I often listen to country music while reviewing research on Sundays. I like old country music, the kind that tells a story. Yesterday, an old George Jones song called the The Race is On, written by Don Rollins and recorded by George came on. The hook in that song goes: “Well the race is on and here comes Pride up the backstretch, Heartaches going to the inside…” Two races seem to be an area of focus for investors and markets.

Election Week

The first is tomorrow’s national mid-term elections. These include many Congressional seats, Governor’s and local political races. The big story has been regarding the distinct possibility that the Republicans will have a shot at taking back the Senate. Some pundits have gone so far as to say that this is the reason for the rally in stocks last week. I believe that the Bank of Japan’s (BofJ) action and the strong GDP growth report had more to do with it (more on that in a few paragraphs).

While some may wish for a Democratically controlled Congress because we have a Democrat in the White House, the reality is that some dysfunction between Congress and the Administration is welcome by markets. Near-term, many believe that the regulatory environment created by a Democratic Senate and Administration creates uncertainty and restricts corporate growth. While that may be true, it is hard to argue with the stock market returns over the last several years.

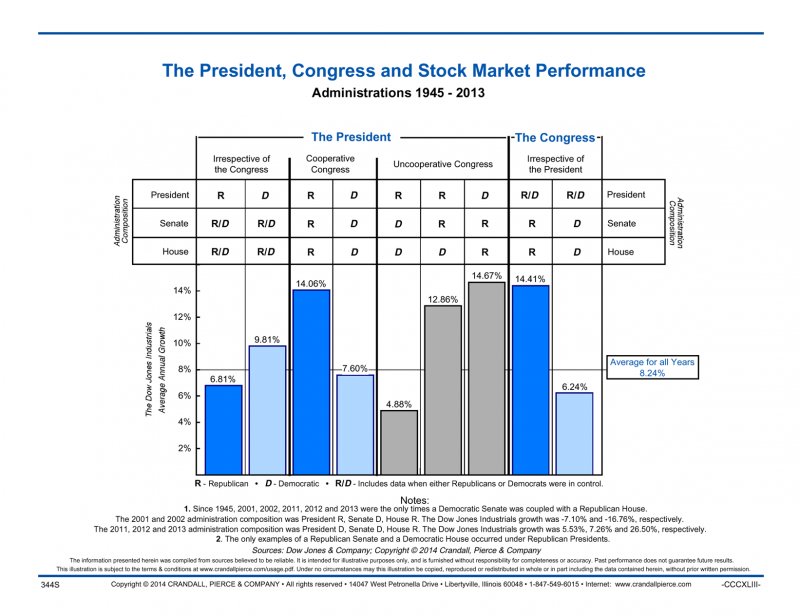

The reality is that markets appreciate some dysfunction in Washington. The chart below looks at stock market returns from 1945 to 2013. Returns are broken down based on which party occupies the White House and Congress. As you can see the highest level of returns comes when the Administration is controlled by Democrats and the Congress by Republicans. The average return during those periods is 14.67%.

