Long-Term Potential Intact, Despite Near-Term Weakness

Emerging market equities as an asset class have been underperforming developed market equities for more than three years, though they continue to maintain the lead over 10-year returns. The divergence in returns between emerging and developed markets widened sharply in 2013, when the prospect of reduced capital inflows heightened investor concerns about slower economic growth in the emerging countries. The fragile fiscal and current account balances of select emerging countries, as well as increased political instability, have also made these markets appear riskier and less attractive to international investors.

In assessing the investment opportunities in the emerging world, we believe that these economies are likely to sustain faster growth rates when compared to the developed countries, for the next few decades. The growing industrialization, which is the result of economic reforms implemented over the last two decades as well as increased export opportunities created by globalization, should allow these countries to lift living standards further. Many of these countries have a relatively young population, which assures both a sustainable labor supply and a large base of increasingly affluent consumers. Many businesses in these countries have matured significantly, expanded their scale of operations and strengthened their management capabilities. As a result, they are in an advantageous position to benefit from the growth in domestic consumption while continuing to exploit overseas opportunities.

At the same time, the emerging economies are unlikely to regain the high growth rates that many investors had mistakenly assumed were the norm rather than the exception. The apparent end of the commodity super-cycle could restrain the export-led growth in several Latin American countries as well as South Africa. Even exporters of manufactured goods, such as China and Mexico, would likely find it difficult to sustain growth as lower-cost competitors arise. These countries may have to retool their economies to facilitate greater balanced growth, which relies more on domestic consumption. Countries such as India that have relatively more balanced economies need to address the infrastructural and other capacity constraints that are fueling inflation risks. Until that happens, these countries would likely have to maintain higher interest rates, which would restrict growth.

In addition, several emerging countries have structural problems that have led to unsustainable current account imbalances as well as wider fiscal deficits and rising debt levels. After these problems became acute during the third quarter of 2013, some countries came up with short-term fixes that have been somewhat successful. Nevertheless, these countries will likely have to launch deeper reform efforts to reduce costs for domestic producers and consumers, make government spending less wasteful, and lower the reliance on foreign capital.

