2015 Global Market Outlook: Exploring the Growth Landscape

For much of 2014, the financial press was filled with dire headlines warning of global stagnation and deflation. These demoralizing reports seemed to paralyze policy makers. The facts behind the headlines, however, suggested the reality was not nearly as gloomy or pessimistic as it seemed. This paper outlines a more optimistic outlook for 2015 where the world economy is expected to remain resilient and where the outlook for sustainable corporate returns remains strong.

2014 Market Review

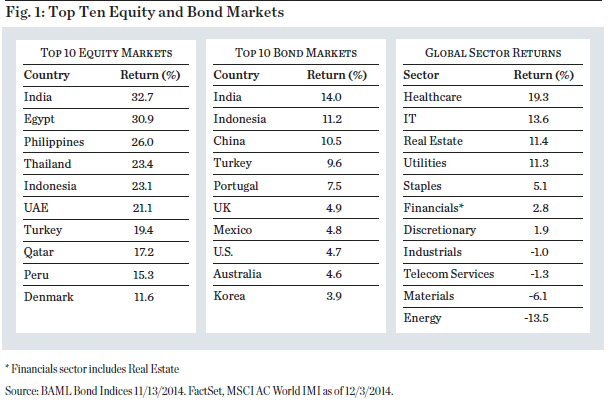

Emerging market economies dominated financial markets in 2014. Figure 1 shows a list of the top ten equity and bond market returns through early December, heavily populated by emerging markets. This was particularly noteworthy in light of the U.S. Federal Reserve’s unwinding of quantitative easing operations. Returns are shown in U.S. dollar terms, thus fully reflecting the negative impact of USD strength. We believe the strong performance of emerging markets in spite of Fed policy headwinds is a testament to how far these countries have come as well as their future potential.

In the bond markets, global yields continued to compress in 2014. As recently as two years ago it would have been highly unlikely for a sovereign to make the top ten returns list with a yield of less than the mid-teens. But in 2014, yields of just under 4% represented some of the best returns available in fixed income. It was not surprising to see the search for yield spill into the equity space. This was evidenced by the fact that three of the top four performing global equity sectors were healthcare, real estate, and utilities.

Healthcare’s stellar performance was perhaps not surprising given the amount of mergers and acquisitions, both fulfilled and unfulfilled, occurring in the sector globally. With companies like Shire, Actelion, and Coloplast each up 40% – 60% in 2014, the market was showing its preference for security, high free cash flow, and good dividend yields.

The emphasis on yield and stable performance was also evident in the real estate sector, which was strong in 2014 across much of Continental Europe, the United Kingdom, and Sweden. Finally, compressing bond yields had a similar positive effect on utilities broadly, with particular strength in the European periphery markets as companies like Red Electrica and EDP-Energias de Portugal performed well. We believe that this focus on yield and free cash flow will continue to be an important driver of returns as we look ahead to 2015 and beyond.

Current Landscape: Low Growth and Pronounced Disinflation

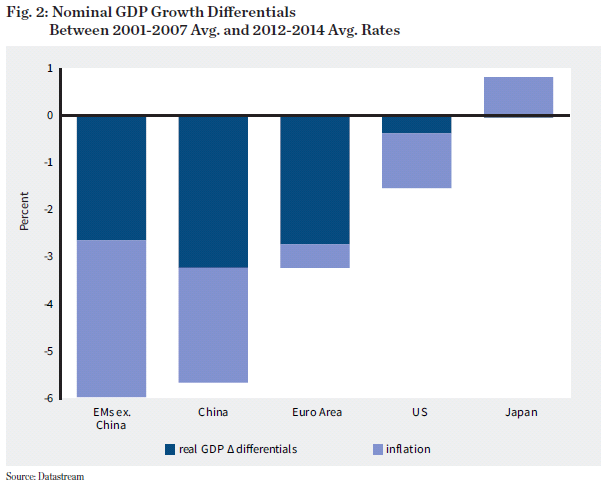

How do we reconcile the disconnect between alarming financial headlines and actual market performance? We assert that it is all about falling inflation or “disinflation,” Figure 2 highlights the differentials between average growth rates in the years prior to the 2008 financial crisis and the last three years.

The total height of the bar is the nominal Gross Domestic Product (GDP) growth differential, which is composed of real growth and inflation. This clearly shows that most of the deceleration in growth was driven by lower or falling inflation. The notable exception was the Euro Area, where real growth decelerated dramatically. This disinflation trend has been a global phenomenon. In fact, the only major economy that registered significant acceleration in inflation over the last three years was Japan.

