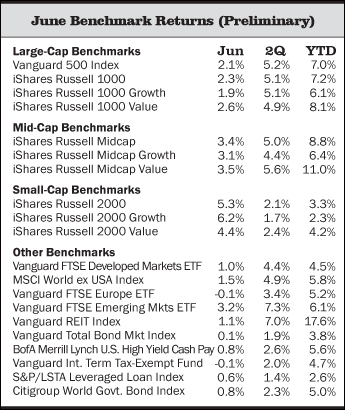

Asset classes across the board rose in the second quarter despite lackluster global economic growth, an uncertain outlook for global monetary policy, and geopolitical tensions in Ukraine and Iraq. The Vanguard 500 Index fund (our S&P 500 proxy) was up 5.2% for the quarter and 7% for the year to date, after rising more than 2% in June. Smaller-company stocks again lagged larger-caps as they have so far this year, though they posted a very strong 5.3% gain in June. Our small-cap benchmark rose 2.1% for the quarter and is up 3.3% so far this year. Our portfolios are tactically underweight small caps based on their historically high valuations and so the year’s relative under performance has been a positive for our results.

In economic news, U.S. GDP data for the first quarter was revised further downward to - 2.9%, marking the largest drop since the first quarter of 2009. Expectations are for growth to rebound in the second quarter (after a very harsh winter depressed activity in the first part of the year); however, the fact remains that the economic recovery continues to be subpar. Other indicators were more positive, including continued improvements in the labor market, though wage growth is still very slow.

Developed international stocks were positive as the European Central Bank took further easing steps as it combats concerns about long-term deflation risk while Japan’s Prime Minister Shinzō Abe continued his multi-pronged effort to generate healthy inflation and boost Japan’s economy. Despite these efforts, though, both economies are mired in uncertainty. After a poor first quarter, emerging-markets stocks rallied. Our emerging-markets benchmark rose 7.3% for the quarter and is now up more than 6% for the year. Among larger emerging markets, China’s growth outlook remains a source of investor uncertainty while India’s newly elected prime minister was viewed favorably among investors and the country’s stock market staged a huge second quarter rally.

Core bonds shared in the gains as Treasury prices rose and bond yields continued to fall—a surprise to many investors—with the 10-year Treasury yield ending the quarter at 2.53%, down from 3.04% at the end of 2013. The Federal Reserve remained consistent in its message: while gradually scaling back its monthly bond purchases (announcing another $10 billion reduction in June) it has also indicated a lack of urgency in raising rates based on what it sees currently on the jobs and inflation fronts. The Fed updated its growth projections in June, revising slightly downward its expectation for 2014 growth, and while most measures show signs of inflation ticking up, it remains below the Fed’s target. For the quarter, we saw positive bond fund performances across the board as the Vanguard Total Bond Market (our core bond benchmark) was up 1.9%. High-yield bonds again posted strong gains as investors sought higher yields. Floating-rate loans (a tactical allocation in our conservative portfolios) and municipal bonds rose as well.

The Lack of Concern Could be Cause for Concern

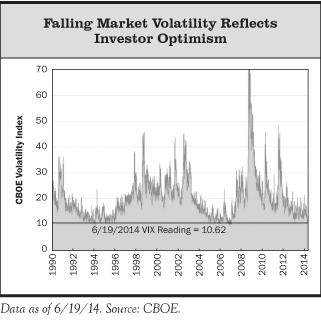

One thing that stands out about the past quarter amidst the record-setting highs of the S&P 500 is the very low stock market volatility. By late June (6/19/14), the VIX, a volatility index that measures expected 30-day volatility of the S&P 500, had dropped to 10.6, a level last seen in February 2007. (The recent VIX readings were in the first percentile of lowest daily observations since 1990, and within two points of the VIX’s record low on 12/22/93.)

