KEY TAKEAWAYS

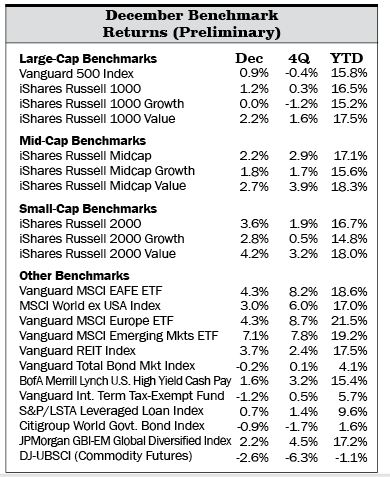

Stocks shrugged off numerous worries to log a very good year in 2012. The riskiest areas were the most profitable. Europe gained over 21% in 2012. Emerging-markets stocks earned 19%. In the United States, mid- and small-cap stocks slightly outpaced large-cap stocks, 17% to 16%.

The bond side also saw riskier asset classes outearning traditionally safer fixed-income market sectors. Emerging-markets local-currency bonds notably gained 17%. Domestically, high-yield bonds and leveraged loans returned 15% and nearly 10%, respectively, while investment-grade bonds returned 4%.

Our actively managed portfolios performed well relative to their benchmarks. Our active bond funds, in particular, added significant value versus the core bond benchmark over the last year.

Our expectation of slow economic growth has largely been right on over the past four years. Though there has been progress with deleveraging, the process is not nearly complete. And while the risk of another crisis has declined, it remains possible and is not easily dismissed.

A key risk going forward is how our politicians deal with the problem of growing public sector debt. The last-minute fiscal cliff compromise buys politicians a little time to address the more important longer-term fiscal issues, but does little to resolve them. Europe also made some progress in 2012, but most of that progress has been in the form of buying time by reducing borrowing costs.

The developed world continues to face significant debt-related challenges. The solutions are not easy and there are no quick fixes. Failure could play out in various ways, from another financial crisis to sharply higher inflation several years down the road. A brighter spot is that developing countries are generally less indebted and growing faster. However, growth has slowed there as well, partly due to the impact of reduced demand from the heavily indebted developed countries.

We recognize that there are a variety of bullish factors that could drive stocks to strong returns over the next five years. The odds of the bullish case playing out may be less unlikely than they were, but in our view they are still not high and it is more likely that we see a slow-growth environment with a continuation of aversion to risk.

Given continued risks and unsatisfactory return expectations for most asset classes across most of our scenarios, our portfolios are positioned in a moderate but not excessively cautious way and we hold some niche assets that we believe offer the potential to add value relative to our benchmarks. This strategy requires the patience to wait for better opportunities. This past year was an example of the strategy working as our portfolios beat their benchmarks despite being underweight to stocks in a very strong year for the stock market.

As we look ahead, one thing we know is that there will be higher taxes on investment profits. As always we will continue to make our asset allocation decisions for taxable clients based on our assessment of where we can capture the best after-tax returns.

|

Stocks shrugged off numerous worries to log a very good year in 2012. And when the bell rang to end the final trading session of the year, the riskiest areas were the most profitable. Europe gained over 21% in 2012. Emerging-markets stocks earned 19%. In the United States, mid- and small-cap stocks slightly outpaced large-cap stocks, 17% to 16%. The bond side also saw riskier asset classes out-earning traditionally safer fixed-income market sectors for the year. Emerging-markets local-currency bonds notably gained 17%. Domestically, high-yield bonds and leveraged loans returned 15% and nearly 10%, respectively, while investment-grade bonds returned 4%. Can the markets continue to climb the proverbial wall of worry? Certainly the worries remain. The most immediate has to do with the spending side of the fiscal cliff. The cliff deal made permanent the Bush tax cuts for all but high-income taxpayers but it did not address spending. The threat of sequestration is still with us (these are the automatic across-the-board spending cuts), though delayed for two months. The timing now coincides with the need to extend the debt ceiling in March. So while the worst case of the cliff was avoided, the work is not nearly done. In the bigger picture, this immediate concern is a side show. In the following pages we discuss our current assessment of the investment environment including a detailed look at what could go right, and tie it all back to our portfolio positioning.