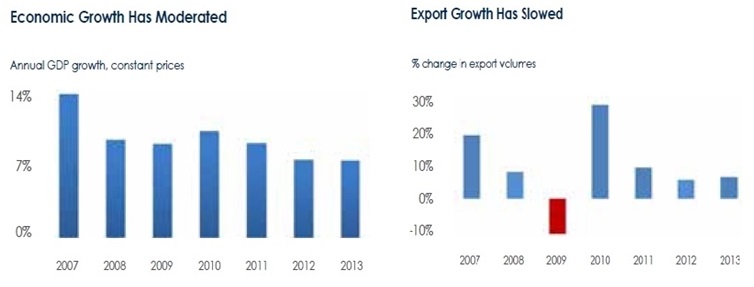

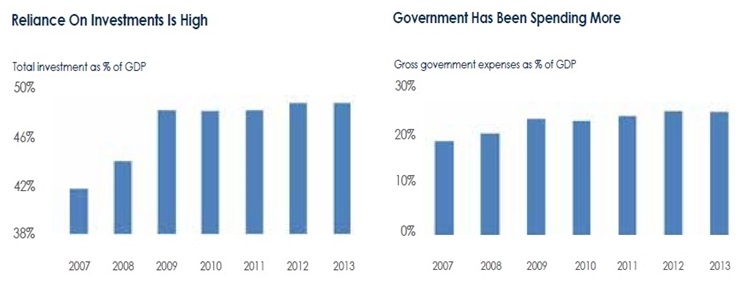

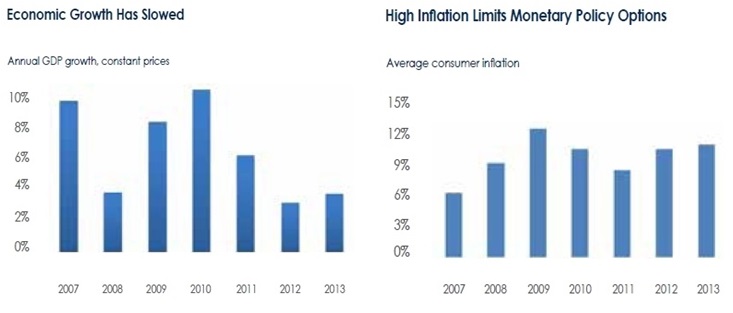

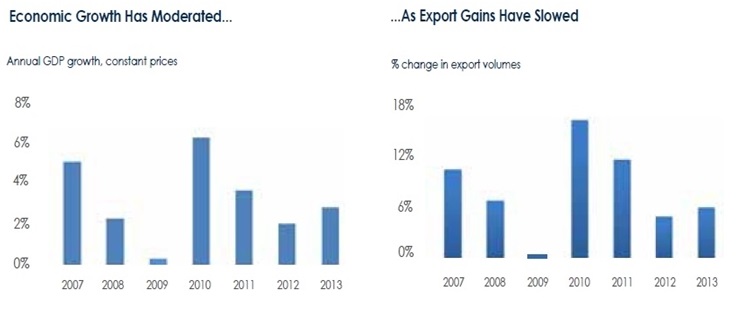

China: Managing a Difficult Transition to Sustainable Growth

The slowdown in China is a top concern for many investors now, as lower growth in the world’s second largest economy could have aftereffects on the prospects for several other countries. Nevertheless, a successful transition from an export-led economy to a more domestic consumption-driven model could make the country’s future growth more consistent and sustainable.

Positives

• The political leadership appears to be convinced about the need to reduce the reliance on exports, even at the cost of short-term growth.

• The government, central bank, and other regulators appear more conscious of the potential risks from asset price bubbles in the housing market, as well as the rapid expansion of unregulated banking channels.

• Domestic consumption growth continues at a healthy pace, as retail sales expanded nearly 12 percent during the first two months of this year. The growing popularity of online retailing, as well as communication and entertainment services delivered over the internet and cellular networks, offers significant growth opportunities for businesses.

Challenges

Challenges

• Fewer new jobs, a slower pace of average income growth, or further rise in living costs could lead to social and political unrest.

• Regulatory efforts to curb excessive credit growth and the growth of unregulated banking, if not managed prudently, could lead to a credit contraction and weaken the economy further.

• Slower economic growth could increase potential loan losses for the banks, though the government is expected to strengthen bank capital in such a scenario.