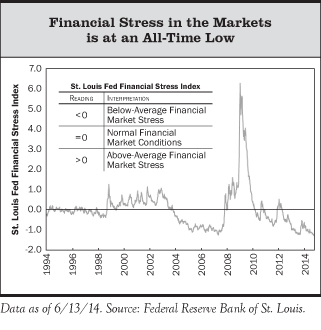

Another indicator of the markets’ state of calm is the recent all-time-low level of the St. Louis Fed Financial Stress Index, which measures the degree of financial stress in the markets based on a compilation of 18 weekly financial market data points.

While low volatility and high stock prices reflect the market’s apparent lack of concern about risk—likely buttressed by a belief that the Federal Reserve will continue to support financial markets with accommodative monetary policy—this seeming complacency is causing us some near-term concern because it suggests a market more vulnerable to negative surprises.

The more investors are expecting and positioning portfolios for a benign or optimistic environment—using leverage and pouring money into riskier and/or less liquid assets to ramp up their near-term returns—the more likely it is that there will be a negative shock relative to these market expectations, and the more disruptive it will likely be if and when the shock happens. The "Investor Speculation" chart below shows margin debt as a percentage of stock market value near all-time highs, suggesting that investors are indeed positioned in accordance with a rosy outlook.

This shorter-term concern about potential market vulnerability is also consistent with what continues to be our longer-term view that stock market valuations in aggregate are discounting too optimistic an outlook. In sum, our view is that markets continue to be too dependent on central bank largesse, too short-term focused, and too complacent about the risks and imbalances that remain in the global economy in the aftermath of the financial crisis.

We are not predicting that there must be a near-term market shock, just that the investment risk is heightened when markets are complacent. A low VIX does not necessarily imply an impending volatility spike or stock market correction. Volatility can remain subdued for long periods of time (as seen in the VIX chart). And at least one investment manager we respect highly, PIMCO, is arguing for just such an outcome. As part of their “new neutral” secular (three- to five-year) investment thesis, PIMCO foresees a low growth/low volatility environment for the next several years, and they have positioned their fixed-income portfolios accordingly.

But what might disrupt the market’s calm? Unfortunately, geopolitical shocks are always a risk and one that we don’t try to anticipate. But even with this year’s events in Ukraine and the sectarian violence in Iraq (to name just two), markets in general have remained relatively calm (except for some short-term, temporary stock-market declines). To the extent there is a sustained geopolitical flare-up, we’d expect U.S. Treasurys and other high-quality bonds to benefit from a more sustained investor flight-to-safety at the expense of global stocks and other riskier asset classes. If a fear-driven market decline is severe, it could present a good long-term buying opportunity, enabling us to shift some of our lower-risk/defensive tactical investments back into riskier but higher-returning stocks.

Inflation vs. Deflation

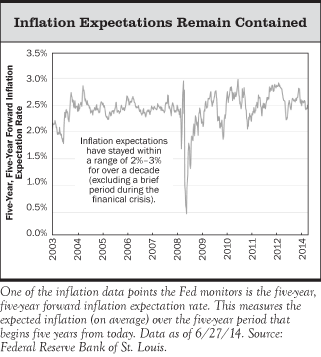

Away from the geopolitical realm, a deflationary or inflationary surprise could be disruptive. In Europe, core inflation fell to a year-over-year rate of 0.7% in May (headline inflation, which includes food and energy, was only 0.5%). Several smaller European countries are in outright deflation. However, the markets have been worried about European deflation for a while now, and the latest CPI number was in line with consensus expectations. Meanwhile in June, as we discuss below, the European Central Bank initiated new monetary policies in an attempt to help reflate the economy, and also signaled that it would act more aggressively, if necessary, to prevent a deflationary shock in Europe from happening. (This echoed its actions in late July 2012, when ECB President Mario Draghi assured the markets it would “do whatever it takes” to prevent a breakup of the European monetary union, triggering a huge rally in European stock and bond markets).

