Risk means different things to different people - danger, uncertainty, opportunity or thrill. In reality, risk arises in any situation where there is more than one possible outcome of differing value to the individual.

Individuals vary widely in how well they tolerate financial risk. Some investors don’t like risk so they stick to investing in CDs or savings accounts, no matter how low the returns. Others swear by stocks, even if they have been knocked down by previous losses. Many people insure their home and contents but not their life. We all differ in how we manage and protect out finances.

Many people believe that risk tolerance varies and is subject to market conditions. However, the evidence suggests that our risk tolerance is an enduring personal trait that is typically set by early adulthood. Like other aspects of our personality, it is determined by genetics and life experiences. It may decrease slightly with age. It may also change as a result of major life events. Divorces, for example, may reduce one’s tolerance for risk (and marriage). But mostly, our risk tolerance is stable.

While some investors (and their advisors) believe risk tolerance changes with major events such as a stock market correction, typically it is an investor’s perception of risk that changes, which results in a change in their behavior.

At the moment, many investors are buying stocks with elevated P/E ratios. Prices are going up a lot faster than corporate earnings and the risks are getting bigger. Yet people are still buying stocks. Investment markets are booming and people are under-estimating risk.

In contrast, in bottoming markets, risk perception is typically at its highest and some investors, out of fear of losses, sell undervalued stocks in favor of cash. This is what many investors did during the Global Financial Crisis.

A media continually in search of dramatic headlines does not help. When stock markets fall, the media’s emphasis is on doom and gloom. Pop quizzes casting investors as panicked lemmings are featured. The focus is always on the money that has moved rather than on the funds that have stayed. Changes in behavior are usually portrayed as evidence of a collapse in risk tolerance.

In such situations, investors’ advisors too often attribute their clients’ decisions to sell risky assets to a drop in their risk tolerance. But the reality is more likely to be that advisors recommended risky investments to clients who did not understand the risks they were getting into - until they eventuated.

This is what happened to countless investors during the GFC. Not only did many of their advisors fail to explain the risks their clients faced in buying up stocks and sometimes borrowing heavily, many advisors didn’t assess their clients’ risk tolerance in the first place to help determine which investments might fit with their risk preferences.

FinaMetrica’s own data supports the view that risk tolerance is stable.

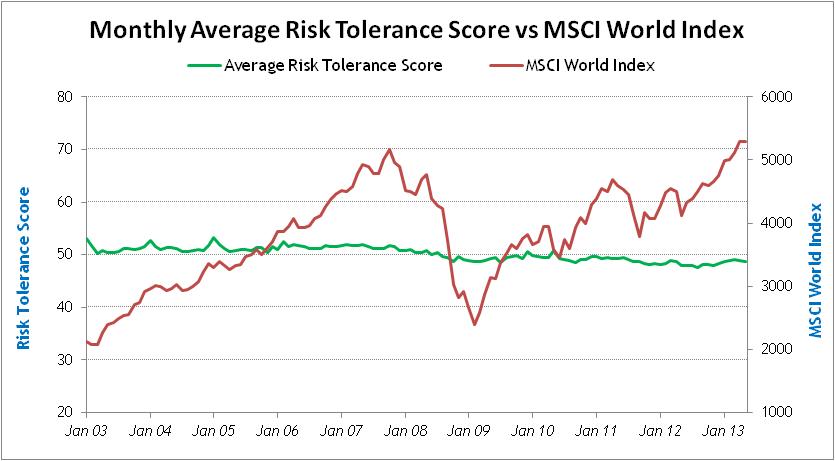

Evidence from the 700,000 risk tolerance tests completed by investors over the past 15 years reveals that risk tolerance scores have been remarkably stable. Average monthly scores, mean 50 and standard deviation 10, from 2003 to 2013 are shown in the chart below.

The risk tolerance data shows a remarkably flat green line[i]. Several other point to risk tolerance being a stable psychological trait[ii].

Perhaps the most convincing was a test/retest study carried out by researchers at the University of Western Australia, the University of Queensland and the University of Newcastle. In this study, the same individuals had been tested in the 2003-07 bull market and then retested in the 2008-09 bear market. The average score decreased only 1.9[iii], less than one fifth of a standard deviation.

What this all means for investors is that risk tolerance is one of the few aspects of their life that is unlikely to change over time. This makes it a solid foundation for conversations about risk generally. Moreover, investors should understand their risk tolerance before making any decisions on how their assets should be invested. Understanding how well you tolerate risk is essential in managing your financial affairs and understanding the consequences of your decisions.

The stability of risk tolerance is also good news for financial advisors. Advisor and client share a common interest: neither wants to experience big losses or the relationship to end in disappointment. If increased risk perception is the likely Achilles heel during a market sell-off, then advisors can influence the client’s risk perception through education about market risk. This needs to be done in advance when clients are not in the highly stressed state brought on by an unexpected collapse in the value of their investments.

Readers wishing to assess their own risk tolerance can complete FinaMetrica’s test at www.myrisktolerance.com. The test costs $55. It takes just 15 minutes to complete and a detailed four-page risk tolerance report is available immediately.

About the Author

Geoff Davey is a cofounder and director of FinaMetrica. He is the creator of the FinaMetrica Risk Profiling system and manages FinaMetrica's ongoing research activities and relationships with academic and research institutions. Geoff is a member of the Australian Financial Planning Association, an international member of the US Financial Planning Association and a member of the US FPA's Asia Pacific Focus Group.