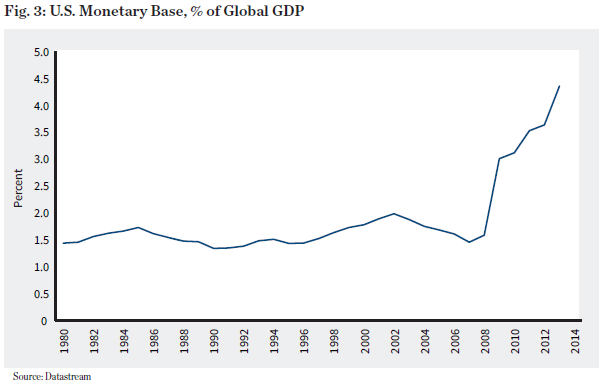

The pronounced and enduring disinflation across the globe is especially noteworthy in light of what has been a very aggressive monetary policy easing pursued by major central banks around the world. Figure 3 illustrates the growth of the U.S. monetary base as a percent of total global GDP. The amount of money supporting the U.S. economy has tripled in the last five years compared to the previous three decades.

The Fed has been joined in this effort by the Bank of England (BOE), and more recently by the Bank of Japan (BOJ), the People’s Bank of China (PBOC), and several smaller central banks. Despite this abundant liquidity injected into the world economy, the anticipated inflation has not ensued. Notably absent from this list is the European Central Bank (ECB), which remains embroiled in a heated debate with Germany, France and Italy on the issue of expanded powers and the fundamental role of the central bank. However, it is expected that Europe will be joining the BOE, BOJ, and PBOC in outright quantitative easing at some point in the spring of 2015.

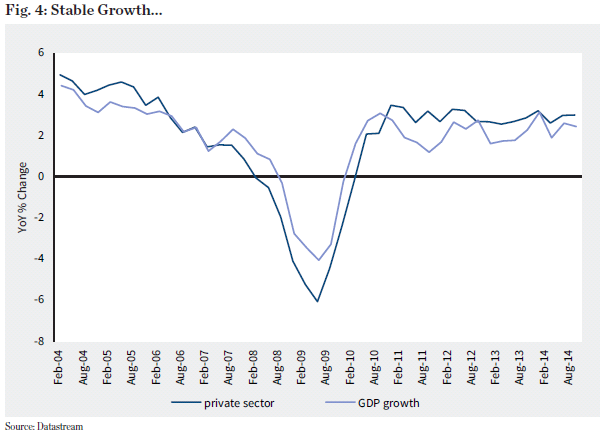

Private sector growth in the U.S. has been quite robust and resilient for the past five years. Figure 4 shows the U.S. private sector has expanded at a rate of 2.25% – 2.50% quarterly (year-over-year) for an extended period.

In addition, industrial production volumes surpassed the 2007 peaks earlier in 2014, and industrial capacity is slowly working back to its pre-crisis levels.

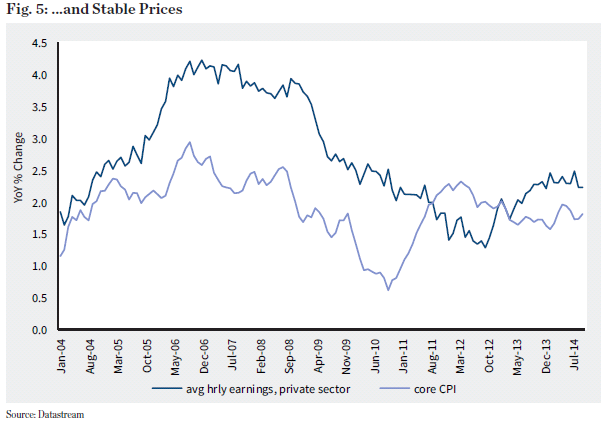

Figure 5 shows that core consumer price inflation (CPI), excluding energy and food, is not accelerating. Likewise, hourly wage growth is not accelerating to anywhere near the levels seen before the 2008 crisis. In fact, the employment report released in early December 2014 was strong, showing the U.S. economy is adding quality private sector jobs at an ever-increasing rate, yet there are no signs that wages are increasing.