Slow Growth As Expected—Now What? For several years we have communicated our expectation that the most likely outcome for the developed world economy would be years of slow growth. This view was based on our assessment that excessive debt levels in the United States and around the developed world had to be reduced, and that this lengthy period of deleveraging would suppress spending. Slower spending would be a major drag on economic growth. Further headwinds to growth would come from heightened risk aversion and increased regulation. This period of slow growth would be accompanied by risk of another financial crisis, possibly triggered by clumsy government policy responses to their fiscal challenges. And as we have pointed out, this expected environment is consistent with the aftermath of other financial crises throughout history. We have also believed that stocks were not fully pricing in the slow growth environment we expected and most definitely were not pricing in the most pessimistic of our scenarios, in which we experience another financial shock. Our expectation of slow economic growth has largely been right over the past four years. While we have been surprised at the strength of the stock market and corporate earnings rebound, our actively managed portfolios have performed well relative to their benchmarks over the full four years since 2008 (despite being underweight to equities), including in 2012. So has anything changed as time distances us from the financial crisis? The simple answer is that though clear progress has been made, the deleveraging process is not nearly complete. And while the risk of another crisis has declined, it remains possible and is not easily dismissed. As for the U.S. stock market, we continue to view it as richly priced relative to all but our optimistic “average recovery” scenario. From a financial market standpoint, monetary policy continues to be remarkably accommodative (not to mention experimental) and this is now increasingly true on a global basis. Exceptionally low interest rates continue to support prices of risky assets including stocks. The first part of our commentary briefly discusses our current take on the key macro challenges, which are primarily debt related.

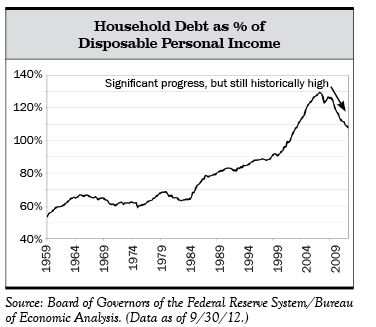

Here in the United States we have made some progress in reducing private sector debt:

As we all know, the public sector’s debt (i.e., government debt) has grown, and is a significant problem. We are all aware of the longer-term challenge: how to reduce deficits so we can maintain public sector debt at a sustainable and affordable level, while avoiding a fiscal retrenchment that will do excessive damage to the economy. The challenge is made even more difficult by 1) current high debt levels, 2) the impact of millions of retiring baby boomers and the resulting demands on entitlements for seniors, and 3) the high rate of health care inflation which impacts Medicare and Medicaid. (The Congressional Budget Office forecasts that without changes, by 2030, one in three dollars of federal spending will go to health care.) This requires hard decisions about how much government we can afford, what our priorities should be, and ultimately a philosophical debate about the role of government.