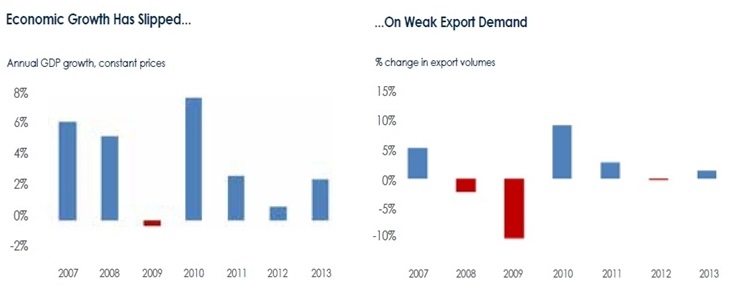

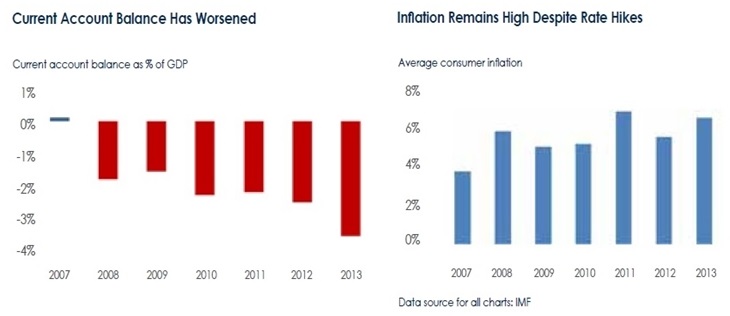

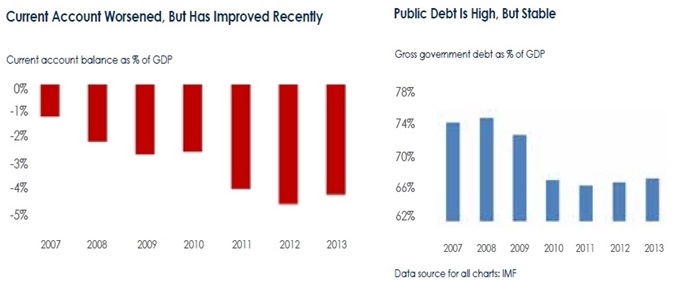

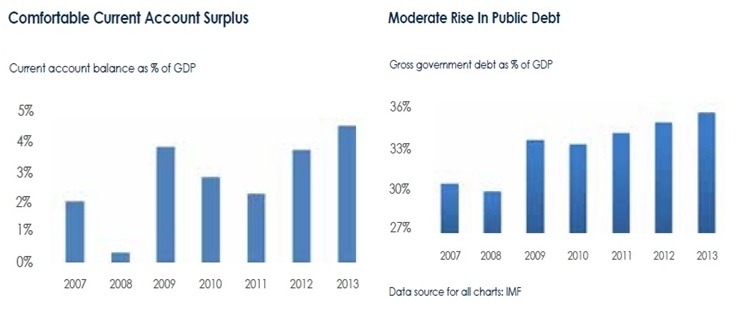

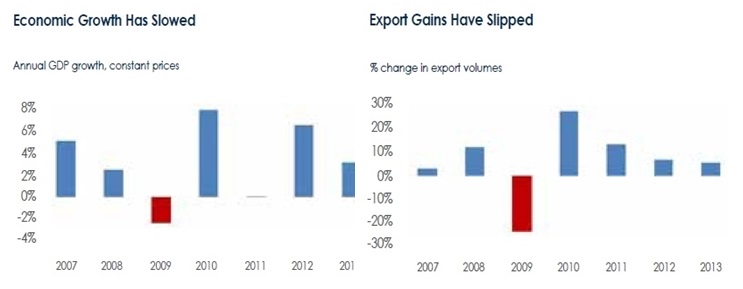

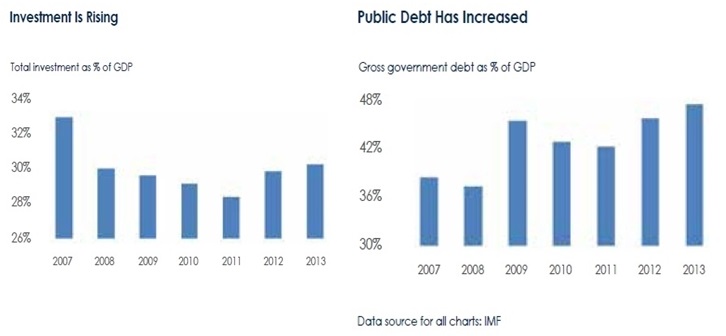

Brazil: In Need of Deeper Structural Reforms

Brazil has seen one of the worst growth slowdowns among emerging countries after the commodity super-cycle started waning. Despite the Brazilian Real decline, exports are yet to see a meaningful revival. Persistent inflation risks have forced the central bank to repeatedly hike interest rates, though the measures have restrained domestic demand further.

Positives

• A populous country with relatively high average income levels when compared to other emerging economies and classified as an upper middle-income country by the World Bank, Brazil has the potential for sustained expansion in domestic demand.

• The relatively mature industrial base, expanding capital markets, and geographical location place the country in a good position to take advantage of regional demand across Latin and Central America.

• The large energy reserves discovered recently could transform Brazil’s external trade composition as and when energy exports start.

Challenges

• Brazil remains one of the highest cost locations for domestic producers and consumers in the emerging world. The recent protests against high living costs highlighted the seriousness of the problem.

• The government’s desire for more control over energy reserves and other valuable resources have caused production delays and have raised questions about governance and political interference.

• Populist government policies of the past have weakened government finances, and similar policy expectations could limit the ability to introduce reforms.

