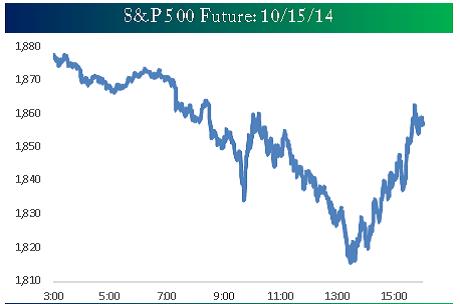

Quite a week we just had, regardless of asset class. By Wednesday the Dow had fallen 688 points by mid-day, thanks to a 480-point morning decline. The problem was a lack of liquidity—a buyer’s strike (no buyers in the market)—as we used to call it. In response, stocks fell, as did commodities (with the exception of gold) and yields plunged on bonds.

Then one of the Federal Reserve Board members said early Wednesday afternoon that with the weakness in Europe, maybe the Fed would put off raising rates. And the markets reversed on a dime and continued higher until the closing bell on FRIDAY. The stock market, while still down for the week by Friday’s close (except for the oft-maligned small caps, which closed higher) soared, with the Dow up over 300 points from Wednesday’s low point to its close that day and posted another 270-point gain on Friday.

But Wednesday is the day I want to focus on in today’s commentary. It was like Halloween had come early, the goblins were out, and the children were scared.

Source: Bespoke Investments Group

Listen to the talking heads on CNBC and a few rep phone calls that day and you would have thought it was October 1987 all over again. But that was a 25% single-day decline. Here, we were talking about the stock averages adding a couple percent decline to a correction that since the market’s all-time high on September 18th was then down about 9.5% (inter-day high to inter-day low) on the S&P 500.

Although the S&P is now down only a bit over 6% since that high, and we have had three up days in a row, we still need to talk about last Wednesday and some “investor’s” reactions to it.

Wednesday, and in fact the stock market’s decline since mid-September, should not have been a surprise to anyone. Readers of this column know that we started the year by saying that the odds were that we would be having a 10% or greater correction this year. Our Political Seasonality Index published in January suggested that historically the best chance of that correction was in the September-October period. We pointed out weeks ago that October was the most volatile of months for stocks, and we’ve seen a big increase in both downside and upside volatility already this month.

As encouraging as the rebound has been since Wednesday, the historical tendencies suggest we could have another down wave before we leave October for good this year. Are we going to have more panic if we do?

I hope not. Because if “panic” means investors are going to abandon their position in stocks or exit long held strategies, then each investor has to ask himself or herself whether they are indeed an investor or are they a trader or, worse yet, have they decided that they can time the stock market all by themselves.

Regardless of what type of investor you are, investing is not consistent with panic. Whether you are a passive or an active investor, the tenets of both disciplines caution against selling when emotion is high and panic is present. Most superb investors invest when there is panic in the streets.

Now, you know I am no fan of passive investing—whether you call it asset allocation, diversification, or Modern Portfolio Theory. It always fails us when a truly bad correction or financial crisis descends upon us—think 2000 and 2007.

I’ve been managing money exclusively based on active investing principles since before I started Flexible Plan in 1981. Active investing and managers practicing active investing utilize technologies designed to recognize the shallow retracements from the “big one.” There’s no guarantee that they will always be right, but that is their goal.

One rule we’ve all learned the hard way is that the stock market can rally much longer than most of us think. Furthermore, we’ve learned that it is easy to get faked out by the market if you are looking for an exit.

Think about the last twelve months. We’ve had five instances when the S&P 500 quickly moved down 3 to 4% (that’s only 2% less than the current decline) and many investors insisted that they had to exit. They did not heed the advice to “buy the dips” (even if it would have been the first buy they were making since the 2007-2008 bear). Yet the S&P just rebounded and kept moving higher.

Now after a year of those shallow dips it is no surprise that many of us were calling for a 10%-or-greater decline. But so far there is little evidence that the “end is near.” In every one of those past less-than-5% declines, there was overseas news that was troubling, or rate hikes were on the horizon and there was an economic indicator or two that seemed to throw us off the track. Yet the S&P just rebounded and kept moving higher.

Is this time that different? Well, I submit, not yet. But if you are an active investor, you don’t care what I think. You are watching your indicators. If you have them and they tell you it is time to sell, then by all means sell.

However, if you have decided you cannot time the market, you don’t want to ride stocks all of the way down when the big one comes, and you’ve chosen to utilize an active investment manager that practices dynamic, risk-managed investing, don’t panic. You found an active manager and chose active strategies that have had a good track record of dealing with past negative market environments … and there have been a lot of them—especially in my 35 years of doing this.

Why would you give up on the strategy or the manager at the first 5%-plus decline in almost two years? Worse still, why would you choose to do so when you are caught up in fear—of the economy, higher rates, European recession or, yes, Ebola—when you know from past practices and deep in your heart of hearts that panic is not a good sell signal?

At the same time, as an active manager I know that just because many long-standing indicators are positive, it’s not a time to just sit and be a passive bull. Instead, after years of being exclusively an all-in or all-out market timer, I’ve learned that a better policy for most markets most of the time is to rotate or re-position as the market goes through its many stages before the big one appears likely.

Almost all of our strategies that are still invested have gone through that rotation since early September. In some cases it meant buying more cash and bonds, in others it meant selling out of leveraged positions, and in others it has meant switching to more defensive equities and alternatives. Heck, in FUSION it has meant taking all of these actions.

We do this because the numbers—the quantitative analysis—that are spit out of our computers throughout the day still are showing, for the most part ,that there could be further substantial gains on the horizon. And we can live with that, despite the talk of the economy, higher rates, European recession and, yes, Ebola, because we know those systems don’t stop analyzing once the trades are done each week. Many strategies are daily, but even those that aren’t have been designed to constantly take in new data, unemotionally analyze it, and change direction if the data, rather than a wave of panic, demands it.

Earlier I mentioned that there could easily be more selling before we move into the November/December rally mode. Our Political Seasonality Index suggests as much (bottoming on October 27), and when we look at the economic reports coming out that have not lived up to expectations of late (do you believe it, eight out of eight below the predictions on, not coincidentally, Wednesday?). And who knows what the November elections will bring?

At the same time, lower interest rates and gas prices are good for consumers. And the highest Consumer Confidence rating since the financial crisis ended (which was registered on Friday) tends to be good for future retail sales and home builders.

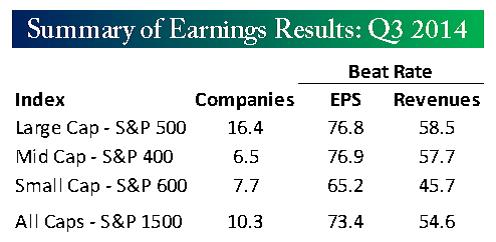

Much of the price action in the short term is going to be determined by earnings reports. We are starting into the heaviest two-week period for the third-quarter earnings and revenue statements. Twenty percent of the S&P 500 companies will report this week alone.

In this period of negativity, I would not be surprised to see the financial press focus on the few stocks coming in under analyst expectations—Netflix and IBM, for example. But as the chart below discloses, so far the reports have been on the whole very encouraging, with a very high rate of surprises to the upside not the downside. (Check out Apple tonight, for example.)

Source: Bespoke Investments Group

If the earnings surprises continue to the upside, the next surprise could be a resumption of the rally that to date has propelled the S&P 500 about 80% higher (5,700 Dow points) since its October, 2011 low—that was the last time we had panic in the markets and learned the truth of who among us was truly an investor.

All the best,

Jerry