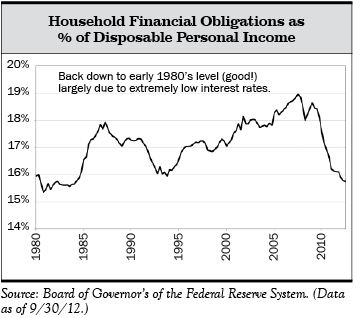

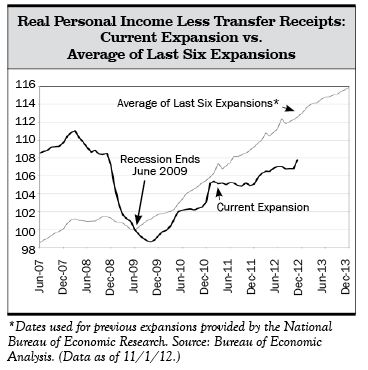

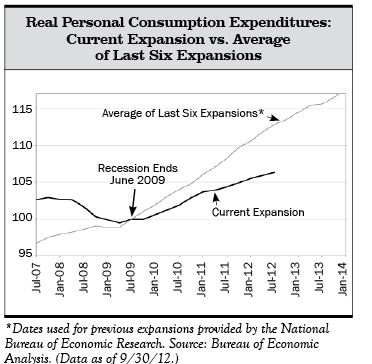

As we have written about often over the past four years, deleveraging has consequences to the overall economy. We are in a “paradox of thrift” world. This refers to a situation where individuals voluntarily or out of necessity become thrifty (saving more/borrowing less), but the impact on the overall economy is actually less savings and spending. This happens because what is good for the individual is not necessarily good for the economy. In the overall economy, more saving means less spending, which means less immediate demand for goods and services, which results in fewer jobs, which means lower income, which means less ability to spend and save. This vicious circle is what is happening in many parts of the developed world. In the United States we can see it in the very slow growth of disposable income and consumption. Both have been abnormally low relative to past recoveries. This phenomenon is absolutely expected in the aftermath of a major financial crisis. And now fiscal stimulus is winding down and this shift means that reduced government spending (though still high) will offer less support to the economy relative to recent years. A reduced rate of spending growth will continue to serve as an economic headwind as we attempt to rein in the growth of public spending. This same dynamic is playing out in much of the developed world.

A key risk going forward is how our politicians deal with the problem of growing public sector debt. Reducing the growth of debt at the right pace and in the right way is necessary, but not easily achieved. The risk is that this goal is not achieved, or that it is only achieved after political dysfunction triggers a crisis. 2013 will be an important year as politicians are charged with putting in place a viable longer-term plan. If this is not done in 2013, the risk is that it won’t be done until after the next presidential election, unless a crisis comes first. The lost time will mean we will face a bigger problem with tougher choices and likely even greater consequences. The markets will be watching and may not behave well if the wait lasts until 2017. Europe also made some progress in 2012—but most of that progress has been in the form of buying time by reducing borrowing costs and thereby lessening the “tail risk” of an imminent eurozone breakup. There has been some improvement in the peripheral countries as most seem likely to have current account surpluses in 2013; capital flight appears to have stopped, and there are signs that the push for austerity may soften a bit.

