Over the weekend I had the opportunity to take in baseball tryouts. I know you are thinking it is August so what tryouts would be taking place in the middle of the season? These tryouts were for U-8 boys. For the uninitiated, this is when boys aged 7 and younger try out for next season’s teams. My son spent two days at a baseball camp and then finished yesterday with team tryouts. During tryouts there were six stations covering the fundamentals of the game. While I have to say I was happy to see his energy during tryouts, his results were mixed so we’ll have to wait and see whether he makes the team. Either way, I give him kudos for his efforts and enthusiasm.

Last week’s markets were a little like baseball tryouts. We had a lot of information regarding the job market, the Fed’s views and the growth rate of the economy. In addition, I had a chance to hear from several money managers last week and I’ll share some of their thoughts as well. Let’s break it down and determine how it might impact where interest rates are headed.

Unemployment

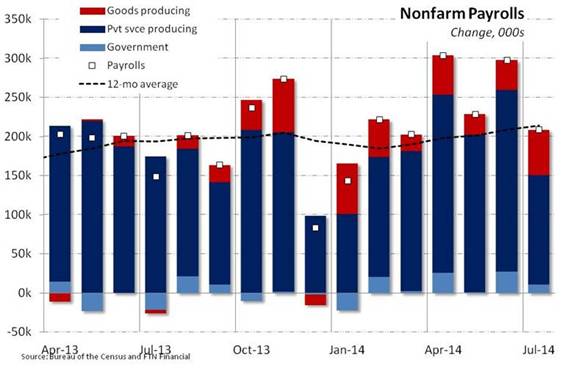

Nonfarm payrolls were up 209,000 jobs in July and the prior month was revised up 10,000 jobs to 298,000. As you can see from the chart below, the first 7 months of 2014 has produced more jobs than the last 7 months of 2013. The unemployment rate rose to 6.2%. The unemployment rate increased because more people are re-entering the workforce which can be taken as an indication that the labor market is improving in terms of the number of jobs available. Private Service sector jobs dwarfed construction and manufacturing gains up 140,000 versus 50,000 new jobs. The largest increase among private service sector jobs came from the combination of leisure and hospitality (+27,000) and education and healthcare (+17,000).

Nonfarm Payrolls

The increase in the number of jobs is great news, as is the fact that we have seen over 200,000 jobs created each of the last six months. The former Fed Chair Ben Bernanke said that he would have like to seen six months of +200k job growth at least three months before the end of the Fed’s bond purchases and so it seems that will be the case if they stay on the current path of reducing bond purchases.

The current Fed Chair, Janet Yellen, has expressed concerns about the quality of improvement in the labor market. While she is happy that the number of jobs being created is improving, she notes that the average increase in wages and hours worked, as well as the low labor participation rate, indicate that not everyone is fully employed. As a result, she has indicated, along with her fellow Committee members, that the rate at which interest rates are raised will likely be slower unless participation rates improve. The Fed has to focus on two things: price stability (i.e. the rate of price inflation) and achieving “full employment.” They currently aren’t too concerned about inflation because despite the occasional volatility in food and energy prices, inflation by their measure remains below their target. The Personal Consumption Expenditures index is up 1.6% year-over-year while the core index (ex-food and energy) is up only 1.5%. The Fed’s target is 2%.

Stock Drop

Last week’s stock drop could partially be attributed to the rise in the Employment Cost Index coinciding with Chair Yellen’s comments that rates will remain stable unless there is a pick-up in wage inflation. The index rose significantly, the most since 2008; however the year-over-year increase was only 1.8% so still in line with inflation. More likely the drop had to do with general indigestion from the geo-political issues roiling global markets.

Labor Participation

The labor participation rate continues to be at a multi-decade low level and it is this rate that has the Fed concerned about the quality of the labor market. While the number of jobs is increasing, the kinds of jobs available don’t necessarily fit the workforce skill set. This is an intractable problem that won’t be fixed in a short period of time and could be one reason for short-term interest rates to rise more slowly. You have college educated young people who can’t get “fully” employed and an older workforce who lacks the skills to find work in the technology driven labor market.

