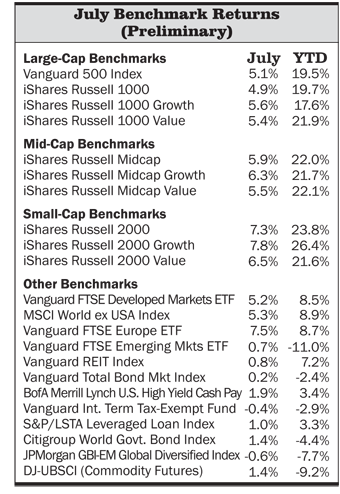

U.S. stocks resumed their positive streak in July (after a slightly negative June). Large-cap stocks rose in three out of the four weeks and were up 5% for the month. Smaller companies generally outperformed their larger-cap counterparts. After Federal Reserve comments regarding the timing of its stimulus withdrawal upset markets in May and June (particularly the bond market), investors seemed to take comfort in the Fed’s more recent comments. Among other points, Chairman Bernanke reiterated that a decision to taper bond purchases is different from raising the federal funds rate. While the former may begin as soon as this autumn—if economic data continue to show improvements in growth and employment, amidst subdued inflation—a decision to raise rates would still be much further out, likely occurring after unemployment dips below 6.5% assuming no serious inflation concerns.

U.S. stock markets also digested economic data that by and large showed a continuation of weak economic growth buoyed by a strengthening housing sector (despite a recent increase in mortgage rates), and a slowly improving employment picture. Corporate earnings season got underway as well. While we don’t put much (if any) stock in the short-term earnings game, the data does suggest a slowdown in the rate of earnings growth in recent quarters, a trend that doesn’t surprise us given the generally tepid level of global economic growth.

After a negative second quarter, the core bond benchmark was slightly positive thanks mainly to a rebound among corporate bonds. Bonds viewed as most sensitive to changes in Fed policy—Treasurys and mortgages, for example—saw very slight losses in July. High-yield bonds and floating-rate loans were among the stronger bond market sectors in July. (Because these represent the debt of less financially secure companies they tend to react well to positive economic news.) We have a dedicated allocation to floating-rate loan funds in our conservative portfolios and have some exposure to the high-yield market through the selections of some of our active bond fund managers and so our portfolios were able to participate in these trends.

International stocks also rebounded from their weak second quarter performances. Amidst short-term indications of growth improvements in Europe and a continuation of Japan’s stronger economic growth (for now), the developed international stock index rose roughly 5%. Emerging markets improved slightly and gained close to 1% for the month. Still, China’s economic data continued to indicate slower growth, a topic we cover within this month’s commentary. Year to date, emerging markets have trailed U.S. large-cap stocks by approximately 30 percentage points, the largest divergence in more than a decade. Our commentary also reviews why we have not further increased our allocation to emerging-markets stocks, despite their lower valuation. A key reason is our concern that a busting of the infrastructure bubble in China could lead to slower growth and poor returns in China and negatively impact emerging markets overall. We think it prudent to await a greater margin of safety before taking on additional emerging-markets exposure.

This month’s Q&A commentary covers a wide range of topics, all of which relate to our current strategy. We did not make portfolio changes during the month and, as a result, remain modestly underweight stocks (U.S. equities primarily) based on our expectations of subpar returns over most of our five-year scenarios. In an effort to soften interest-rate risk and improve the return potential of our bond allocation, we are tilted toward flexible and absolute-return-oriented funds, and these again added value in July as they have done throughout our holding period.

Research Team Q&A

We regularly use a question-and-answer format to address questions from readers about our investment views and current strategy. This format permits us to address a range of different topics and allows readers to focus on areas of interest. Members of our research team worked on this Q&A piece jointly, and answered questions received during the past several weeks.

INTERNATIONAL STOCKS

Your model portfolios have evolved over the years to become much more global. You’ve provided a lot of detail in the past about your U.S. stock valuation framework, but can you speak further to your valuation framework for foreign equities?