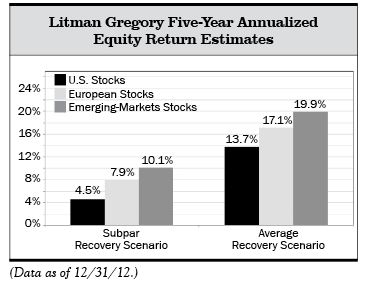

The problems in Europe ultimately reflect competitive imbalances. After the launch of the euro in 1999, interest rates for historically less-fiscally sound peripheral countries dropped to Germany’s levels. This set off a borrowing (and lending) binge to fund consumption, and in some countries (such as Ireland and Spain) led to housing bubbles that have not all fully burst yet. Because the peripheral countries were not competitive with Europe’s core, largely due to labor costs, they ran large trade and current-account deficits. This greatly benefited Germany’s export market. Lenders were lax in their underwriting and ultimately banks were saddled with bad loans leading to a severe banking crisis and the need for bank bailouts—this part of the story is still unfolding. In Ireland, huge bailouts essentially bankrupted the government. Spain is threatened with the same outcome, which is why there has been a desire to allow European bailout money to go directly to the banks, rather than through the government (to avoid forcing the government to take on so much debt). The problems of the banking crisis are exacerbated because the banking sector is huge in Europe—much bigger than in the United States. Also exacerbating the problem is that European banks are heavily leveraged and not heavily funded by deposits, which are the most stable funding source. Unlike in the United States, European banks have not deleveraged and this too will be a problem for growth. In August, the European Central Bank stepped up with outright monetary transactions, or OMTs, the open-ended program to purchase distressed eurozone government bonds. We discussed the OMTs at length in our last quarterly commentary. So far the program has been successful (without yet deploying any funds) in relieving market fears of a eurozone breakup and reducing sovereign bond yields in the periphery. This is a very important accomplishment. However, while it buys time for these countries, it does not solve the underlying problems of too much debt, a lack of growth, and the competitive imbalance between core and periphery Europe. Europe is now back in recession. Severe austerity has taken a toll on growth and appears to be counterproductive. It remains an open question whether European governments will be able to make the right decisions with respect to: growth policies, pursuing competitive balance, debt relief, and the fiscal and banking integration that is needed to hold together the single currency over the long run. As challenging as the politics are in the United States, the challenges are even greater in Europe where countries with different cultures and economic characteristics are being asked to give up some of their economic sovereignty. Solving these problems will take a long time and along the way they could trigger more serious social unrest. As in the United States, Europe’s problems are all about debt-related economic headwinds and the threat of political mishandling of a fragile economy. But in Europe, the problems are more complicated because the weaker countries don’t have the option of devaluing their currencies to improve their competitive position relative to Germany. Instead they must accomplish this with structural changes such as labor market reforms and real-wage cuts. One important distinction between the investment prospects for the United States and Europe is that European stocks are cheaper—our expected annualized return for European stocks is around 8% in our base-case scenario. (We made a dedicated investment in European stocks in June, right around the market bottom.) Japan has not been in the headlines like Europe, but its government debt relative to GDP is about twice the level of Europe or the United States, and close to twice as high as it was 10 years ago. Private sector debt is also high. However, the country has largely been able to self-finance thanks to a high savings rate. But as the population ages, the savings rate is declining and the country is beginning to rely more heavily on foreign lenders. Moreover, having struggled with deflation off and on for many years, Japan is trying to reflate. While ending the long period of deflation is clearly a desirable goal, a byproduct of this period has been extremely low interest rates. Long-term government bond yields are under 1%. If inflation returns, Japan risks being caught in a debt trap where even a relatively modest rise in the borrowing rate on its massive government debt could result in sharply higher debt service costs that would widen its deficit and increase the rate of debt growth. So the developed world continues to face significant debt-related challenges. The solutions are not easy and there are no quick fixes. Failure could play out in various ways, from another financial crisis to sharply higher inflation several years down the road. A brighter spot is that developing countries are generally less indebted and growing faster. However, growth has slowed there as well, partly due to the impact of reduced demand from the heavily indebted developed countries. Then, of course, there is the Middle East—always a wild card and perhaps even more so right now with continued shifting sands from the Arab Spring, and the possibility of military conflict with Iran that would likely lead to an oil shock. It is Important to Consider the Optimistic Scenario Our message has been consistent, even as new information unfolds, that deleveraging will mean slower growth at the same time it raises the risk of another financial crisis. That said, an important part of our investment discipline is to minimize the risk of “confirmation bias.” Confirmation bias refers to the human tendency to seek out and favor information and data that supports one’s beliefs, arguments, etc. Confirmation bias is a powerful trait that all people are prone to, and our industry is not immune. We all want to be right and confirm our beliefs. This can lead to digging in one’s heels, dismissing counter evidence, and ultimately an avoidance of admitting mistakes. In the long run it’s valuable to be able to change one’s mind when we’re presented with new information. John Maynard Keynes famously said, “When the facts change, I change my mind, what do you do?” (Actually there is some controversy as to whether Keynes actually ever said this, but we like the quote anyway.) Our attempt to avoid confirmation bias in our decision-making involves lots of debate among our team and exposing ourselves to alternative points of view through our reading and working our extensive industry network. Most important, our scenario approach forces us to think through a variety of possible outcomes. With that context, the next part of this commentary lists a variety of bullish factors that, though counter to our base-case view, could drive stocks to strong returns over the next five years. 1. First, the passage of time has led to an improvement in our expected returns for stocks. This happens as we anticipate a return to more normal earnings growth in the later years of our analysis. As we write this, our five-year expected returns for U.S. stocks in our base-case subpar growth scenario are still low, at about 4.5%. This scenario now assumes a gradual return to trend-level earnings. But in our optimistic scenario, the returns—at close to 14%—are very strong. This scenario assumes that as we put deleveraging-related headwinds behind us, earnings can temporarily overshoot the long-term trend level (we assume by 20%) in five years. Expected returns in this scenario for European stocks (which had suffered large price declines until a market rebound that started in June) and emerging-markets stocks are materially higher than for U.S. stocks.

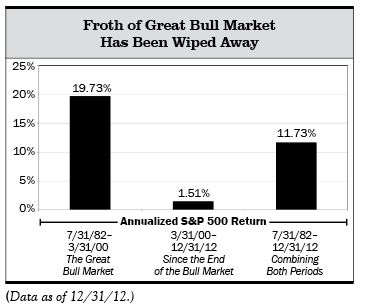

The passage of time is important in other ways. Let’s remember that an enormous amount of froth has been taken out of stock prices. The stock market, as measured by the S&P 500, is at a level first reached 13 years ago. And even with the rebound from the extreme lows of 2009, the two bear markets since the start of the 2000s have taken back much of the great bull market of the 1980s and 1990s (that started in the summer of 1982). Looking back over 30-plus years, a period that encompasses that great bull market, the annualized return for the stock market is around 12%. That is a good return but it’s not exceptional and, as such, is evidence that the froth of the incredible 17-year bull market has been wiped away. Besides the fact that stock prices were flat over the past 12 years, multiples are much more reasonable than they were.