Elections

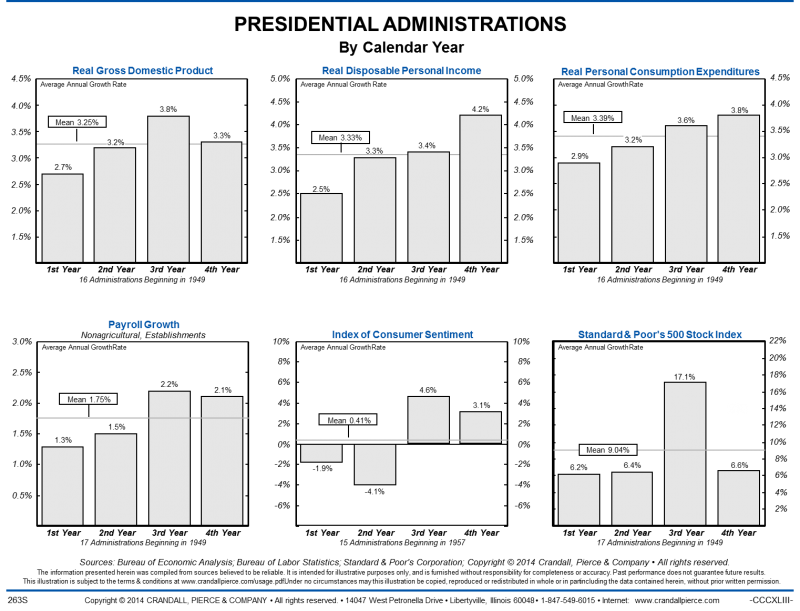

If Republicans take the Senate and you combine that with the data provided in this chart below you get a pretty good picture for 2015. These graphs reflect the strength of the economy, growth in disposable income, consumption and stock prices from 1949 forward. You can see that the 3rd year of a presidency seems to be the either best or second best. Most importantly, the third year is the best for stock price appreciation.

Presidential Administrations

Of course, we’ll have to wait for tomorrow’s results to find out just what kind of policy period we’re faced with.

Central Bankers

The other race that has been underway for six years is the one in which the central banks of the U.S., Europe, and Asia attempt to create the most stimulus for their lackluster economies. In this banker race, the U.S. seems to have decided to take it easy on the backstretch as the Federal Reserve ended their quantitative easing (QE) policy last week. Remember that the Fed has used two weapons to try and stimulate economic growth. They have been buying bonds each month and maintaining very low short-term interest rates. Last week they announced the end of their bond buying program which at one time was acquiring $85 billion of securities a month. The end was well telegraphed by the Fed and as a result we didn’t see much movement in interest rates. The 10-year Treasury yield started the week at 2.27% and finished at 2.35%.

Some might argue that the Fed’s program didn’t accomplish much, but that depends upon your perspective. Stock prices have appreciated over 38% during the latest QE period. Unemployment declined from 8.1% to 5.9%. Even by the Fed’s standards, the quality of the improvement isn’t as good as the headline number implies. The U.S. dollar has appreciated in value by about 7%. However, economic growth has barely budged and the rate of inflation has remained stable, but below the Fed’s target rate.

Nonetheless, the Fed, with “Pride,” has eliminated their bond purchase program and left the door open to begin raising rates next year. At the same time, perhaps as Heartache did in the song, the BofJ announced a new QE program that included raising asset purchases by $720 billion and using the government pension fund to acquire the stocks of certain companies. This looks like a move to the inside as they try to get the upper hand on an intractable problem.

They can’t get the economy growing fast enough to create any measure of inflation. The opposite of inflation, deflation is the enemy of any central banker. When prices are declining, businesses and consumers put off purchases with the assumption that goods will be cheaper in the future. This creates a lack of demand and slows the economy which pushes prices down. A deflationary spiral is very difficult to pull out of.

Europe is dealing with a similar problem, however not as bad. Economic growth has been weakening this year and as a result inflation has been declining. The unemployment rate across Europe is over 11% and core inflation was reported last week at 0.7%, also well below the European Central Bank’s (ECB) target level. The difference between the ECB and the BoJ is that the ECB has had a much more difficult time getting all the countries involved to agree on the same course of action.

For now, the U.S. appears to be winning the race as our economic growth rate is in better shape than our other developed country counterparts. Last week, real gross domestic product was reportedly up by 3.5% versus the expected 3%. Much of this growth seemed to be defense related as spending was up by 16% over the prior period and government spending was up by 4.5%. Consumption grew by only 1.8%, down from the 2.5% rate in the second quarter. Still, we believe that we’ll see better numbers ahead as the decline in gas prices makes its’ way into consumers’ pockets.

Given the herculean efforts of central bankers to stimulate demand and the meagre outcome for their efforts, you could argue that the song’s right – “the winner loses all.”