At a broad level, our valuation framework for other equity classes, such as European and emerging-markets equities, is similar to that of U.S. equities. We try to assess a few key variables:

- First, we try to assess the long-term normalized earnings level and earnings growth for the asset class overall. We do this by analyzing historical earnings trends/paths across different macroeconomic environments, i.e., across varied periods and levels of economic growth or recessions, interest rates, inflation, etc. Our forward-looking qualitative view of the environment then informs what earnings path and/or normalized earnings growth we can reasonably expect.

- Second, at any particular point in time, we analyze whether an asset class is over- or underearning relative to this normalized earnings power and by roughly what magnitude. Inevitably, history shows that stocks, wherever they are domiciled, in aggregate revert to their normalized earnings power. We typically assume asset classes revert to their normalized earnings power in about five years, though we know it can happen sooner or later. For example, in the current cycle the normalization process may take longer than five years because of unprecedented and, we believe, unsustainable monetary policies. It is also important to note that at any point in time, over a year or even a few years, we do not expect actual earnings to follow the exact earnings path we have come up with. Our focus is on long-term (or normalized) earnings levels, and if we are roughly right in our estimate of earnings outcomes, then as market participants become too optimistic or pessimistic relative to our framework, we believe we can add value by making tactical shifts in or out of equities.

The goal of these two steps is to come up with what we think are reasonable earnings growth expectations five years out within the range of economic scenarios we consider plausible.

- The third step is our assessment of valuations. In this step, we try to assess what valuation multiple is fair or prudent to apply to the normalized earnings power of an asset class five years out. This involves an exhaustive study of history, again factoring in what sort of valuation multiples were seen historically and why, and applying our judgment as to what valuation multiple a prudent investor would pay in order to be adequately compensated for taking on equity risk in the economic environments we see plausible. Our absolute-return orientation, not relative-return orientation, in managing portfolios has an important influence on what valuation assumptions we choose.

Finally, we analyze what dividends or income can realistically be obtained. We use current dividend yield unless we see a compelling reason to use a different number. Generally, qualitative variations in this factor do not materially alter our return expectations over the next five years. Dividends are, of course, an important component of returns, but for the most part, earnings and valuation multiples contribute to most of the variance in our return estimates.

In the case of U.S. equities, we have a long earnings and valuation history to analyze. However, in Europe and emerging markets, we do not have a long data history. This impacts our decision-making in two ways. One, we rely more heavily on our qualitative analysis and judgment when assessing normalized earnings level and growth. Two, our confidence in these models is not as high as it is in the case of U.S. equities. Hence, we require a bigger margin of safety or a bigger return differential, in both absolute terms and relative to U.S. equities, before initiating a tactical over- or underweighting in Europe and emerging-markets equities.

If your investment thesis for emerging-markets stocks hasn’t fundamentally changed, why did you not add to it during the June sell-off? At what trigger point would you consider adding to your position?

As we just outlined, we have a higher return hurdle for over- or underweighting assets classes like emerging-markets equities. We did not add to emerging markets during the recent sell-off because of a number of factors:

- We have been concerned for several years now that China’s massive investments in infrastructure and property were excessive and could lead to poor returns, bad debts, and potentially a hard landing for China. This scenario could have global repercussions, but, importantly, could result in a severe negative outcome for the rest of the emerging-market countries. Bottom line, while we did not include this severe China risk-scenario in our base-case return expectations, it has so far prevented us from having a larger position in emerging markets. Over the past year, as emerging markets have underperformed, we have added to them, but in a very measured fashion. As a result, we are only 1% tactically overweight to emerging-markets equities in a typical balanced portfolio relative to our strategic weighting, though within our equity allocation, we are overweight to emerging markets relative to U.S. equities.