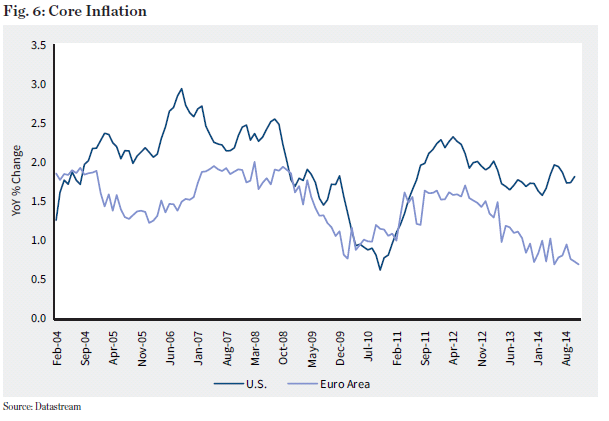

Figure 6 illustrates a similar disinflationary dynamic in the Euro area, especially when actual growth differences between the two sides of the Atlantic are taken into account. Core inflation has always been somewhat lower in Europe compared to the U.S., however, the more recent slowdown is largely due to weak growth. The headline inflation in the Euro Area is even weaker than the core, which has been the one beneficial effect of the rising tensions and sanctions on Russia. In the very short term, vast quantities of food exports destined for Russia were instead left in Europe, where a sizeable short-term oversupply meant lower food prices for many European consumers.

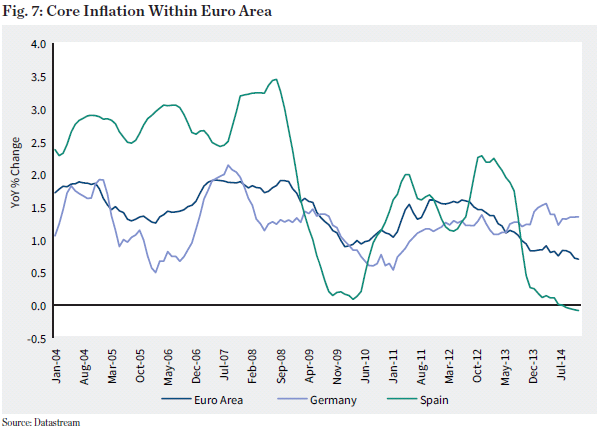

On a longer term note, change in the regional source of inflation within the Euro Area speaks to the ongoing significant structural adjustment taking place in Europe.

Figure 7 shows that, before 2008, core inflation in Spain was persistently at least one percentage point higher than the average for the Euro Area. At the same time, Germany was the “sick man of Europe” with correspondingly weak domestic consumption and inflation. Today, this dynamic is completely reversed, as Spain is regaining competitiveness while the German consumer is enjoying good wage growth.

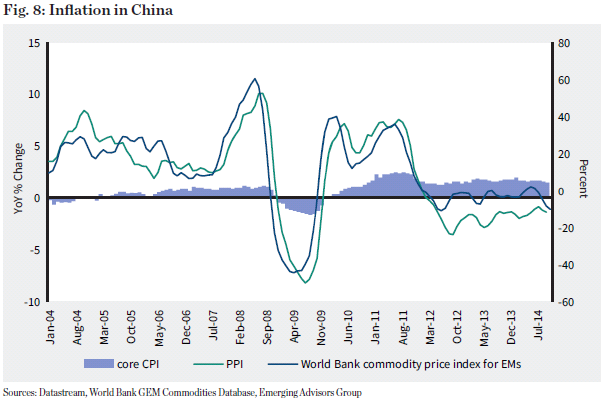

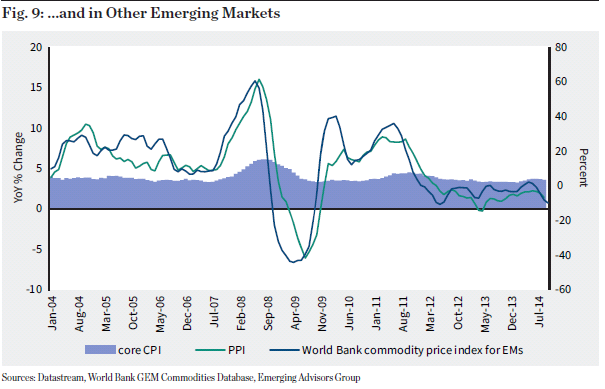

The same disinflation trend is also evident in emerging markets. Figure 8 illustrates how core prices in China are growing faster now compared to the pre-2008 years. This is welcomed evidence of the ongoing rebalancing of the economy toward private domestic consumption. Much of the disinflation is coming from commodities prices, as producer prices in China follow commodities prices quite closely. China is not unique in this respect.

Figure 9 shows the same dynamic playing out across emerging markets broadly.