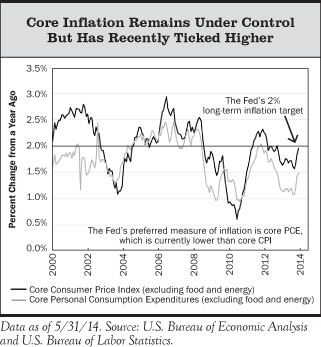

In the U.S. economy, deflationary and inflationary risks are more balanced. While inflation, and importantly, inflation expectations remain under control, it has recently been ticking higher. Core CPI hit 2% on a year-over-year basis in May. The inflation measure the Fed focuses on, the core personal consumption expenditures price index, rose to 1.5% in May, which is still below the Fed’s long-term inflation target of 2%. In her most recent policy statement, Federal Reserve Chair Janet Yellen expressed little concern about the recent uptick, referring to the short-term inflation data as “noisy.” But several economists have pointed to the acceleration in the inflation rate over the past year as a potential harbinger of higher inflation to come. For example, core CPI has increased at a 2.8% annualized rate in the past three months, compared to the 2% trailing 12-month rate. (Our base case five-year scenario view is that neither extreme inflation nor deflation will take hold, though this could change, of course. As we discuss below, it is an area we are closely monitoring.)

Central Bank Policy

Inflation obviously bears watching, and no one is watching it more closely than the central banks. But that doesn’t mean the financial markets will necessarily agree with central bankers’ assessment of the inflation risks or that the central banks’ assessment will be correct. (As with most economists, central bank economic forecasts have been pretty lousy.) Central bank policies have been a huge driver of financial market returns in recent years, e.g., driving down bond yields and pushing up stock market valuations (P/E multiples). Monetary policy remains a key uncertainty, and its impact—both intended and unintended—on the markets and the economy must be taken into account in managing investment portfolios.

Based on the latest actions and statements of the two key central banks in the global economy—the Fed and the ECB—the most likely scenario is for monetary policy to remain accommodative for a while. (The Bank of Japan is also in a very accommodative mode and China’s central bank relatively so.) At its latest policy meeting on June 18, the Fed, as expected, continued on its path of tapering its monthly bond purchases (quantitative easing) by another $10 billion, and remains on course to end the program this fall. But Janet Yellen, while emphasizing that Fed actions will be economic-data-dependent, gave no indication the Fed is planning to raise the federal funds policy rate anytime soon. This is consistent with market expectations of a first rate hike sometime around mid-2015. Markets also expect the pace of rate tightening, once it begins, to be slow. But this generally sanguine take means the markets are susceptible to an inflation surprise that leads to more aggressive Fed rate hikes.

As noted earlier, the ECB took action in June to provide additional liquidity to Europe’s financial system in response to ongoing concerns about very low growth and inflation there. While it stopped short of full-blown quantitative easing, at his press conference on June 5, 2014, ECB President Mario Draghi said the bank was ready and willing to do more, “Using all unconventional instruments within its mandate in order to further address risks of too prolonged a period of low inflation. . . . Are we finished? The answer is no.” Given the weakness in the European economy, we think the ECB is likely to ultimately follow in the footsteps of the Fed, the Bank of England, and the Bank of Japan and embark on quantitative easing, and its June actions appear to open the door a bit wider for such a step. The International Monetary Fund also urged the ECB to consider undertaking “large scale” bond purchases (i.e., quantitative easing) if low inflation persists. Clearly, central bank policy is yet another indication that we remain far from a normal economic environment. Global monetary policy remains a significant influence on financial markets, and a material source of uncertainty.

Update on our Macroeconomic Outlook

We’ve touched on just a few specific big-picture topics. Overall, our macro view and assessment of the risks and returns across the major asset classes has not changed meaningfully since last quarter. We continue to see the U.S. economy—and the global economy more broadly—on a slow path of recovery from the 2008 financial crisis. Private sector balance sheets continue to strengthen (reflecting the U.S. household and financial system deleveraging that has occurred since 2009). This lessens the odds of another financial crisis and is a key support for the recent increase in our estimate of fair value for the stock market as we discounted a less stressed macro environment.