- In the past month or so, it has become clear that this China risk has become more prominent in investors’ minds, in part because the Chinese government is concerned about its past overinvestment and potential bad debts, and is taking steps to rein in credit growth. China’s actions in turn are slowing growth there as well as in the rest of the emerging markets, which has led emerging-markets assets to correct sharply in May and June. Now, the good news is that this slowdown and our concerns about China’s infrastructure bubble leading to poor returns and slow growth has to some extent been priced in to emerging-markets stocks. Also, it is good to see the Chinese government taking actions to address this issue before the problem gets even bigger, so this bodes well for the very long-term growth prospects of China as well as emerging markets overall.

- However, the bad news is that a mere acknowledgement of the problem by China does not mean that the problem has gone away. There is a real risk that the infrastructure bubble is already big and that as this bubble unwinds, it could inflict damage that may still not be adequately priced in. As we see it, this overinvestment could unwind violently, which would mean a hard landing for China and would not be good for all risk assets, and certainly not for emerging-markets risk assets. Or it could occur in a slow, inexorable fashion, which would also be damaging for emerging-markets risk assets.

- We think it is prudent to no longer assume the unwinding of China’s infrastructure bubble as only a risk scenario, but consider it as a sub-scenario that is part of our base-case thinking and one that could very well play out. Based on the initial work we have done thus far, modeling what we believe are some really bad earnings growth outcomes for emerging-market equities in this sub-scenario, we get potential five-year returns for emerging-markets equities in the 5%–8% range. In other scenarios, returns could be much lower; at this point we think these scenarios are unlikely, but we continue to evaluate these risks.

- Now, modeling some bad outcomes does not mean we are giving up on our current base-case return expectation of 13%–14%—that may still happen. China has a lot of policy flexibility to engineer a relatively smooth adjustment. For example, real rates in China are positive, so there is a lot of room for monetary easing. The new political leadership also seems to be serious about embarking on supply-side reforms that will prove challenging in the short term, but would ensure healthy growth for China and other emerging markets over the long term. Lastly, it is quite possible that the infrastructure bubble in China is not as big as we fear, in which case low double-digit to midteen returns are quite possible from here. If this outcome were to pan out, then we may have missed an opportunity to add to our tactical position (though we may still get that opportunity). But that’s not the end of the world as we already have a significant allocation to emerging-markets stocks and would likely benefit.

- We have to consider other broader portfolio-level issues. First, as our clients know, we manage our portfolios to specific 12-month downside risk threshold targets. We model in higher downside in emerging-markets equities and adding more to this position increases the likelihood of violating our downside risk thresholds in some of our models. So, in order for us to take this risk, we have to be extremely confident that we’d get paid to increase our allocation to emerging markets. Second, we have to consider how we’d fund an increase to emerging-markets equities. One natural funding source would be U.S. equities, where our base-case return expectation is quite low relative to emerging-markets equities. However, we can think of a scenario that could generate high single-digit annualized returns in U.S. equities from here. This could be happening while our bad sub-scenario in emerging markets noted earlier is playing out. In addition, we know our return expectations typically don’t transpire in a straight line, i.e., U.S. returns could be front-end loaded while emerging-markets equity returns are back-end loaded. So, at this point, we’d like to see the range of 5%–8% in our China risk scenario to shift up at least a few more percentage points more before we consider adding more to emerging-markets equities.

In your scenario analysis, did you explicitly think through how a change in Fed policy might impact emerging-markets debt and currencies?

First, it is important to review how we think about our position in the emerging-markets local-currency sovereign bonds we have through PIMCO’s Emerging Local Bond fund. Our time horizon for this position is longer than the five years typical for our tactical position. In some respects, we see this as a strategic position. Even with the recent rise in U.S. rates, the differential in real rates, or carry, offered by emerging markets remains attractive in our view.

Moreover, emerging-markets local-currency bonds perform the role of an inflation/dollar-decline hedge in our portfolios. Longer term, as emerging markets mature and their local-currency, sovereign bond markets deepen, we expect a convergence of sorts in rates—whether it stems from emerging-markets rates declining (which they have to an extent since we took on the position in 2009, and offered some nice capital appreciation), or U.S. rates rising, or a combination of both.

