I have to admit that I usually avoid shopping. Typical male behavior, I suppose, but even male shoppers stop and consider signs like “Two for the Price of One!” when they eventually choose to grace the shopping aisles.

It just seems like an irresistible bargain, doesn’t it? But truth be told, it isn’t always, especially if you don’t really need one of the items, let alone two. Still, when you are shopping for something you do need and spot such a sign, it’s usually a good deal to take advantage of it.

In the last few days we have been treated to a pair of such sales in the stock market. Last week, the online shopping/auction site, eBay, announced that it was going to split into two companies consisting of its sales and PayPal payment system, with its stockholders ending up with shares of both companies. This morning Hewlett Packard followed suit and said it would be spitting its systems and computer/printer businesses into two companies with the same result for shareholders.

Why would two of America’s great success stories and most recognizable brands decide to split in two?

Those of us who can remember back to the 1960s can venture an educated guess. In the early part of that decade, the hot investment trend was conglomerates. Ling-Temco-Vought, ITT Corporation, Litton Industries, Textron, Teledyne, and Gulf and Western Industries were among the most notable conglomerates of the time.

The conglomerate was a company that owned many other companies. It was more than just a holding company, however. The companies owned were a diverse collection of companies deliberately selected to represent different sectors so as to allow the parent company to perform well in most economic scenarios.

By the end of the ‘60s, most of these companies had abandoned the conglomerate approach. Why? Primarily, because they found that it was too difficult to manage these diverse companies and maximize the potential of each while having centralized management of the parent company.

Each company eventually decided to reemphasize core competencies and spun off many of the different companies accumulated just a few years before. In the same way, both eBay and HP believe that their two constituent businesses can better provide their core services and address the very different competition the two divisions of each face with separate management of each of their currently combined divisions.

In portfolio management, we often face the same dilemma as the conglomerates of the ‘60s and the expanding brand names of today. We want to give our investments the best chance of growth in diverse circumstances while still managing our individual holdings in the best possible way.

Back in the early ’60s, portfolio management was much like those conglomerates. Modern Portfolio Theory (MPT) was in vogue and financial professionals carefully constructed portfolios of diverse asset classes to achieve diversification. They thought this would increase the odds that their clients would thrive in diverse markets and stay invested through the “thick and thin” of the financial markets.

Of course, today it is obvious that this accomplished neither. Those portfolios that were diversified by asset class and managed only passively, while besting an undiversified stock market index, still suffered market losses that were frightening to investor clients who thought they were protected.

In addition, we learned from all of the declines that punctuated the severe bear markets in each of the decades since the ’60s that once investors suffer substantial losses, whether in an individual stock, index, or diversified portfolio, they are very leery of returning to the stock market.

Today, we are merely seeing a repeat of investor behavior that we have seen play out so many times in the past. Since the stock market bottomed in March, 2009, the various stock market indexes have risen at least 100%, but many investors, now over five years later, still either have no or little investment in stocks in their portfolios.

Brian O’Connor, one of my favorite financial columnists, addresses this problem in an article today. He points out a Bankrate.com survey that recently found that 73% of Americans are still not inclined to invest in stocks even after these substantial market gains.

History tells us that this is a mistake. Yet it’s hard to overcome a deeply ingrained financial behavioral bias among investors. All of the studies tell us that investors are about twice as motivated by losses as they are by gains.

There have been many new developments since the ‘60s when MPT was created and in the decades since when it has continued to reign supreme among “politically correct” financial advisors. As we have discussed many times, portfolios of managed strategies (like our FUSION program) are designed to capture the best of both worlds, creating diversified portfolios of individually managed active strategies, instead of just asset classes.

Last week we released a white paper on another new methodology, bucket investing, and presented a webinar of the results of the research presented therein (financial professionals can receive a copy of the white paper and the webinar here).

Bucket investing abandons the single diversified portfolio approach and replaces it with multiple goal-based portfolios for each investor. Because we tend to “mentally account” for dissimilar investments differently (think about how differently you value and consider the possible uses for money in your pocket, wallet, savings account, or IRA), we tend to have different standards for judging their performance.

For example, in a two-bucket approach (you can create as many bucket portfolios as you want), you might have one income “bucket” and one growth “bucket.” The former would be invested to provide a retiree, for example, with current income. It would be evaluated for its ability to meet those needs and its performance judged over a relatively short time period based on how good it was at protecting the principal needed to generate that required income. At the same time, the growth “bucket” could be invested in stocks with a view to growing at a rate faster than inflation. Since growth needs time to be evaluated, that bucket would tend to be given greater leeway, since current income would not be affected by its performance and its role is to seek growth over the long term.

Financial behaviorists, and anecdotal evidence from professional advisors, tell us that this bucket approach does accomplish what it was fashioned to do. Investors do think of the various buckets differently and give more leeway in terms of performance expectations to the longer-term buckets.