Significant risks remain, however, concerning central bank policy, European deflation, and a disruptive unwinding of China’s credit bubble, among others. More recently, we are becoming more sensitive to inflation risk, given the uptick we have seen in the United States over the past quarter and the strengthening (although still not strong) labor market, which at some point should start pressuring wages higher. Improved wage growth should be beneficial for consumer spending and the overall economy (and Yellen has explicitly said she wants to see higher wage inflation), but it would also likely put pressure on corporate profit margins and therefore earnings.

Based on Fed statements and behavior, we continue to see the risk of the Fed overshooting in terms of accommodative monetary policy, keeping rates “lower for longer,” and allowing inflation to move above their 2% long-term target. This strikes us as a bigger risk than the Fed tightening too soon and snuffing out the tepid economic recovery. But it isn’t clear how or when the markets will react if the Fed remains accommodative in the face of a sustained rise in inflation above 2%. And the markets’ reaction will almost certainly influence the Fed’s behavior as well. Fed credibility has been critical to market stability, and markets have reacted positively (or at least neutrally) to the most recent Fed statements and actions. But that credibility may be increasingly called into question if the market perceives the Fed is remaining inactive in the face of inflation or other potentially worrisome economic indicators.

This view was recently expressed by economist and strategist David Rosenberg, “This Fed is erring on the side of uber-accommodation far too long and is playing with fire. If this forecast proves prescient, it is difficult to believe that at some point inflation expectations won’t become unhinged and send long-term bond yields substantially higher” (David Rosenberg, “Breakfast with Dave,” Gluskin Sheff Research, June 19, 2014). Or as European hedge fund manager Sir Michael Hintze more colorfully put it, “The central bankers very much believe they can control the exit [from their current accommodative policies]. But remember, their balance sheets have never been as large. They also believe that their pronouncements will be listened to forever . . . Maybe they can keep control, but if people stop believing in them, all hell will break loose” (Ralph Atkins, “Financial Markets: Hurrah Before the Storm,” Financial Times, June 13, 2014).

Our Portfolio Positioning

In the meantime though, the music is playing, the punch bowl is out, and the equity markets are dancing to the central banks’ tune. This party may continue for several more months or quarters. But we don’t think relying on central bank generosity is a sound investment strategy over the five-year horizon on which we base our tactical portfolio decisions.

While we think inflation risk has increased at the margin, we have not made any portfolio changes because we don’t view the change in inflation risk as significant enough, nor is our conviction that an inflationary scenario will play out high relative to other potential macro scenarios we consider. Importantly, we have already positioned our balanced portfolios for the likelihood of rising interest rates, consistent with some increase in inflation.

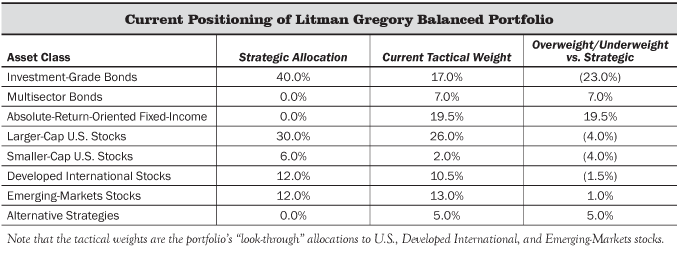

Overall, our balanced portfolios continue to be somewhat defensively positioned, with a moderate underweight to stocks and equity risk (primarily U.S. stocks and smaller caps due to their unattractive valuations) and a significant underweight to core bonds and interest-rate risk, relative to our long-term strategic allocations. These tactical allocation decisions are based on our asset-class risk and return estimates, which in turn are driven by our assessment and analysis of economic fundamentals and market valuations. As noted earlier, we’ve upgraded our view of the fundamentals over the past few quarters. But valuations—for U.S. stocks at least—remain unattractive, in our view. (See our First Quarter 2014 Commentary for our analysis of U.S. equity valuations and expected returns.)