We did not explicitly model how leveraged carry-traders would behave in part because we do not know when and how they would behave, and we certainly would not be concerned by their behavior over a span of two months. (Unwinding the carry trade was one of the factors in second-quarter declines of emerging-markets currencies and bonds.) We acknowledge the equity-like risk of this asset class and that’s why we fund this position from equities.

Bottom line, for us to unwind our position in emerging-markets local-currency sovereign bonds, our long-term fundamental outlook has to change. At this point we continue to expect solid mid- to high-single-digit returns from this asset class. However, here too, we are evaluating how an unwinding of China’s bubble impacts our long-term thesis. In this scenario there is certainly a heightened risk that emerging-markets fundamentals will be impacted to such a degree that exposure to emerging-markets currencies becomes a major headwind rather than the minor tailwind we expect in our base case. As we evaluate this scenario more, it is possible we will unwind our allocation to emerging-markets local-currency bonds or may even use it as a funding source for an increased allocation to emerging-markets equities.

Additionally, since we’ve owned this position—from the beginning of August 2009 through June 30, 2013—it has returned around 7% annualized, in line with our conservative expectations.

It seems like an opportune time to harvest some losses from many of my clients’ emerging-markets stock positions. Do you have a recommendation for an alternative, low-cost position for Vanguard FTSE Emerging Markets ETF (VWO) that would be suitable for a tax swap?

Our Litman Gregory investment advisors had similar opportunities to harvest tax losses for our private clients where appropriate. We did some work and were able to get comfortable with the iShares Core MSCI Emerging Markets ETF (IEMG) as a tax swap for VWO. We looked at expenses, geographical exposure, trading, and liquidity as some of the considerations, so that would be one option to consider, along with the unique circumstances of your clients’ tax situation and amount of losses—and their CPA or tax professional should be involved in the decision as well.

Another option to consider is the iShares MSCI Emerging Markets Index ETF (EEM). However, we prefer the much lower-expense IEMG because it’s possible that after doing the swap this may end up being a longer-term holding—if prices rise rapidly and you don’t want to sell it and realize a capital gain to swap back into VWO.

More broadly, can you speak to what goes into the decision process that makes you hold a position as opposed to selling and re-establishing it at a lower basis?

The two key elements to our top-down decision process when constructing and managing our portfolios are 1) our five-year return outlook for various asset classes, and 2) the 12-month downside risk thresholds for each portfolio, with more conservative models having smaller downside risk thresholds. Our tactical allocation approach is based on these longer-term time horizons because we don’t think we or anyone can consistently predict what markets are going to do over short-term periods, because markets are driven by a lot of day-to-day noise, unpredictable and random events, and short-term investor sentiment.

So, when an asset class that we own is selling off in the short term, what do we do? One idea is to get out of the way and sell it, and then re-establish the position at a lower price point. Sounds good in theory, but of course that assumes we will get the opportunity to buy it back at a lower price than where we sold it. And that we will have the foresight to act on that opportunity. We aren’t comfortable with that assumption. (E.g., maybe we’d be expecting further market drops so we’re still sitting on the sidelines waiting for even lower prices to buy, but instead the market reverses course and heads higher. Do we buy or wait for another reversal, which may or may not ever come?) The bottom line is that it’s an approach that just doesn’t fit with our investment discipline. We think we’re much more likely to end up being whipsawed trying to do that, rather than sticking to our longer-term analytical horizon and approach.

Having said that, if we view the risks to have changed meaningfully—so that our assessment of the potential 12-month downside loss for a portfolio changed meaningfully—then we might sell even as an asset class is sharply falling in price. This was what happened in mid-September 2008, when our assessment of the macro environment and the risk that a global financial crisis was unfolding led us to quickly and sharply reduce our equity risk exposure even after stocks had already declined significantly from their highs of the year. But that is a rare example.

Typically, as long as the investment is performing consistent with our expectations across a range of scenarios, we will not try to short-term time the market. Instead we will hold and assess whether the price decline has created a sufficiently compelling opportunity to add to our position at the lower prices.