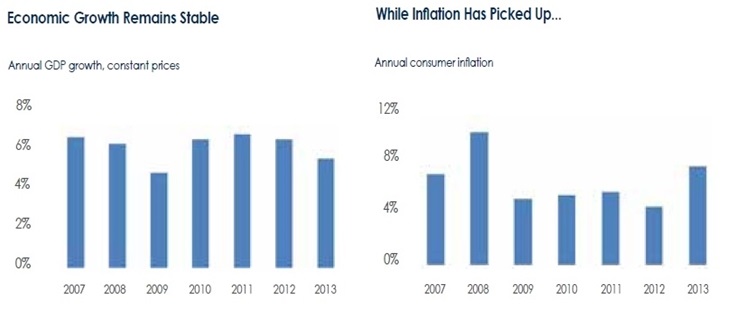

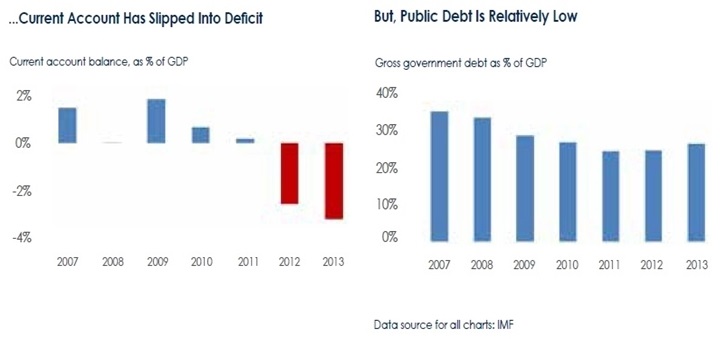

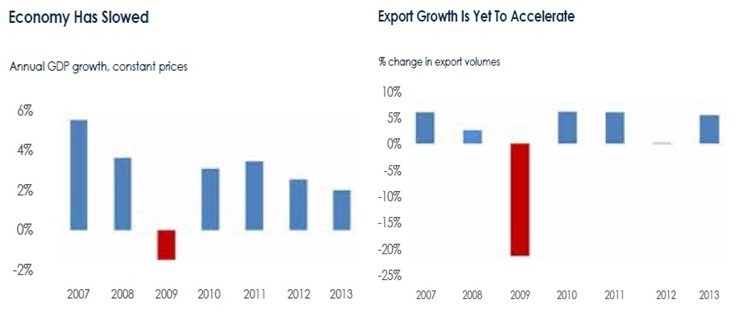

India: Hope Rises For A Proactive Government

India was one of the worst hit among emerging markets during the third quarter of 2013, as concerns about a wide current account deficit sent the Indian Rupee sharply lower, -13 percent versus the U.S. dollar in 2013. The short-term measures such as import controls on gold and interest rate hikes initiated by the government and the central bank have narrowed the current account deficit since September 2013. While economic growth still remains subdued, the likelihood of a new pro-growth federal government after the elections scheduled in May 2014 has lifted market sentiment.

Positives

• India has the most appealing demographic profile among large emerging economies, which could potentially sustain domestic demand-led growth for several decades.

• A more decisive federal government could push through some of the much needed reforms to sustain long-term growth.

• The country boasts relatively mature and transparent corporations with good management track records.

Challenges

• A fragmented political structure with strong regional parties makes it difficult to achieve policy consensus.

• The large majority of the population is still dependent on the farm sector, and has very low income levels. Generating new jobs on a large scale in the manufacturing and services sectors would be a challenge for future governments.

• Insufficient infrastructure and long delays in project approvals continue to dissuade businesses from making large-scale industrial investments.

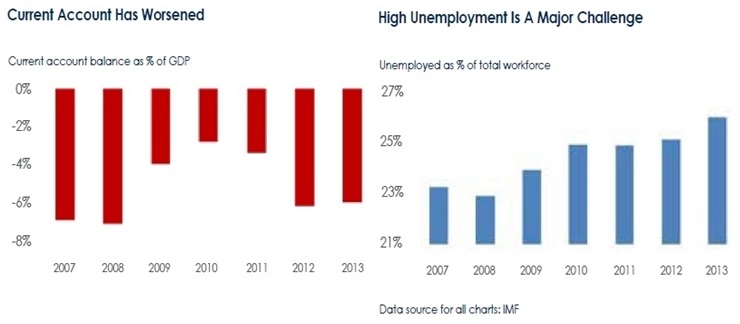

Indonesia: Growth Potential Remains Promising

After being an investor favorite for several years, Indonesia fell out of favor as slower export growth and a sustained rise in imports widened the country’s current account deficit in 2013. The central bank was forced to hike interest rates by 1.75 percentage points to 7.5 percent as the currency plunged 26 percent against the U.S. dollar 2013. The trade account balance improved during the last quarter of 2013 and aggregate economic growth has not declined as much as feared.