With that big-picture backdrop, we will now walk through our current portfolio positioning in our balanced (stock/bond) accounts in more detail. (Our specific Balanced portfolio allocations are shown in the table below as an example. We don’t hold fixed-income or alternative strategies funds in our most aggressive portfolios, which are 100% invested in equities.) (See our accompanying fund positioning article for highlights from many of the specific mutual funds we are using to implement our asset allocations.)

Fixed-Income

ABSOLUTE-RETURN-ORIENTED AND MULTISECTOR BOND FUNDS

Our fixed-income allocations are not based on a particular short-term view of the timing or pace of Fed rate hikes, but our base case scenario assumes rates will move higher over the next five years. Therefore, more than half of our fixed-income exposure in our balanced accounts is in funds that have significant flexibility to manage their inflation and interest-rate risk (i.e., duration) and other risk exposures as compared to “core” investment-grade bond funds, which are managed against the benchmark Barclays Aggregate Bond Index.

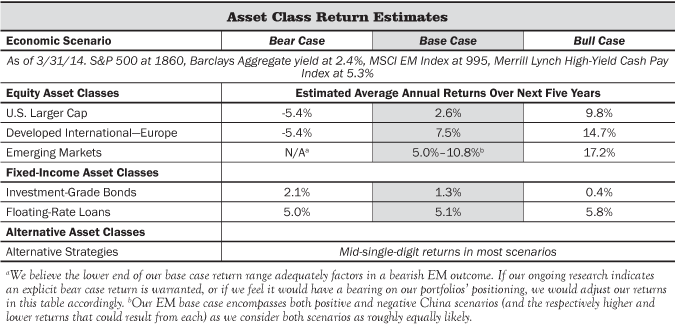

With a current yield of just 2.3%, we estimate the core bond index is likely to return somewhere in the range of 1%–2% annualized over the next five years in nominal terms (i.e., before inflation). We expect our more flexible fixed-income funds, run by skilled and experienced managers, to outperform core bond funds and the bond index over our five-year horizon. Among our key fund holdings in this area are Loomis Sayles Bond, PIMCO Unconstrained Bond, and Osterweis Strategic Income.

CORE BOND FUNDS

While our five-year expected returns for core bonds are quite low, core bond funds still play an important risk management role in balanced (stock/bond) portfolios. These funds serve as a hedge against an economic downturn, deflation, or some other macro shock that would lead to increased risk aversion and falling prices for riskier assets amidst a flight to quality. Even in the absence of that type of scenario, the diversification benefits of owning some core bond exposure was seen in the first half of the year as interest rates reversed course from 2013 and declined, surprising most market participants and providing a tailwind to core bond funds relative to absolute-return-oriented fixed-income strategies.

We own two core bond funds run by proven managers, DoubleLine and PIMCO, with excellent long-term records of risk management and alpha generation. We like the additional portfolio diversification benefit we get from owning both funds as they have different approaches to core fixed-income investing.

FLOATING-RATE LOAN FUNDS

In our most conservative portfolios, we continue to own positions in diversified higher-quality floating-rate loan funds in order to further benefit from and protect against rising short-term rates and unexpected inflation. In a rising-rate environment, traditional fixed-coupon bondholders see the value of their bonds drop as rates rise. If rates rise substantially, this could lead to a meaningful loss of principal. Floating-rate loans on the other hand are largely unaffected by rising rates as they have variable interest rates that “float” regularly to reflect changes in current market rates. We expect to earn solid returns (~5%) from these funds over our five-year horizon across our range of macro scenarios. The floating-rate loan positions are funded from our strategic allocation to core bonds. While we assume floating-rate loan funds won’t perform as well as core bond funds in a shorter-term “risk-off” scenario (where investors flock to assets perceived as safer), we like the longer-term risk/return trade-off, and our stress tests give us confidence that the overall downside risk for the portfolios that hold floating-rate loan funds is in line with our objectives.