So the key for us is making accurate assessments of the potential shorter-term risks and longer-term returns for each asset class in our portfolio over a range of scenarios and potential outcomes. If we have built the portfolio with diversified risk exposures and return drivers—consistent with each portfolio’s particular risk objective—then short-term market dips shouldn’t lead us to conclude that we need to sell a position to “get out of the way” of potential further downside. In that way, we should protect ourselves from getting sucked in to chasing the herd market action and remain focused on the long term, letting “time arbitrage” work for us.

BONDS AND BOND FUNDS

PIMCO Unconstrained appears to be very heavy in derivatives exposure. I know you’ve assessed their ability to manage counterparty risk before. But with just around five major bank dealers backing all of these esoteric products, and recent heavy outflows for the flagship Total Return Fund, are you at all concerned about your exposure to the firm?

As the question notes, we have investigated and addressed PIMCO’s counterparty risk several times in the past, and we remain comfortable and confident in their ability to manage that potential risk. We are not concerned about our exposure to PIMCO overall or the Unconstrained and Total Return funds specifically in this regard.

During the recent rise in interest rates, PIMCO Unconstrained performed better than PIMCO Total Return, as we expected. It is also ahead of the Barclays Aggregate Bond Index for the year (as of 6/30/13). But its portfolio does reflect the PIMCO house views and so it was hurt in the second quarter by its positions in TIPS, mortgages, and foreign bond holdings relative to the core bond index. We continue to like the Unconstrained fund as a vehicle that allows PIMCO wide latitude to express their views, both in terms of managing various risks (often via derivatives) and capitalizing on opportunities across the global fixed-income universe.

Regarding the recent outflows, news reports indicate PIMCO Total Return fund had just under $10 billion in outflows in the month of June on an asset base of $285 billion. That’s roughly 3.5% of fund assets in outflows. That is certainly meaningful, but it is not alarming to us—and probably shouldn’t even be surprising given typical investor behavior. We are confident PIMCO has effectively managed and can continue to effectively manage such outflows should they continue. However, while most of their exposure is in highly liquid fixed-income sectors, they do have meaningful exposure to less liquid areas, with TIPS probably the key one at this point. We’re keeping a closer eye on how they manage that exposure going forward.

In your April commentary, you included a table about bond fund risk factors in which PIMCO Total Return was shown as having “moderate” interest-rate risk, yet it really seemed to get hit hard when rates spiked in the second quarter. Was the performance in line with your thinking of a fund with moderate risk?

Yes, we’d say it was definitely consistent with that, but it may be partly a matter of semantics. The word “moderate” does not have a precise quantified meaning in this case, but in the notes to that table that we published in early April we wrote that we were referring to a “fund’s current exposure to that risk factor relative to the core bond index.” (emphasis added)

So by saying moderate interest-rate risk exposure, we meant to convey that we believed PIMCO Total Return had interest-rate risk roughly in line with the Barclays Aggregate Bond Index. Our assessment of that was based on the fund’s duration at that time of a bit less than five years, compared to the index’s duration of slightly above five years. (As of the end of May, PIMCO Total Return’s duration had moved up to slightly above five years, and as of the end of June it had increased to 5.8 years.)

Also, since there was only one risk category above moderate—which we called “meaningful”—we were reserving that higher risk category for funds that had particularly long duration (in absolute terms and versus the Aggregate Index), e.g., if we had owned a long-term Treasury or TIPS fund.

We recently walked through second-quarter performance attribution for PIMCO Total Return with a PIMCO representative and the gist is that the fund’s duration exposure to the so-called “belly” of the Treasury curve (in the five- to 10-year maturity range) hurt it relative to the core bond index, as rates in that part of the curve rose more than at the long end of the curve. But an even bigger drag on the fund’s relative and absolute performance in the second quarter was its TIPS exposure, because TIPS got hit even worse than nominal Treasurys as real yields rose. And a third key factor was the fund’s emerging-markets bond exposure. So the underperformance for the quarter was in part caused by PIMCO’s U.S. nominal Treasury duration exposure, but a larger negative was the TIPS and emerging-markets bond exposures. So the fund did get hit harder than the core bond index when rates spiked, but it wasn’t purely due to the fund’s duration or interest-rate risk exposure.