If you look at the unemployment rate among people with a college degree it is 3.1%. People under age 30 however have a higher rate of underemployment. There are a number of reasons for this and all of them are long-term trends. Boomers are working longer because they need to. The last five years weak labor market has made it difficult for recent graduates to find jobs that match their skill level, leaving them underemployed. Their high level of college debt forces them into jobs they might not otherwise take and so they have less time to look for a better paying job. This high level of debt presents another problem.

Housing

The Fed pays a lot of attention to the housing market because it is a primary driver of consumer oriented growth in the economy. The market is fueled at the front end by home formation, i.e. young people finding jobs, forming families and buying homes. As a result of employment trend above and cultural phenomenon, we don’t see this happening often enough. New home sales haven’t reached the 600,000 per year level since the beginning of the financial crisis. At the peak, sales were 1.4 million. If the Fed is going to maintain a reasonable growth rate in the housing market they need to keep the cost of debt as low as possible. Mortgage rates are keyed off of the longer end of the Treasury yield curve, 10-year bonds. It is possible that the Fed will try to talk the long end of the curve into remaining stable while raising the short-term Fed Funds rate, albeit slowly.

Last week, I had an opportunity to hear from one of our bond managers, Rick Rieder at BlackRock. He noted that credit scores among college educated young people with student loans have trended lower since 2008 while those people of the same age without a college degree have moved higher. The average score for someone with student loans is now under 635 while for those without it is 657. At the same time the percentage of people age 27 to 30 with mortgage debt has declined from near 34% pre-crisis to 22% post crisis. I am not suggesting that the best thing for young people to do is saddle themselves with mortgage debt, rather that these trends suggest that the housing market is going to be weaker and the Fed needs to figure out how to keep costs low for some time.

I also met with a developer of apartments last week. His target markets are urban and suburban-urban areas where young people and empty-nesters are congregating. He told me that his markets have very strong demand right now. He noted some of the same trends I mentioned above. He also indicated that the demand for rental housing is greater than 1.3 million units per year while the supply is less than 300,000. It might be a coincidence but these figures suggest that the housing formation for young people and empty-nesters is going to be rental, multi-family housing rather than the traditional home.

Economic Growth

Also last week, we received the first look at the second quarter’s economic growth (GDP), which was up 4%. This is a significant reversal from the -2.1% growth rate in the first quarter. However, before we get too excited about being off to the races, we note that final sales rose only 2.3%. This number does a good job of eliminating some of the inventory adjustments that take place from quarter to quarter. It also looks more consistent with the idea that the economy will continue to chug along at 2 to 3%, again providing some comfort regarding the notion that interest rates won’t rise to quickly. Consumption showed a 2.5% increase in the report up from 1.2% during the first quarter. Net exports detracted 2.2% from the growth rate due to the higher cost of oil. Overall the report was solid but certainly not an indication of a new growth paradigm.

With all of this news: employment improving, the Fed’s unemployment number being achieved, housing weak and growth recovering, where does that leave interest rates? Let’s look at the 10-year Treasury’s closing yield last week. We began the week with the yield near 2.50%. When the Employment Cost Index was released it rose to over 2.6%. On Friday, the yield fell to 2.5%. So despite the mixed bag of economic information, Fed speak and labor information, yields remained almost unchanged. Even the shorter term 2-year Treasury rose and fell by about 15 basis points (100ths of 1%). It is likely that this mixed bag of information will prevent rates from rising significantly for longer than most investors are currently thinking.

Brian K. Andrew

Mr. Andrew is President and Chief Investment Officer at Cleary Gull, Inc., an investment advisory firm in Milwaukee. He leads the firm’s investment research and strategy and chairs the Investment Policy Committee. Mr. Andrew received his B.S. in business and finance from the University of Minnesota and completed the Harvard Business School/CFA Institute Investment Management Program.