2. The risk of another financial crisis has declined. Time has allowed for some healing, some deleveraging has happened, and Europe has made some progress. So the risk of a crisis that leads to deflation is less than it was. Over time, this should have some impact on investor risk-taking, especially if this trend continues. 3. There have also been enormous changes with respect to investor sentiment and fundamentals that drive expectations. For example, stocks recently comprised 35% of household financial assets compared to over 50% in early 2000. Over that period of time, households withdrew about $1 trillion from stock funds. And almost the same amount has flowed into bond funds since March 2009. U.S. public pension funds have also been selling stocks, with allocations falling from 70% to 52% over the past 10 years, according to the Financial Times.

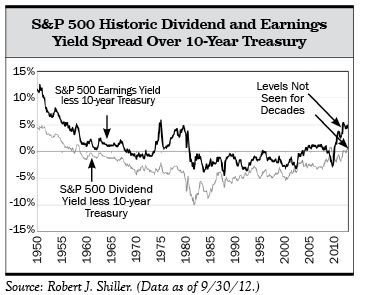

These shifts reflect huge changes in investor confidence. Confidence about the economy was very high in early 2000, about double today’s level. Today’s low confidence is clearly related to the losses experienced during the financial crisis and its aftermath as we deal with the related problems of debt, lack of demand, and weak job growth. The labor market is particularly important. In early 2000, the unemployment rate was just over half of today’s 7.7%. The takeaway is that bull market peaks are characterized by overconfidence. Back in 2000, when optimism was unrestrained, we recall a consensus forming that the economy would be less volatile with fewer and shallower recessions. There was growing belief that asset valuation didn’t matter. Conversely, bull markets are born from pessimism that makes investors cautious and keeps expectations low. Fears of another financial crisis are a good example of this. When expectations are low and fundamentals have been weak, improving conditions are more likely, i.e., it is easier to have a positive surprise. When expectations are very high, there is greater risk of disappointment. This confidence obviously has an impact on stock prices, with optimism usually leading to overvalued stocks and pessimism leading to undervalued markets. Confidence, while improving, is not high as we head into 2013. As a contrarian indicator, this is a positive. 4. Relative valuations driven by the Fed’s low interest-rate policies could continue to play a big role in equity returns going forward. Valuations are in a fair-value range (not cheap) on many absolute measures. If one assumes that macro forces will result in below-average earnings growth (as we do in our base-case scenario), stocks look around 20% overvalued. However, if economic growth gradually improves, tail-risk fears subside, and as time further distances investors from the financial crisis, investors could find stocks far more appealing than bonds or cash. Cash yields nothing (and has a negative return after inflation) and is likely to continue to be the case for some time given Fed policy. Bond yields are also painfully low and everyone knows that at some point there will be a rise in interest rates that will result in lower bond prices. This point may be far down the road, but, in the meantime, investors are increasingly aware of the longer-term risk in holding bonds, and they are paid very little to take that risk. In terms of the relative yield, stocks have not looked this attractive compared to bonds for decades. If time continues to pass without a crisis, and moderate economic gains allow earnings to make steady progress, stocks could benefit from the mountain of cash allocated to bonds in recent years starting to be reallocated back into the stock market.