The fund’s long-term record remains very strong. As PIMCO pointed out in a recent communication to shareholders, the fund has beaten the Barclays Aggregate Bond Index on an annualized basis by more than 200 basis points on average over the past five years since the depths of the financial crisis and has had positive returns over every two-year period during its 26-year lifetime.

You’ve done a lot of work positioning away from the core fixed-income benchmark in your taxable portfolios particularly. Have you done any work on absolute-return-oriented municipal bond funds, or looked at shorter duration muni funds? Core muni funds got hit pretty hard with the bond sell-off in June and they have longer duration than the funds from PIMCO, DoubleLine Total Return, and FPA Income that make up your core bond allocation in your taxable strategies, which is concerning looking forward in a rising-rate environment. Also, could high-yield munis be an option, since you’ve taken on credit risk in funds like Osterweis Strategic Income and Loomis Sayles Bond?

The Fed’s tapering comments resulted in rising yields (and falling prices) in all fixed-income sectors in the second quarter, but muni bonds were particularly hard hit. Muni yields (measured by 10-year AAA yields) were up nearly 60 basis points in the second quarter, and muni returns suffered their fourth worst quarterly loss in over two decades. The three worst periods occurred after Meredith Whitney’s default comments, the market’s collapse at the end of 2008, and Fed tightening in early 1994.

The recent rise in interest rates is not impacting our fixed-income positioning, either on the taxable or tax-sensitive portfolios. We have been anticipating higher interest rates for quite some time, though we never pretend to know when or by how much rates will increase. While this recent move in rates was volatile, our five-year scenario analysis has incorporated expectations for higher interest rates to varying degrees and our bond allocations include funds that can perform well in different economic environments. Predicting interest rates is hard, and poorly diversified portfolios or asset allocations that are structured to perform well in only one scenario have often led to poor performance.

So as we’ve covered on numerous occasions, we continue to have a tactical underweight to core bonds (muni and taxable), and an overweight to taxable absolute-return-oriented fixed-income strategies. Examples include PIMCO Unconstrained (that we own alongside muni funds in our tax-sensitive portfolios) and in our most-conservative portfolios, floating-rate loans, which can benefit from rising interest rates.

Currently we are not interested in owning short-duration muni portfolios. While they are less interest-rate sensitive, we don’t think you are getting paid enough at current price levels as yields are paltry at 60 basis points. Nor do we want to venture into high-yield munis. First, we are already taking some credit risk in portfolios such as Loomis Sayles Bond (also owned in our tax-sensitive portfolios), and given current valuations we don’t think taking more credit risk is prudent.

So in tax-sensitive portfolios, we continue to think the intermediate part of the muni curve is the most attractive part of the market. We will continue to evaluate our portfolio positioning, balancing risk and reward in a manner that is consistent with our longer-term investment discipline. We also invest with active managers we think can add value relative to the muni benchmark.

In a rising-rate environment, what level does inflation have to be at in order for an allocation to TIPS to make sense?

In answering this question, we would like to remind investors that higher inflation generally leads to higher rates. Higher rates equate to falling share prices for bonds, but especially TIPS, which are a long duration asset. Any hint that inflation is rising would almost certainly lead to a decline in prices, as prices and yields move in opposite directions. In this sense, TIPS funds can actually provide the opposite of what many investors may be expecting, where rather than protecting against inflation, investors could in fact be hurt by it due to falling prices. In our stagflation scenario, we have inflation reaching 7% over our five-year investment horizon. In that same scenario, we also estimate that 10-year Treasury rates will be 6%. While shareholders will benefit from a higher coupon as TIPS income resets periodically with inflation, that higher coupon will be offset by price declines. So even in this high inflation scenario, we estimate that TIPS returns will be flat to mildly positive. So higher inflation in and of itself is not a good barometer of TIPS returns.

