What’s Wrong with PIMCO?

The Trouble with Owning Bond Funds as Opposed to Individual Bonds

When Federal Reserve Chairman Ben Bernanke first talked about reducing or tapering the Federal Reserve’s asset purchase program back in May of 2013, the market response was dramatic. Investors started fleeing bonds, causing bond prices to drop and bond yields to rise.

In a rising interest rate environment, the net asset value (NAV) of fixed income mutual funds falls as rates rise. This often leads to shareholder redemptions (they want out!), forcing these bond mutual fund portfolio managers to sell bonds in an unfavorable market.

An investor holding individual bonds doesn’t have this pressure. He or she can hold their bonds to maturity, rather than selling them when their prices have fallen, and get repaid the full principal amount of their bonds when they mature. Since a bond fund shareholder owns shares in a mutual fund instead of individual bonds, the bond fund investor is stuck; the shareholder either has to exit the fund at a less than ideal time, or suffer through the NAV declines. In a fixed income mutual fund, there is no guarantee or assurance of holding bonds to maturity and hence no assurance of repayment of principal.

In addition, owning individual bonds provides the investor full transparency and control as opposed to fixed income mutual funds, which may hold a variety of instruments including stocks.

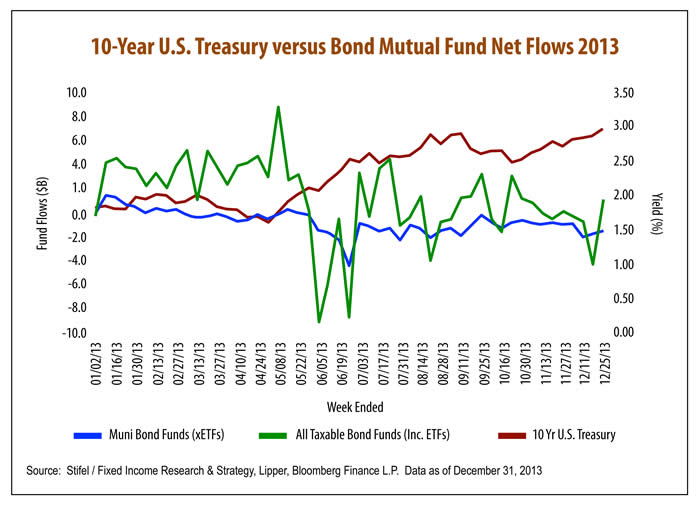

The graph (Figure 1) shows the rise in bond yields that began in May (red line), and the money that flowed out of municipal bond funds (blue line) and taxable bond funds (green line).

The Turmoil at PIMCO

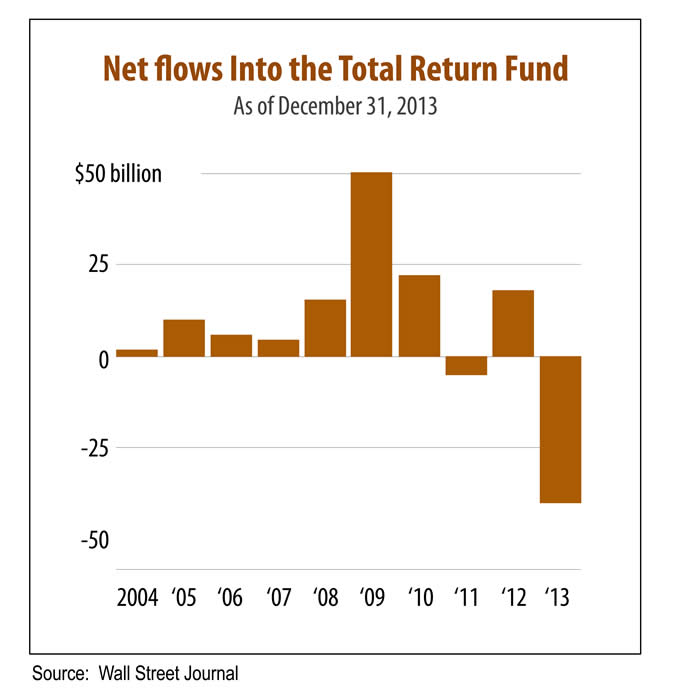

Shareholder redemptions were particularly acute at PIMCO (Pacific Investment Management Company), the nation’s largest bond fund manager with approximately $1.9 trillion of total assets under management. The widely held PIMCO Total Return Fund, managed by the firm’s founder, Bill Gross, suffered record net redemptions of $41.1 billion in 2013, or almost 15% of the fund’s total assets. Last year, PIMCO Total Return Fund had a negative 1.92% return. Firm-wide, PIMCO is trying to reverse net mutual fund redemptions that totaled $30.4 billion in 2013. That, by the way, was the biggest drop among the ten largest mutual fund families. The graph (Figure 2) illustrates this dramatic turn in PIMCO’s fortunes.