5. Uncertainty about policy decisions and debt-related risks continue to drive investor concerns. However, these risks are the subject of great focus and real progress could be made in 2013. As we mentioned at the outset of this commentary, Congress’s last-minute compromise on the fiscal cliff on January 1, 2013, allayed the worst fears of tax increases combined with abrupt spending cuts. However, President Obama and Congress will still need to address the spending cuts, which were delayed for two months and it remains to be seen if politicians can agree upon a credible plan for long-term deficit reduction. If they do, that could go a long way toward mitigating concerns about future debt build-up and related policy errors. In the United States, this could unleash corporate animal spirits as the fear of tail risk subsides. The corporate sector is sitting on a lot of cash that could be used for capital investment and hiring as some of the uncertainty recedes. (Corporate sector cash is a positive no matter what—companies are buying back large amounts of their shares. This improves earnings per share over time. If uncertainty declines and businesses instead invest for growth, this will be good for the overall economy.) In Europe there is also fear of policy errors and though this fear is certainly justified, it is also possible that 2013 could see progress toward banking and fiscal union and a return to growth later in the year. If that happens, fear of a disorderly breakup of the monetary union could decline. Less uncertainty would be bullish for stocks. 6. The global economy has experienced some encouraging macro developments. In the United States, the housing market may be in a sustainable upturn. Home values are increasing and are cheap relative to replacement costs, and interest rates are exceptionally low for those who can get a loan. Housing starts are moving up from of a very low level. Housing is now a driver of growth rather than a drag on growth. Credit markets also continue to improve with easier lending standards. And the labor market is slowly healing, though it remains historically weak. The number of unemployed per job opening remains high, but is steadily declining and virtually every labor market measure is getting better, though there is a long way to go before the patient is fully healed. And as mentioned, there is a possibility of the economy gaining more traction if corporations loosen their purse strings and begin to invest and hire. Overall, there is no robust growth story, but the recovery is broadening out and the participation of the housing sector is important. Outside the United States, the growth slowdown in the emerging markets may have ended and there are numerous signs that China’s economy is picking up (though not to previous growth levels). Even Europe, currently in recession, could start growing again in the second half of 2013. How Probable is the Bullish Case? The odds of the bullish case playing out may be increasing, but in our view they are still not high. There is no easy road out of our debt bind and there are consequences to that reality. The only easy road would be robust growth, but this is close to a mutually exclusive condition with a deleveraging global economy. So despite somewhat improved odds of the bullish scenario, it is more likely that we see a slow-growth environment with a continuation of some aversion to risk. In this environment, corporate earnings will be challenged as growth through cost cutting has largely played out. Revenue growth will need to be a driver and ultimately that will depend on demand. Partly due to very high (and potentially unsustainable) profit margins, our estimate of normalized earnings is materially below the current level. As to the point of low interest rates making stocks look cheap, we know that rates can’t stay this low indefinitely, but if they do for many years it will mean that the economy has continued to be very weak, which ties back to our expectations for low earnings growth. And while we believe the risk of another financial crisis has declined, it remains higher than we would like it to be. We are reliant on public policy to make wise decisions in a highly politicized world. In Europe, solutions require one country’s taxpayers bailing out another’s (or several others’). And it requires populations sacrificing their standard of living to obtain those bailouts. This may work out in the end, but we don’t think we should be quick to assume a happy ending. In the United States it requires compromise between Republicans and Democrats—something that seems more plausible than it did a year ago, but still no slam dunk. In the worst case of outright policy failure, we could be looking at another devastating bear market. That seems less likely with the passage of time, and outright failure is less likely than partial failure. However, as we have seen, markets are not forgiving when fearful and the wrong decisions could lead to another market revolt. How This Impacts Our Portfolio Positioning So where do we net out after fully considering the positives and weighing them against our concerns? Our portfolio positioning reflects several considerations:

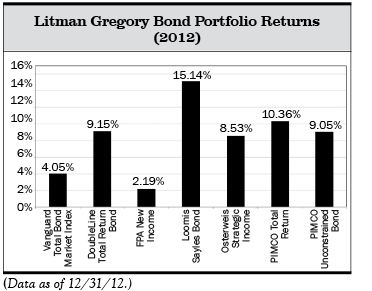

During 2012, our fixed-income positions added enormous value to our portfolios and helped to offset the impact of our equity underweight. Here is how these funds performed relative to the Vanguard Total Bond Market Index (our proxy for the core bond market benchmark):

A reasonable question going forward is whether this sort of outperformance can be expected again. We have rightly been significantly underweight to the bond index, preferring exposure to other areas of the bond market, and we expect that to continue to be the case. Our expected five-year return for the core bond index is under 2% in all scenarios—largely due to its sizable allocations to ultra-low-yielding government bonds. Our view is that there is still sizable potential for excess returns from our fixed-income positions in coming years, but the magnitude is likely to be less than what we captured in 2012. Most of the bond funds we hold pay much higher yields than the bond index and have less interest-rate risk. The lower-interest-rate risk is a function of lower duration and more credit exposure, which is likely to perform better in a rising interest-rate environment. (Many of these funds may not perform as well as the index in a recessionary bear market environment.) However, yields have come down and this means lower potential returns than what we were able to capture in 2012 and over the past several years.