As a result, investors tend to stay with their financial plan longer through market ups and downs, which normally is in their best interest. Also, since the focus is on the necessary portfolio to meet the initial income needs of the investors, they are more likely to invest in the program in the first place because of their exposure to an immediate decline in stocks is lessened.

Like any other investment technique, bucket investing has some weaknesses, but I’ll address them, as well the issue of when “Two for the Price of One” may not be advantageous, at the end of this article, along with a significant new discovery reported in our white paper. But first, let’s talk about what’s happening in the financial markets.

As I reported last week (even before the month was done), September was not a good month for any asset class. Stocks (foreign and domestic, large and small), bonds, and commodities all lost money in September. Furthermore, most also lost money in the third quarter as a whole, with a few notable exceptions where small gains were earned (the S&P 500 eked out a 0.66% gain in the three months, for example).

Although both stocks and commodities continued their decline last week, interest rates fell and bonds rose. This is a positive turn for at least one mainstay of higher stock prices, but with a Fed rate hike looming over the economy, it’s hard to rate it too positively.

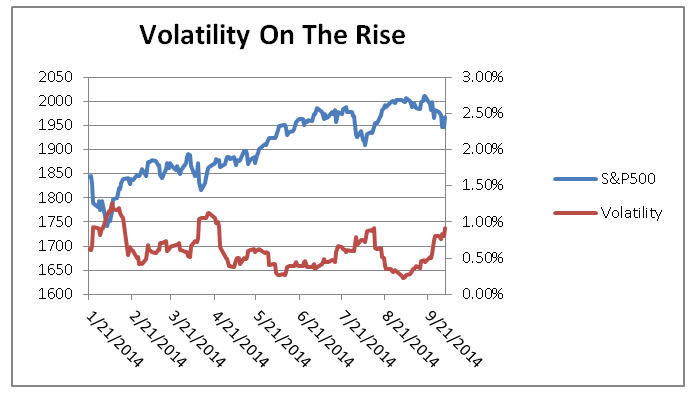

A real problem appears to be the reemergence of volatility in stocks. When we first developed our Targeted Volatility Analysis (TVA) position sizing, we measured volatility based on a ten-day average of daily volatility (standard deviation). As the chart demonstrates, when this measure is relatively high, stocks can flatten out or decline. There is no doubt that this measure is signaling a return of volatility after a period of very low volatility.

Source: Flexible Plan Research

While an improved employment report last Friday sparked a 200-point rally in the Dow Jones Industrial Average, economic reports generally continue to disappoint. We rated fourteen as below expectations last week, while thirteen were better than anticipated. It is encouraging, though, that when one takes out the three inflation-based indicators, the count was instead sixteen to eleven in favor of better-than-projected reports.

Source: Bespoke Investment Group

Earnings may provide the catalyst for a market rebound. The positive quarterly reports over the last few years have certainly done so. But these reports don’t start in earnest for a few weeks. And, of course, Wall Street continues to fret about whether the weakness in European and Emerging Market economies may cause our multinational companies’ earnings to lag.

Some have asked why, since I have been right in forecasting that September and October would be weak for stocks, did I not just exit the stock market. While some of our strategies have retreated to money markets, my opinion has been that at this time of the year the stock market can often reverse itself and move up very quickly. Therefore, I have simply advised investors who are underinvested in equities to increase their allocations to stocks as the market declines.

As we have been pointing out, seasonality is weak in this part of October and not usually supportive of a rally until nearer the end of month. But it is important to note that, as Bespoke Investment Group reported:

Going all the way back to 1928, more than a quarter (7) of the S&P 500’s 26 bull markets have either started or ended in the month of October! Additionally, of the 93 rallies of 10% or more without a 10% decline, nearly a third of them (30) either started or ended in October.

Furthermore, the probability of gains in stocks is highest in the fourth quarter. This is the case generally, and the odds are higher still when stocks are higher for the year, it is a mid-term election year, power is divided in Washington among the Republicans and Democrats, or we have a lame duck (can’t seek reelection) President. At the present time, all of these are favorably positioned.

Bucket investing can help you get back into stocks in a market like this one. But be aware there is a weakness to the approach. Believe me, after attending losses by the favored Tigers and Lions this weekend, I know that there is no sure thing.

Bucket investing does not always employ the optimal allocation of one’s portfolio. It often is too safe, i.e. it contains more than the optimal share of cash and short-term asset classes than it should to efficiently respond to the needs of all ages. As a result, in long-term studies it can underperform traditional portfolios and have a wider variation of returns for different investors (some substantially better than traditional portfolios and some less). “Two for the price of one” turns out to not always be the best.

However, in addition to being better suited to investor psychology in dealing with losses, and being a more appealing way to get back into the stock market, our white paper, reveals that the possible bucket investing deficiencies can be corrected with one simple addition. Our study demonstrates that by managing the various buckets with active management techniques, bucket investing can overcome the deficiencies, and outperform, yielding “Two for the price of one!”

All the best,

Jerry