Positives

• The most populous country in South East Asia with a relatively young population averaging 25 years of age, Indonesia has the potential to see strong growth in domestic demand if the political and policy environment remains favorable.

• The political system has shown growing maturity in recent years, which could ensure economic policy stability in the future.

• Rich in natural resources, the country should continue to benefit from increased export demand.

Challenges

• The government policy of encouraging exports of processed or semi-processed industrial materials could restrict exports in the short-term, though it should benefit the economy in the long-term.

• Underdeveloped infrastructure could discourage global manufacturers from investing in Indonesia.

• Perceptions about high levels of corruption and inefficient government bureaucracy could also limit industrial investments.

South Korea: Sustaining Growth in a Maturing Economy

South Korea is the most developed among the major emerging markets and, if it sustains the current growth pace, could even graduate to the developed markets classification. The country has a comfortable current account surplus as well as healthy fiscal deficit and public debt levels. However, the economy is still predominantly export-oriented, which leaves the country vulnerable to fluctuations in global demand and currency devaluation by other exporting countries.

Positives

• South Korea has a developed industrial base with growing capabilities in product development.

• The country has mature corporations with large international footprints, capable of competing across markets.

• South Korea boasts healthy current account balances and government finances, which have kept the currency relatively stable even when most emerging market currencies turned very volatile.

Challenges

• As it moves higher in average income levels, the country will likely see a gradual erosion in cost competitiveness and could lose manufacturing jobs to lower cost countries.

• The transition to an economy more oriented towards domestic consumption could be a slow process, and would require policies that would not be very favorable for exporters.

• A few large industrial groups, or chaebols as they are known in Korea, control a substantial share of the economy, which could discourage competition and innovation.

South Africa: Gateway to Future Growth on the African Continent

South Africa is one of the oldest emerging markets, with the country having long standing trade ties with Europe as a major exporter of industrial materials and precious metals.

Though gold exports, once the primary driver of South Africa’s economy, has dwindled, the country is still the leading producer of metals such as platinum and manganese.

Growing economic inequality has led to labor strikes recently and, coupled with lower commodity prices, has dulled investor interest in the country.

Positives

• Companies in South Africa are well positioned to benefit from consumer and industrial demand in other countries in the region, which have some of the fastest economic growth rates in the world.

• South Africa still has large deposits of minerals and metals that have the potential to attract investments in the future.

• South Africa has a fairly developed financial system, with relatively mature capital markets.

Challenges

• Exports are still skewed towards commodities and need broader diversification to ensure sustainable growth.

• The threat of asset takeovers by the government could discourage potential investors in mining.

• Very high unemployment rates could keep the risk of labor agitations high.

Thailand: Constrained by Volatile Politics

One of the Asian Tigers that saw rapid industrialization during the final two decades of the last century, Thailand was the epicenter of the last major financial crisis in the region in 1997.

The country’s economy is far less vulnerable to external shocks now, but highly confrontational politics continues to often unnerve investors. Elections held in February this year have been invalidated by the Constitutional Court, and fresh elections are expected to be held in the coming months.

Positives

• Thailand, the world’s largest exporter of rice, has a fairly diversified export basket.

• One of the major tourist destinations in the region.

• Thailand has relatively developed industrial capabilities and is a regional manufacturing base for products such as automobiles.

Challenges

• An aggressive style of politics limits the scope for consensus building, which is often seen as essential in a democratic environment.

• The perception of corruption and political favoritism towards businesses could limit foreign investment inflows.

• Nearly half of the population is still engaged in farming and related activities, and income inequalities between urban and rural areas remain wide.

