One of our family’s most memorable and pleasant vacations took place years ago when we visited Cape Cod, Massachusetts for the first time.

Among the numerous highlights: swimming at the Cape Cod National Seashore, the freshest possible harborside seafood dinners, touring the many quaint villages, endless sunsets over the water, and, of course, visits to those ubiquitous “all you can eat” pancake breakfast restaurants (a favorite of the kids). For the adults, a side trip to the famous Kennedy Compound in Hyannis Port, along the Nantucket Sound, was a special treat.

But nothing topped taking the children out to the very tip of the island for a whale-watching cruise departing from historic Provincetown. By the end of the hours-long excursion, we believed the Captain when he said “it doesn’t get much better,” having witnessed up close several different whale species and many travelling as “families” or “pods” (different families together).

I thought of this trip in pondering some of the market news this week, where Wall Street was practicing its very own version of “whale watching.”

The Street’s whale watching comes in three different forms, all of which involve the very close viewing of the investment decisions by the biggest and most famous hedge fund managers out there. These particular “whales” reveal their specific fund actions approximately 45 days after the end of each calendar quarter, through required filings with the SEC. This is a highly scrutinized event, with several websites devoted exclusively to detailed analysis and usually exhaustive press coverage.

The second example involves periodic and unscheduled announcements by fund whales touting particular stocks or asset classes they are buying or selling, fondly known as “talking their book.” This can take the shape of a 150-slide presentation to other fund managers and analysts, a detailed research report, or, in the newest twist, a simple tweet. But however the information is released, the goal remains the same: trying to influence other market players to their side and bolstering support for their positions, which can be quite substantial.

The third and perhaps the favorite of the business media has dueling hedge fund whales publicly airing their differing points of view on certain companies or investments. More and more, this has become quite the public spectacle, as each “blows hard” about their opinions.

This past week saw the trifecta of whale sightings:

- SEC second quarter filings were revealed, with those of the biggest whale of all, Warren Buffett, garnering the most headlines. His upping of Berkshire Hathaway’s stake in General Motors was just one of many significant actions, with his company also selling major portions of holdings in Kraft, Mondelez and Gannett and initiating a new stake in Dish Network. Buffett’s “Big Four” core holdings in American Express, Coca-Cola, IBM and Wells Fargo were relatively unchanged, with some additional WFC shares purchased. (Berkshire also apparently has some sort of major surprise in store, as part of its filing was kept confidential.)

- Carl Icahn perhaps single-handedly changed the sentiment surrounding Apple with two tweets early in the week as he announced a “large” position in the stock and encouraged further stock buybacks by the company (strongly suggesting he has the ear of CEO Tim Cook). Wired Magazine called these the “$17 billion tweets,” with Apple’s market cap increasing that amount this week alone.

- And Mr. Icahn was also highly visible in his continuing public and vitriolic disputes with fellow fund manager Bill Ackman over the prospects for nutrition and weight loss company Herbalife and with Michael Dell over the founder’s efforts to take Dell private through a buyout.

There were also at least two other notable whale sightings in the past two weeks, each of which may have played a small role in the current weaker market sentiment.

It was revealed that one of the largest positions of legendary investor George Soros is a bet against the S&P 500, at least as of last quarter. And market-mover David Tepper of Appaloosa Management, who has been one of the biggest cheerleaders of the bull run since 2010, said in an interview recently, “If I was super bullish before, I’m just bullish now.”

But there were certainly many other factors this week as the Dow recorded its weakest performance in 2013 and the major indices had their first back-to-back weekly losses since late June, with both the Dow and S&P down over 2%. StateoftheMarkets.com pointed to any number of recent concerns laying bricks on the wall of worry, with higher interest rates, uncertainty over Fed tapering, disappointing forward guidance by several bellwether companies, doubts about China’s growth, the upcoming Washington budget battles, and unrest in the Mideast leading the list.

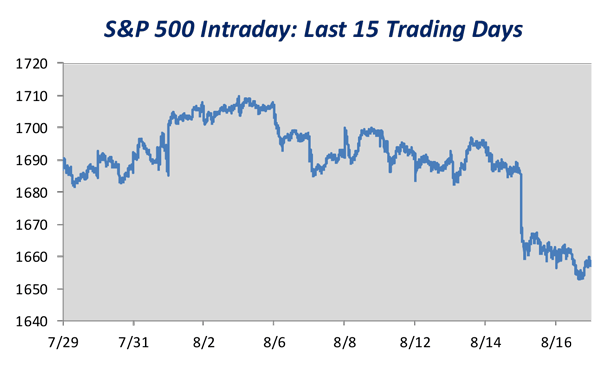

The action over the past two weeks certainly looks less than encouraging, as the S&P chart below indicates:

Source: Bespoke Investment Group

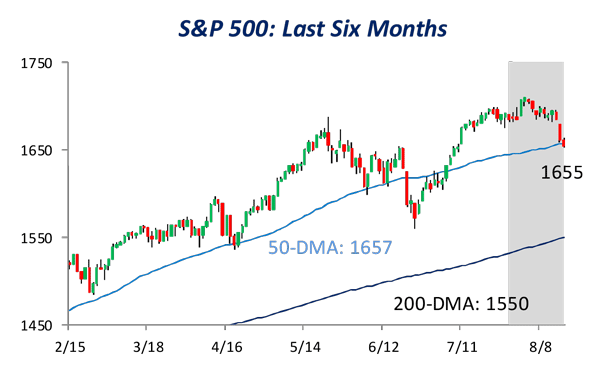

Bespoke Research noted the market’s struggle this week, but concluded that bulls should not “lose all hope yet” as “the first two weeks of August have been poor for equities over the last several years.” The S&P finished out an options expiration week just below its 50-day moving average, a critical junction point, with technical indicators now leaning more neutral than bullish.

Source: Bespoke Investment Group

Will the 50-day MA hold again, as it has several times this year, or give way as seen in June, leading to some significant market declines?

As said a time or two in this space, investing should not be about guessing the market’s next short-term move. Rather, we believe a disciplined, well-diversified approach to active portfolio management can produce higher risk-adjusted returns over time and much better performance in times of market stress.

The temptation to chase the latest “hot trade” of the day, week or month is strong, but it can frequently be costly and misguided, and based on some very misleading information.

For example, trying to follow the holdings or recommendations of major hedge funds is in effect utilizing facts which are outdated and incomplete, to say the least. Who can really say with certainty what those funds are holding today, or tomorrow, or how their overall portfolios are structured and hedged? MarketWatch has commented that trying to follow these funds’ investments can be a bit like watching the light emanating from a distant star which just now is reaching us – a star which might not even exist today.

So, as the summer winds down, we think we will keep our whale watching confined to that of the denizens of the deep, not those inhabiting the dark pools found on the “Street.”

© Flexible Plan Investments