Trouble at the Top

In January 2014, a leadership shakeup at PIMCO was triggered by the sudden resignation of Chief Executive Officer Mohamed El-Erian, who shared the role of Chief Investment Officer with Bill Gross. El-Erian was considered to be Gross’ heir apparent.

Interviews with people close to Gross and El-Erian suggest that many factors were involved in the departure: a high-pressured work environment that turned less collegial over the past year, a deteriorating relationship between the two senior executives, and certain decisions by Gross that confused employees.

In late January, PIMCO announced a new chief executive, a new president and six deputy investment officers. PIMCO has yet to choose a new heir apparent for Gross, who is 69 years old. That highlights two risks for PIMCO fund holders that are characteristic of firms with leadership turmoil. The first risk is whether or not the new management team will be successful. The second risk has to do with whether or not Mr. Gross will cede control.

Many institutional investors have begun to review their use of PIMCO’s services, citing the management shake-up. The Florida Retirement System Pension Plan has put PIMCO on a formal watch list. Also, the California Public Employees’ Retirement System, known as Calpers, said in an email, “we are monitoring the issue and will keep our board aware of any changes.”

In a recent interview, Gross said that he would be stepping back from some investment duties, although others at the firm are skeptical that he will give up any control. According to PIMCO employees and former employees, when Gross establishes an investment thesis, he does not appreciate dissenting views. El-Erian told Gross to be less combative with employees and to give others more leeway in investment decisions. At the end of the summer 2013, Gross agreed to be less confrontational, but according to PIMCO executives, the change did not last.

On March 18th, Morningstar, the mutual fund research firm, downgraded PIMCO’s stewardship grade to C from B (A being the highest and F being the lowest). In addition, one of the categories used for Morningstar’s analyst ratings that looks at the priorities of the firm was downgraded from positive to neutral. According to an article by Morningstar analysts, Eric Jacobson and Michael Herbst, “Those changes reflect a higher degree of uncertainty around the firm’s recent personnel changes….” Morningstar analysts may downgrade their ratings for PIMCO’s mutual funds after a review of the firm’s regulatory issues, board quality, manager incentives, fees and corporate culture.

PIMCO has extensive derivative use in its funds. Morningstar tabulated the securities held in the Total Return Fund as of September 2013, and there were almost 20,000 of them. Because the derivatives and swaps that PIMCO uses are relatively opaque, it is hard to deduce the strategy by scrutinizing them directly.

At South Texas Money Management (STMM), one of our specialties is fixed income separately managed accounts. We are currently constructing fixed income portfolios with short average maturity, individual bond ladders – staggering maturity dates so as to not get locked in to a particular maturity for a long time period, utilizing taxable or tax‐exempt bonds, as appropriate. And in the meantime, the investor is receiving steady income. In addition, we are buying short to intermediate individual bonds, which are less vulnerable to rising interest rates than longer bonds. At STMM, most of our purchases are in the new issue market, and there are no markups associated with those purchases. STMM only buys fixed income bonds that are A rated or higher and our fixed income portfolios average credit rating is AA or higher. Therefore, the risk of default in municipal bonds that are purchased by STMM is minimal.

© 2014 South Texas Money Management, Ltd. ("STMM”). All rights reserved. No part of this report may be reproduced or distributed without permission. STMM assumes no liability in connection with the use of this report. This report is not an offer or solicitation to buy or sell securities or investment services and is provided for informational purposes only. Information is subject to change without notice, and STMM shall have no duty to update the information contained herein. Past performance is no guarantee of future results. There is a possibility of loss. All material and information presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Individual bonds may not be appropriate for every investor and bond funds may be used by STMM when the fixed income allocation of an account is not sufficient to warrant individual bond purchases.

© South Texas Money Management