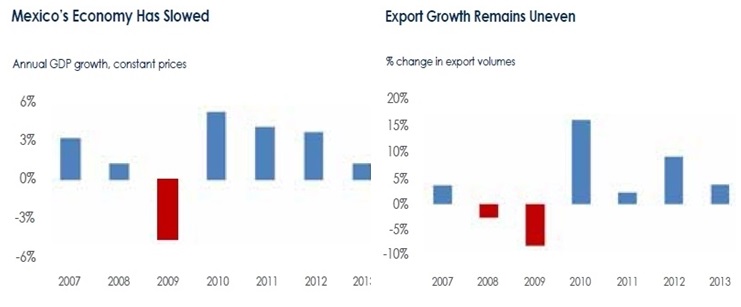

Mexico: The Promise of Bold Reforms

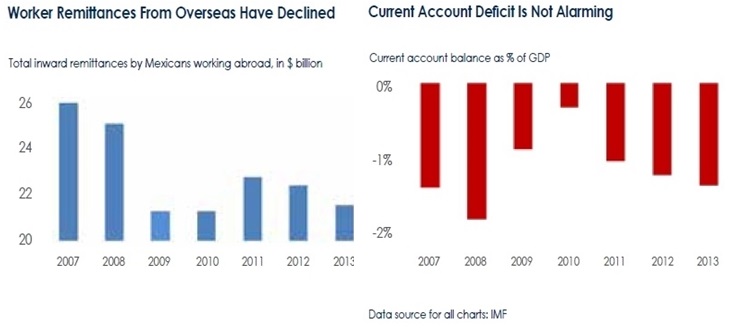

After several decades as the source of cheap labor for the U.S., Mexico has gradually emerged as a cost-efficient manufacturing location. However, the decline in remittances by Mexicans working abroad has hurt domestic demand growth as net migration to the U.S. has slipped to almost nil.

The government of President Pena Nieto has launched a wave of economic reforms to vitalize Mexico’s industry and increase competition. Success of these reform measures could significantly influence the country’s future economic growth potential.

Positives

• Close geographical proximity to the U.S. makes Mexico an attractive manufacturing location for global businesses, especially when labor costs are increasing in Asia.

• The country’s industrial capabilities have seen appreciable gains in recent years.

• The government’s recent reform measures demonstrate political will to restructure inefficient sectors such as energy.

Challenges

• Mexico’s economic fortunes are closely linked to industrial and consumer demand in the U.S., which is the country’s largest export market.

• The decline in remittances by Mexicans working abroad is likely to restrict economic growth until the manufacturing sector generates more jobs.

• Violence related to the illegal narcotic drug trade continues to hold back the industrial development of select regions.

Conclusion

In summary, the macro-fundamental reasons for the relative underperformance of emerging markets are well-known now. Problems such as current and fiscal imbalances, structural inflation, and the risk of asset price bubbles that some of these countries have been facing are serious and deserve effective policy responses. Nevertheless, the risk of a deeper financial and economic crisis triggered by these problems appears to be low. At the same time, countries that have taken proactive steps to address their macro-economic fragilities could regain investor interest and potentially outperform other countries that have deeper structural problems.

This article is for informational purposes only. This article is not intended to provide tax, legal, insurance or other investment advice. Unless otherwise specified, you are solely responsible for determining whether any investment, security or other product or service is appropriate for you based on your personal investment objectives and financial situation. You should consult an attorney or tax professional regarding your specific legal or tax situation. The information contained in this article does not, in any way, constitute investment advice and should not be considered a recommendation to buy or sell any security discussed herein. It should not be assumed that any investment will be profitable or will equal the performance of any security mentioned herein. Thomas White International, Ltd, may, from time to time, have a position or interest in, or may buy, sell or otherwise transact in, or with respect to, a particular security, issuer or market on our own behalf or on behalf of a client account.

FORWARD LOOKING STATEMENTS

Certain statements made in this article may be forward looking. Actual future results or occurrences may differ significantly from those anticipated in any forward looking statements due to numerous factors. Thomas White International, Ltd. undertakes no responsibility to update publicly or revise any forward looking statements.

(c) Thomas White International