MUNICIPAL BOND FUNDS

Our before- and after-tax return expectations differ significantly enough for our core bond holdings that we recommend investors in the 18% or higher tax brackets substitute municipal bond funds for some or all of their core taxable allocation. Municipal bonds are having a strong first half of the year, with gains that seem to be driven by improving fiscal outlooks for local and state government. At the same time, muni bond issuance remains subdued (perhaps due to continued austerity efforts as well as concerns about federal support to the states). This lack of supply can be favorable for prices in the face of rising investor demand. Risks remain, however, including interest-rate risk as well as headline risk such as what we’ve seen from Detroit, Puerto Rico, and Illinois. We favor active management for our muni bond exposure because, in our view, a combination of higher credit risk from some municipal issuers and price risk associated with higher interest rates make security selection and yield-curve positioning that much more important.

Stocks

We remain underweight to stocks versus our long-term strategic target, although we increased our equity-risk exposure slightly at the end of the first quarter. As we discussed in our First Quarter 2014 Investment Commentary, that move was based on an improvement in our five-year expected returns for stocks combined with increased shorter-term risks we saw for our tactical position in emerging-markets local-currency bonds, which we sold to fund the increase to global stocks.

Our tactical underweight to stocks is invested in a mix of flexible bond funds (discussed above) and alternative strategies (discussed below). We assume these investments have much less downside risk than stocks but more downside risk than core bonds in certain stressed scenarios, and we account for this in our overall portfolio risk analysis. So while we have an 8.5 percentage point tactical underweight to stocks in our Balanced portfolio based on simple math, we view our actual tactical equity risk underweight as closer to five percentage points when we take into account the risk factors our tactical positions contribute.

Within our overall global equities exposure, we are tactically underweight U.S. stocks relative to our strategic allocations, and we are roughly fully allocated to developed international and emerging-markets stocks. This is because our low single-digit base-case return expectation for U.S. stocks is not enough to fully compensate us for their risk. Meanwhile, expected returns in the mid- to high-single digits for both international and emerging markets are adequate and we view those markets as trading within a fair value range. (See our expected returns table below.)

U.S. LARGER-CAP STOCK FUNDS

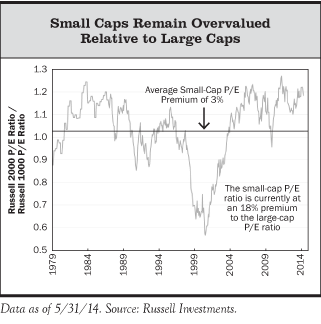

Within our U.S. equities allocation, we continue to be significantly underweight to smaller-cap stocks in favor of larger-cap stock funds. Our tactical underweight to smaller caps is a function of their significant overvaluation relative to larger caps and our expectation of worse downside performance in the event of a broad market sell-off. With regard to valuation, the chart at right shows the small-cap Russell 2000 index trading at an 18% valuation premium to the large-cap Russell 1000 index at the end of May. This is down from 22% earlier in the year as small-cap stocks have underperformed large-cap stocks since then. But it is still near all-time highs and well above the long-term average small-cap P/E premium of 3%.

INTERNATIONAL STOCK FUNDS

As mentioned earlier, we are roughly fully allocated to developed international stocks. This is obviously a very broad and diverse asset class, including countries with widely varying economic fundamentals, let alone individual company idiosyncrasies. But from our top-down perspective, valuations and expected returns appear reasonable and in line with the fundamentals in our base case scenario.

In keeping with our preference for managers focused on stock picking as a primary tool to add value, our international allocation includes several funds with broad mandates that enable them to invest across the globe. We also gain international exposure through Oakmark Global, a concentrated, all cap, value-driven fund that invests in the United States as well as international and emerging markets. (In calculating our portfolios’ exposure to emerging markets—an allocation we discuss specifically below—we take into account that our developed-market international funds typically hold a modest amount of emerging-markets exposure as well, although this will vary over time depending on the attractiveness of the stock-picking opportunities.)