Osterweis Strategic Income is one bond fund we have owned for the past few years. It has out-returned the bond index over the trailing three and five years by about two percentage points per year (200 basis points). The fund’s portfolio has a yield-to-maturity of over 5% after expenses (more than triple the yield on the bond index), and has a low duration of about two years, so interest-rate risk is low. However, this yield has declined significantly over the last few years and the fund won’t be able to match its trailing returns of between 7% and 8% over extended time periods. However, capturing the yield would get us a return of around 5% and we believe a return of 4%–6% is a realistic expectation. We view this fund as earning us a relatively low-risk return while we wait for better opportunities. At present we are not anticipating major changes in our portfolio positioning unless we see a significant change in market pricing or fundamentals. One possible exception is our exposure to municipal bonds funds, which we may slightly reduce, though we wouldn’t view this potential move as urgent. The municipal bond market rallied through most of the year and was recently priced at absolute yield levels that, while attractive relative to Treasurys, are not as attractive relative to other flexible bond fund options on an after-tax basis and also in light of higher interest-rate risk over our five-year investment horizon. One encouraging sign was the improved showing of active equity managers late in 2012. This was reflected in the performance of our managers who, on average, beat their benchmarks for the year. This is also reflected in the performance of our Equity model. This improved performance kicked in later in the year and is a welcome change from the last three years of severe underperformance. To get a sense for the magnitude of active manager underperformance, one measure is to look at the Vanguard 500 Index Fund return over the last three years versus its fund peer group. This fund tracks the S&P 500 Index and ranked in the top 18% in the peer group based on Morningstar data. This compares to a top 45% rank over 15 years. Clearly, the index has been much tougher to beat recently than over the long run. (Our Equity portfolios have beat the S&P 500 over 15 years.) One likely reason is the focus on macro risks that cause investors to sell or buy stocks as a group, rather than focusing on individual company fundamentals. This has been reflected in high correlations between stocks through much of the last few years. Very recently correlations have dropped, though we are not confident in saying that we are now entering a sustained period of more typical correlations. But we do expect that to happen at some point and when it does, skilled active managers should find it easier to add value. As we look ahead, one thing we know is that there will be higher taxes on investment profits. As always we will continue to make our asset allocation decisions for taxable clients based on our assessment of where we can capture the best after-tax returns. And changes in client portfolios will be implemented only after weighing any tax cost against the expected economic gain from the change. What Could Change our View? Our commentaries have been rather depressing reads in recent years. This one may have been somewhat cheerier as we laid out factors that could result in a more optimistic scenario playing out. However, the weight of the evidence still suggests global deleveraging will create an environment that will mute returns and carry outsized risks. And we also are aware that some policies already in place are virtual experiments—specifically Federal Reserve monetary policy. As the Fed buys assets their balance sheet is growing. Currently, their balance sheet equals 18% of GDP and heading much higher given their commitment to continue to buy Treasury and mortgage securities each month. These policies are unprecedented and are goosing financial asset returns higher. We all hope they will be effective and can ultimately be reversed without causing a harmful inflation problem down the road. But while we are not concerned about this risk in the near term, longer-term we can’t be confident how this will play out. What would shift our outlook toward the more bullish scenario? One factor would be policy decisions that credibly address the structural problems relating to debt and the need for economic growth. Positive surprises with respect to economic fundamentals would also be a significant development and would help us foresee an easier path to debt reduction. Less enjoyable, but nevertheless significant, would be a sizable market sell-off that results in higher stock market return expectations from that point forward. Given continued risks and unsatisfactory return expectations for most asset classes across our macro scenarios, our portfolios are positioned in a moderate but not excessively cautious way, and we hold some niche assets that we believe offer the potential to add value relative to our benchmarks. This can be a frustrating strategy that requires the patience to wait for better opportunities. But this past year was an example of this strategy working as our portfolios beat their benchmarks despite being underweight to stocks in a very strong year for the stock market. We wish you all a happy and profitable 2013. —Litman Gregory Research Team (1/3/13) |

© Litman Gregory Research