The Weekly Speculator

We wrote last week on the eve of the FOMC meeting which resulted in the surprising decision not to reduce the current program of treasury and mortgage security purchases. What was to our eyes equally surprising was the volume and strident tone of the commentary that was issued following this release, ranging from the arrogant to the outraged as if anything really meaningful had changed. At most the FOMC has delayed its decision by a number of months, which may well be ill-advised (at least to our way of thinking) but cannot be said to have radically changed the economic or investment landscape.

Contrast the reaction to this meeting to the complete ignorance shown exactly five years ago when Chairman Bernanke took the lonely and courageous decision to place the FRB’s balance sheet in the line of fire. As can be seen on the attached chart it took several weeks of substantial asset purchases before the term “quantitative” started to appear in a large number of news stories. The reason for this is that everyone was too busy focusing on the crisis itself rather than the FRB’s role in crafting a solution.

The fact that the FRB’s balance sheet had never before been used in this manner made most people forget that it had the legal and functional ability to conduct these operations, as Chairman Bernanke had explained at length in his November 2002 speech on deflation. Even when people realized what was taking place, denial that it would prove effective and dire warnings about both the risk of an FRB bankruptcy and hyper-inflation drowned out saner arguments that suggested that the massive intervention in credit markets was likely to succeed.

In the case of the ECB’s introduction of the LTRO in 2011 there was no shortage of attention, but the vast majority of it was strongly opposed to its implementation and denied that it would form the basis for a workable solution to the Eurocrisis. Almost three years later this looks like a foolish viewpoint, since although many of the long term fiscal issues remain in place the foundation for a meaningful recovery is becoming apparent.

The point we would make is that in our experience policy that is either ignored or rapidly rejected often proves to be much more significant than episodes like last Wednesday that may seem incredibly important at the time and even lead to rapid price adjustments across asset markets (which certainly happened in this case) but ultimately do little to change the balance of risk and opportunity going forward.

From our perspective current US monetary policy was inappropriately loose before the meeting and would have remained so even if a modest tapering of bond purchases had been implemented. The current FOMC may have exceeded our estimation of the degree to which they would be willing to stretch reality to justify their current policy but we had already incorporated the concept that they were exhibiting clear signs of “recovery denial”. If anything “permanent” was achieved last week it was to put the FRB’s remaining credibility in peril should economic data point to an acceleration of activity in the US.

Despite the strong reaction to the statement, the direct relevance of this decision on large portions of global asset markets is open to question. Although we are not surprised to see the bond market rally in the immediate aftermath of the decision, there remains the central problem that fixed income returns continue to badly lag those available in equities across developed markets. The odds of another wave of capital re-allocation out of bonds between now and the end of the year seem high.

With regards to emerging markets the notion that the US threat to taper has been a major influence on this portion of global markets is hardly credible. Emerging market equities started their long period of under-performance over two years ago, a time period that has been punctuated by a remarkable wave of monetary generosity by central banks of the entire developed world. Although two years ago the Euro-crisis obscured the domestic origins of the deterioration of local EM equity markets, subsequent months have provided ample data-points to justify the reticence of investors to continue to pour money into this area.

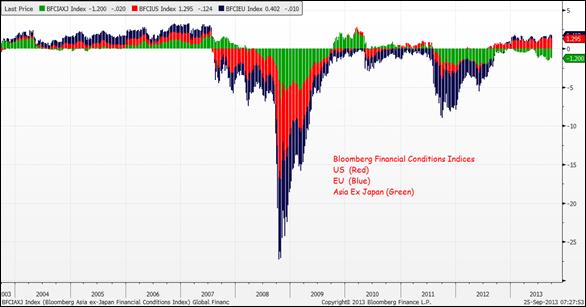

Indeed it is interesting to note that a marked divergence has taken place between the financial conditions (as measured by the regional Bloomberg Financial Conditions Indices) currently present in the US, Europe and Asia ex Japan. To remind readers, these aggregate readings use volatility, credit and swap spreads to produce a simple reading of Financial Conditions, with zero representing “normal” and each integer a single standard deviation.

As can be seen on the chart on the next page the Bloomberg US Financial Conditions index is currently at a very healthy +1.31 having set a 19 year high of 1.48 at the start of August. Somewhat bizarrely the FOMC stated that deterioration in financial conditions was a justification for continuing with bond purchases but certainly with regards to the US it is hard to see any basis for this view. In the Eurozone conditions remain comfortably positive at 0.412, and although this is substantially lower than the almost giddy readings in the US this is a healthy reading for the current stage of Europe’s recovery and compares with that seen in the US prior to breaking out above 0.50 towards the end of 2012.

By contrast since falling into negative territory in August 2011 the Bloomberg Asia ex-Japan Financial Conditions index has spent the vast majority of time below zero. It remains substantially negative at -1.26, and was as low as -1.63 at the end of August. Although we are yet to see a “crisis” reading in 2013 that would be triggered by the index falling below -2 (the index fell to -2.3 in October 2011) we are not that far away from this level. Furthermore the exclusion of Latin America from this index means that if anything, this measure probably understates the strains felt across the emerging market complex. This does bring up the possibility that the FOMC’s mentioning of financial conditions was an oblique reference to emerging markets, which the committee felt needed to be included in its policy decision without wishing to explicitly recognize this was the case.

Whatever the exact truth to the matter (which we suspect will never be known) as the 3rd quarter draws to a close the massive outperformance of US and developed market equities over other asset classes will once more come into consideration. Although some will no doubt be tempted to “bottom fish” in the underperforming bond and emerging market complexes, given the good fundamental foundations for the divergence of performance we would expect the trend to remain intact. We continue to be hopeful that the US equity market can break out further into blue sky territory and although we note that the SPX index is yet to break free of the 1,700 level economically sensitive sectors have performed well in recent sessions and should be expected to continue to do so.

Moreover the RTY index has recorded a series of marginal new all time highs in recent weeks and looks likely to continue to edge higher while European equity markets have enjoyed an excellent 3rd quarter that was largely undisturbed by the August decline in US equity markets and we would continue to favor these areas going forwards.

Please note that we will revert back to our regular Thursday publication next week.

The information provided herein represents the opinion of Marketfield and is not intended to be a forecast of future events, or a guarantee of future results. This report is for informational purposes only, is not an offer to buy or sell any specific security, and is not intended to provide specific investment advice because it does not take into account the differing needs of individual clients. This report is based upon information that Marketfield Asset Management LLC believes to be reliable, but no representation is made by Marketfield Asset Management LLC as to its completeness or accuracy. This report is not a complete analysis of every material fact concerning any company, industry or security. Marketfield Asset Management LLC assumes that it will be read in conjunction with any other available reports and data. Opinions expressed herein are subject to change without notice. No investor should rely on the views, opinions or any suggestions contained herein. Investors are advised to consult with their own individual advisers on their specific situation before taking any action based on any information contained in this report.

© 2013 Marketfield Asset Management LLC. All rights reserved. Charts are courtesy of Bloomberg, Inc.