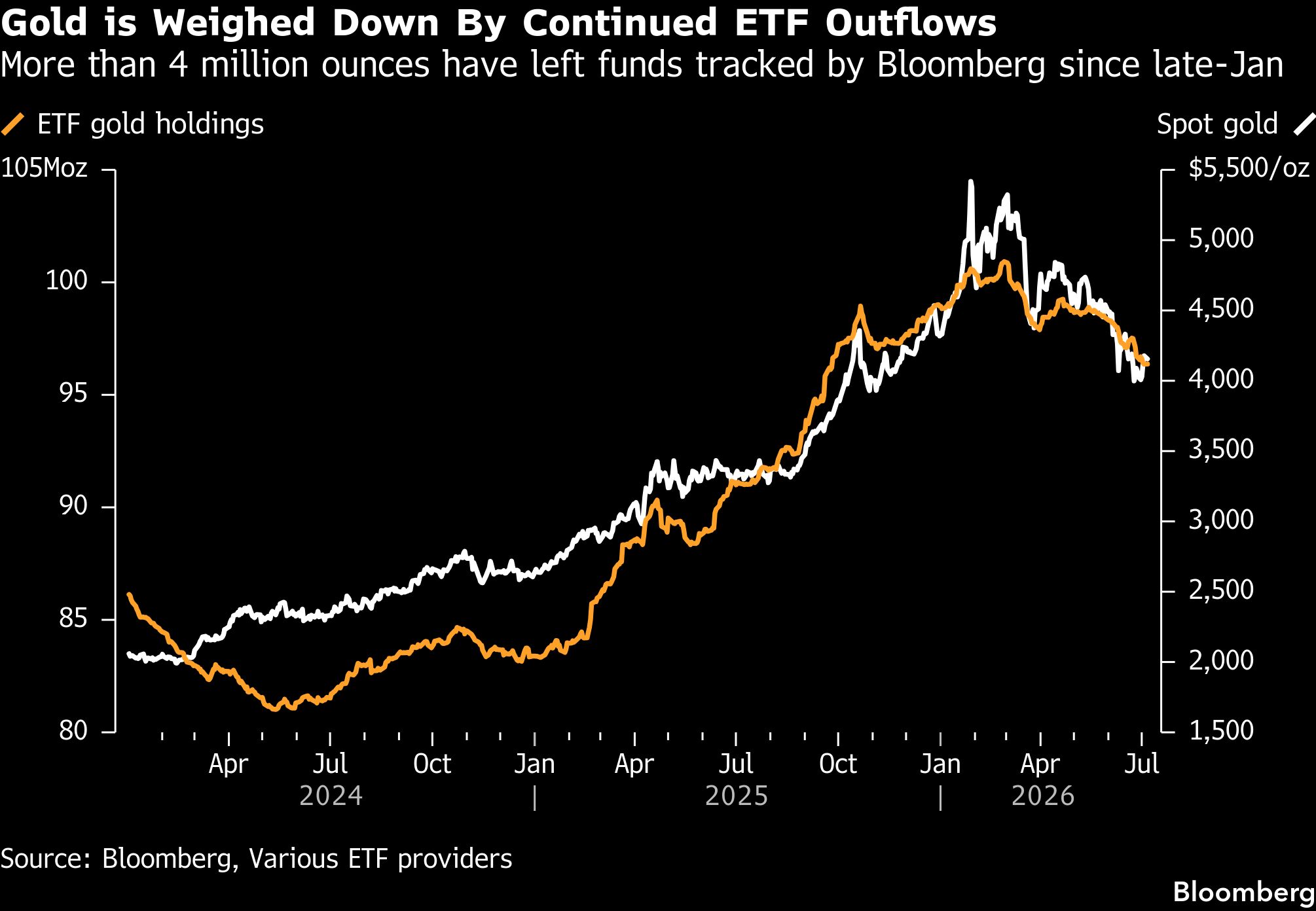

ETF Investors

For both retail and institutional investors, bullion-backed exchange-traded funds are among the most popular ways to gain exposure to gold. Inflows and outflows serve as a key barometer of gold’s appeal relative to other assets as conditions shift in financial markets and the broader economy.

Since the outbreak of the war in Iran, a wave of selling by ETF investors has weighed heavily on prices, helping to fuel the biggest monthly slump in nearly two decades over June.

While gold typically fares well during periods of geopolitical turbulence, the surge in oil prices caused by the conflict has been of greater concern, with the withdrawals from ETFs accelerating as investors braced for rate hikes that would dent gold’s appeal relative to yield-bearing assets like Treasuries.

ETF investors tend to be particularly sensitive to shifts in borrowing costs, and they’ve become the “marginal pricing power in gold” as other sources of demand have gone quiet, analysts at JPMorgan said in a note.

The bank now sees about 50 tons of outflows from global gold ETFs this year, a stark reduction from the roughly 400 tons of inflows it had expected in prior forecasts. While it retains a bullish long-term outlook, analysts led by Greg Shearer say “the macro/rates setup will likely continue to cap gold in a lower range over the coming quarters.”

Central Banks

Central-bank demand was a key driver of gold’s years-long rally, but in the early days of the Iran war, sentiment in the gold market took a hit as it emerged that central banks including Turkey, Russia and Azerbaijan had offloaded metal.

That forced investors to confront the prospect of a broader wave of central bank selling. However, recent industry estimates show that central banks as a whole actually upped their pace of buying in the first quarter. Survey data indicate they intend to buy more.

The People’s Bank of China in particular has continued buying throughout the selloff. The central bank, one of the largest sovereign buyers, has bought gold for 20 consecutive months, with disclosed acquisitions reaching the fastest pace since 2023 in June.

“I generally see consistency in how central banks are thinking about gold reserves,” said Chris Louney, commodities strategist with Royal Bank of Canada. “If you’re trying to de-dollarize and diversify, gold stands out as that long term reserve asset that’s already a part of the global monetary system.”

Wounded Bulls

Buying gold has been one of the consensus trades on Wall Street for years, but several banks have cut back their gold forecasts in recent weeks, including UBS Group AG, Goldman Sachs Group Inc and Deutsche Bank AG.

Still, analysts are broadly sticking with the view that gold’s longer-term bull case remains intact, even as few are rushing to call the bottom. The market has moved from “euphoria to reckoning”, said Nicky Shiels, head of metals strategy at MKS Pamp SA. The next leg higher would likely require the dollar’s recent rally to fade and structural themes like currency debasement to reassert themselves, she said.

After its worst month in nearly two decades, gold has found its feet above $4,000 an ounce over the past week as investors dialed back their bets on higher rates and a stronger dollar.

Some investors, like Alexandre Carrier at DNCA Invest Strategic Resource Fund, have been underweight on precious metals relative to other asset classes, but he’s planning to buy following the slump in prices.

“With more clarity on rates and when the US dollar stops strengthening, we will probably reinforce our positions,” he said.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All