MANAGER DUE DILIGENCE

This past quarter you removed Longleaf Partners Fund from your portfolios and the Recommended List. Can you provide any additional details behind your decision?

By way of background, we downgraded and removed Longleaf Partners Fund from our active portfolios in the second quarter. For more information regarding this sale, as well as the similarly timed sale of two other active equity funds, please see our due diligence updates published in early June.

In many cases when we decide to remove a fund from our portfolio, there is a balancing act. On one hand, our natural inclination as Litman Gregory research analysts is to provide all of the details of our analysis underlying the decision. On the other hand, there is the possibility of potentially jeopardizing our ability to gain deep access to other managers for due diligence purposes in the future or inadvertently going against our commitment to acting as a responsible, high-quality shareholder.

We will certainly not hesitate to remove a manager if, based on our ongoing due diligence and analysis, we find that we can longer maintain a high level of confidence in them and in their ability to outperform over the long term. But we do hesitate to publicly air the details of such decisions, just as we don’t publish detailed reports on funds and managers that we do research on but ultimately do not end up investing with or recommending.

We do this because we don’t want to create a disincentive for managers to give us the access we require to do our full due diligence out of a potential fear on their part that if we come to a negative conclusion based on our qualitative assessment that we will make a point of publicly discussing it. It’s important to note here that we’re not talking about a situation where we think a manager is engaging in unethical or illegal behavior, rather we’re referencing a normal situation where our due diligence leads us to question whether the manager has a sustainable investment edge or where we can’t confidently identify such an edge.

Also, when we are in the midst of a serious reassessment of a manager or have significant fundamental concerns about elements of their investment process, team, culture, firm, etc., we don’t want to give the manager a roadmap or telegraph what our specific concerns may be. To do so, we think, would give the managers the opportunity to “game” their answers to our questions (i.e., tell us what they think we want to hear). Crafting our questions for managers so that they don’t obviously reveal our key concerns is part of the skill and art in what we do.

In the case of Longleaf, a firm that we had invested with for 20 years, we began to seriously question and actively revisit our investment thesis in mid-2012—the culmination of a period where they had made several major stock-picking mistakes. Our due diligence process was lengthy and intense and included face-to-face meetings with key investment decision-makers on the fund, as well as many internal research team vetting sessions, discussions, and debates where we hashed out our perspectives on the key issues. While we didn’t provide the details of those discussions in public, we did indicate on two quarterly research team conference calls (in both August 2012 and April 2013) that we were in the process of seriously reassessing our conviction in Longleaf, in addition to a few other funds that we held in portfolios.

As our process came to a conclusion this spring, we were ultimately unable to positively resolve many of the critical questions we had with regard to the implementation and execution of Longleaf’s investment process—questions revolving around their assessment of fundamental business risk, valuation/margin of safety, and company management. Our previously high level of confidence in them was not reaffirmed, so we made the decision to sell.

The number of manager choices in the larger-cap domestic stock area of your Recommended and Approved funds list is dwindling. Are you planning on doing work in the domestic equity space to add managers?

With the recent removal of three large-cap funds from our Recommended List, our bench is definitely thinner. Additionally, strong performance of three Recommended funds—Touchstone Sands, BBH Core Select, and FMI Large Cap—has resulted in asset growth, and subsequently these funds have recently closed to new investors. We are keenly aware of this issue, and deepening the bench is among our research priorities. Without getting into specific names, there are a handful of domestic equity funds that are in the early stages of due diligence. We also continue to be particularly focused on emerging-markets equity funds. In case anyone missed it, our most recent addition to the Recommended List was in April, when we added Nuance Concentrated Value, an all-cap value equity strategy.

—Litman Gregory Research Team (8/1/13)

© Litman Gregory