EMERGING-MARKETS STOCK FUNDS

On a strategic long-term basis, we believe emerging-markets stocks should comprise a significant (20%) share of most investors’ total global equity allocation. We’ve explained why in past reports (e.g., Third Quarter 2013 Investment Commentary), but in a nutshell it comes down to emerging markets’ superior long-term growth, demographic, and debt dynamics relative to developed economies. Of course, emerging markets have unique risks as well—as was evident in 2013—but they are manageable as part of a broadly diversified long-term-oriented portfolio. On a tactical basis, given current attractive valuations and our five-year return expectations, we are allocated at or slightly above our strategic targets to emerging-markets stocks.

Over the past six months we have made new investments in two actively managed emerging-markets stock funds: Baron Emerging Markets and Brandes Emerging Markets. These funds employ very different investment strategies—Baron is long-term growth and Brandes is deep value. So in addition to our expectation that both funds will outperform the broad emerging-markets index over time, we are getting excellent diversification between them. (We also continue to like the additional diversification we gain by investing in Parametric Emerging Markets, an enhanced index-like fund that actively reduces the country-concentration risk found in market-cap-based index funds.)

Alternative Strategies

The final broad area of exposure in our balanced portfolios is to alternative strategies funds. These include lower-risk strategies such as merger arbitrage and event-driven arbitrage. These strategies are intended to generate long-term returns that are better than core bonds, with much lower downside risk and volatility than equities and relatively low or no correlation to the stock and bond markets. In other words, we expect them to provide diversification and risk management benefits, while generating expected returns around the mid-single digits. Beyond this long-term strategic rationale for owning alternatives, on a tactical (five-year) basis we believe they can generate returns competitive with or better than stocks across our most likely scenarios. That has definitely not been the case over the past five years, as stocks have been in a roaring bull market, a trend we do not view as sustainable in our base case scenario.

Concluding Comments

Our view of the macroeconomic landscape has improved over the past several quarters as the U.S. and global economies have continued to slowly recover from the 2008 financial crisis. As such, we increased our exposure to stocks (primarily international) earlier in the year. However, we remain underweight to U.S. stocks, with a tactical overweight to flexible fixed-income funds and lower-risk alternative strategies. Despite our more positive fundamental outlook, we have not been more aggressive in adding back to equity risk because the U.S. stock market remains overvalued in our analysis, except in our optimistic scenarios. Given the risks and uncertainties that we still see from the aftermath of the financial crisis, we are not willing to assume the optimistic case plays out over our five-year tactical time horizon. But it might, and we do give it weight in our range of potential outcomes.

If our base case scenario of continued subpar economic growth and a lower market valuation multiple plays out, our more defensive positioning should perform well in absolute terms and also relative to our strategic benchmarks. If the optimistic scenario plays out, our portfolios should perform even better in absolute terms because we do have meaningful exposure to stocks and are fully allocated or slightly overweight to international and emerging-markets stocks. If a bearish stock market scenario plays out, our Balanced portfolio (e.g., with a 10%, 12-month loss threshold) will likely experience negative returns over the shorter term, but our defensive tactical positions should hold up much better than equities on the downside. And a severe market sell-off would provide us the opportunity to add back to our stock exposure at much more attractive valuations and higher expected returns.

As we consider the range of potential outcomes, we are comfortable with our positioning and the risk and return trade-offs we are making. Unfortunately, in the current low-volatility, low-yield, high-P/E environment where investors aren’t getting much in return potential for taking on risk, we don’t see any asset classes offering compelling fat-pitch returns relative to their risk. Instead, our tactical positioning is more on the defensive, risk-management side. We know we sound like a broken record, but this remains a period in which patience and discipline are particularly critical, even if over the shorter term it may not seem so as markets continue to hit new highs. There is a powerful behavioral inclination to chase markets and asset classes that have already performed strongly. In contrast, our investment process and discipline is forward looking—based on longer-term analysis of fundamentals and valuations across multiple scenarios, informed by economic and financial market history and cycles, yet with a recognition that history does not exactly repeat. This investment discipline has served our clients well over our firm’s 27-year history, which is one history we do hope to repeat.

Thank you for your continued confidence and trust.

–Litman Gregory Research Team (7/1/14)

© Litman Gregory