Young and old alike celebrated Halloween last week, albeit in soggy fashion in much of the nation.

The good news, according to some media sources, was that the Obama administration was finally able to demonstrate a successful “web launch.” The orange-themed White House was dramatically decorated for Halloween with giant black spider webs and the First Couple, in full costume, greeted hundreds of delighted trick-or-treaters.

Unfortunately, trick-or-treating was postponed for safety reasons in many areas as a fierce storm moved across the middle of the U.S., with extremely high winds up to 50 mph in 12 states and several tornado reports. Sadly, there was some loss of life, as hazardous flooding accompanied the often violent wind and rain.

Watching the weather stories on Halloween, my thoughts turned to another storm of note, Hurricane Sandy, which had its first anniversary, coincidentally, last week. It was hard not to make this leap, as the major networks had been running numerous one-year-later retrospectives on Sandy.

I did not need a retrospective, however, as our family resides on the coast in Connecticut and our town saw more than its fair share of damage from the winds, flooding and tidal push. I have numerous firsthand anecdotes about both the day of the hurricane and living in its immediate aftermath, but thankfully they all relate more to property damage and serious inconveniences than loss of home or life.

I will spare you the details, but one concerns a 90-foot tall White Eastern Pine tree which came down on our property, shaking our entire old stone house, narrowly missing the structure by 20 feet. Another involves a good friend who lives on the beach in a small bungalow he had purchased a few years back, for which he had the foresight to raise onto a 3-4 foot concrete above ground foundation. Unlike many of his immediate neighbors, he was able to survive the tidal flooding with minimal damage.

The clichés surrounding nature and the weather are many when they come to the financial markets, but like clichés from many areas, they often have a basis in fact.

No, “trees do not grow to the sky,” as we learned in dramatic fashion that day of Sandy.

And, yes, proper planning for “worst case” scenarios can help you “weather the storm.”

Which is why at Flexible Plan Investments, Ltd., we are enthusiastic proponents of dynamic, actively managed strategies that put diversification and risk management at the forefront. Such an approach can adapt to any market environment and help portfolios reduce downside risks while not sacrificing return, which becomes especially important in those times of volatile and uncertain markets.

It has been written in this space on several occasions that it is important to “keep one eye on the exits” in any market environment, no matter how enthusiastic the trend and sentiment might appear to be on the surface. This could be particularly relevant at this point in time, as the “frothiness” of the markets appears to be capturing the attention of some serious market participants.

About a week ago, Blackstone Advisory Partners Vice Chairman Byron Wien said in a CNBC interview, "There are signs of speculation out there, and that makes me worried."

While we are not in the prediction business, it was interesting last week that small-cap stocks (as represented by the Russell 2000) were down over 2% on significant volume in an otherwise benign market which saw the S&P register its fourth straight week of gains. Small- and mid-caps have led the way higher this year (a whopping 29.5% gain for the IWM ETF) and often are viewed by technicians as “the canary in the coal mine.”

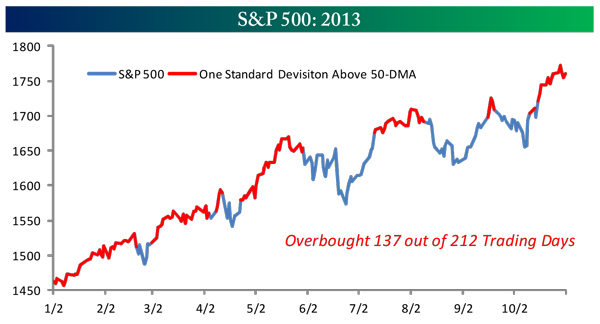

However, as our friends at Bespoke Investment Group point out, even though the S&P 500 Index might be technically in “overbought” territory currently, it has a way of staying overbought for long periods in bullish trends. Bespoke adds that “so far this year, the S&P 500 has closed the day at overbought levels on 137 out of 212 trading days (65%),” with only relatively small pullbacks along the way.

Source: Bespoke Investment Group

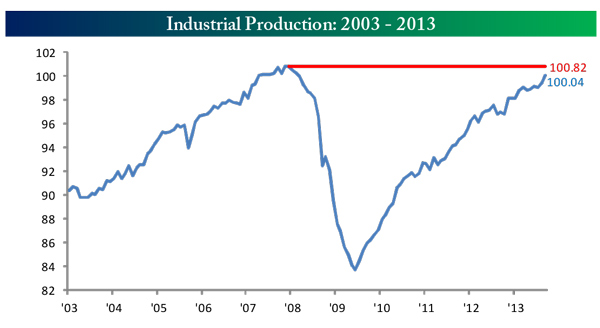

While many continue to attribute the market’s 2013 performance primarily to the Fed’s continued “QE-4-ever” policy, and the diminished threat of imminent tapering of bond purchases, Bespoke emphasizes the continued strong trend in Industrial Production, which is less than 1% off of all-time highs seen in 2007. In a week which saw mixed results again in over twenty economic releases, the week started off and finished on positive notes on Industrial Production, the Chicago PMI report, and ISM Manufacturing data.

Source: Bespoke Investment Group

While there are plenty of worry points for market participants over the remainder of 2013—lack of clarity over the Fed’s short-term intentions, the continuation of Washington’s budget/debt ceiling infighting, the poor employment numbers, an inconsistent earnings season with lackluster revenue growth, and uncertain consumers fed up once more with their elected officials—history is leaning in favor of a continued positive end to the year for the financial markets.

Although P/E’s are starting to become a bit elevated (16.7 vs. historical norm of 15.3) and bearish sentiment is down to a fairly extreme level (just 16.5% according to the Investors Intelligence survey of investment newsletter writers), November and December have been historically positive market months, and even more so during very bullish calendar years.

Bespoke mentions that in the 35 instances of YTD market gains through October of over 10%, the markets have averaged a final two month performance of nearly 5% with positive returns 82% of the time. The case becomes even stronger when the market has gained over 20% through the end of October, though the data sampling is far smaller.

But whether or not we see clear skies through the end of the year as many predict, or some unanticipated stormy weather in the short term that a few others are calling for, we think we will stick to our discipline and leave the forecasting to others.

All the best,

David Wismer, Director, Communications, for Flexible Plan Investments, Ltd.

© Flexible Plan Investments