Commodities and Resources

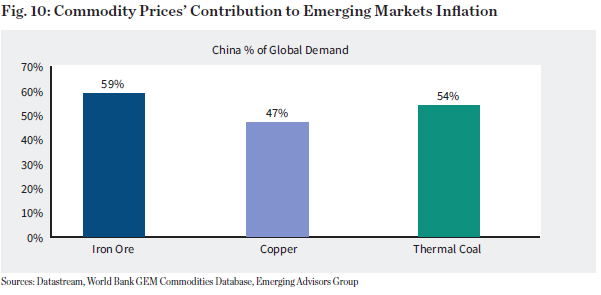

China’s massive infrastructure overinvestment is clearly a factor in the pressure on commodities prices. In metals and certain forms of energy, most notably coal, China accounts for a large proportion of global demand (Figure 10). At the same time, the ongoing slowdown in residential real estate construction is applying downward pressure on the associated industrial metals and minerals prices. However, metals and coal account for only about 15% – 20% of commodities consumed by the emerging markets. The two principal contributors to inflation, food and energy, account for over 80%, and China is only one of many players. Specifically, China accounts for only about 20% of global fuel consumption, which is roughly in line with its share of global GDP. In agricultural markets, China barely plays any role at all. This supports the thesis that global disinflation has been driven by broader forces than China’s supposed overinvestment.

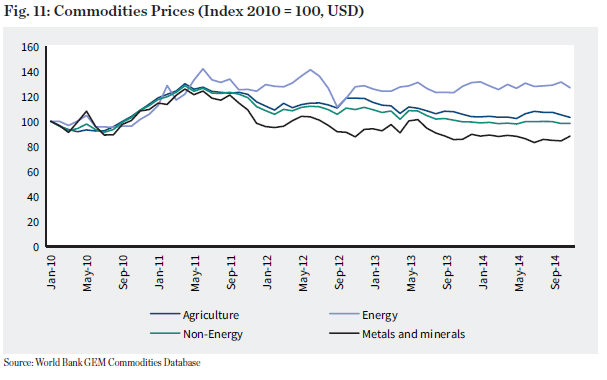

Over the past five years, commodities prices, as shown in Figure 11, have been broadly flat or declining slightly, showing no signs of inflation.

Oil prices fell sharply in the second half of 2014 due in part to the strong growth of shale production in the U.S. in recent years. At this point, the general expectation is that a dramatic reduction in oil prices will likely drive out some of the high cost producers in the U.S., with less additional supply resulting in higher oil prices by the end of 2015. While it is possible that this conventional argument will play out, we believe it is also equally possible that technological changes that are driving down the cost of fracking and shale production in the U.S. will continue to be underappreciated. Instead of leading to a significant decline in supply, current oil prices may only slow the growth of U.S. shale production. In this scenario, lower oil prices may not rebound as conventional wisdom suggests.

The drop in oil prices can be viewed as a tax cut on a global basis; some estimates are as high as $40 billion. This is clearly a positive for the consumer globally. On a country-by-country basis, the impact may be positive or negative depending on whether you are an importer or exporter of oil. From a Russian or Venezuelan perspective, this is almost a catastrophic development. On the positive side, countries that are dependent on imports are actually doing much better; for example India is a clear benefactor. For the U.S. and Europe, the pull-through from cheaper oil prices is a significant positive and clearly beneficial for the consumer.

Why Does Inflation Matter?

We believe that the prevailing environment of low inflation is particularly relevant to equity investors as it is a key source of corporate pricing power. The economy, as measured by GDP, effectively consists of wages and corporate profits. Both of these are partially driven by rising prices. Since the end of World War II, policy makers around the world have sought to ensure that the global economy operates in a low and stable inflationary environment. Company executives learned how to produce and sell products in such an environment, while financial markets participants designed tools to assess corporate performance in an inflationary setting. What are the implications for growth in a world without inflation? To the extent that inflation is seen as a manifestation of growth, is disinflation by extension a sign of stagnation?

Are growth and inflation really disappearing? We believe that the three key forces simultaneously driving growth and disinflation over the past four or five decades are globalization, technological innovation, and deregulation. Their importance over this time period is uncontested, and it is clear that they are not necessarily always forces for good – there are excesses and negatives associated with each. As we try to determine whether growth and inflation have permanently changed, we closely examine these themes.

From a globalization point of view, the expansion of trade and increased level of investment that have been seen post-World War II and post-Bretton Woods have led to integrated supply chains, cheaper products and even cheaper services on a global basis. Clearly economic growth has benefitted from globalization, but it has also been a significant contributor to disinflation as well.

Deregulation has enabled the opening of industries to private capital, the breaking down of monopolies, changes in workforce regulations, and the creation of wholly new industries. The resulting competition has driven growth, yet deregulation is not a panacea as the negatives associated with deregulation are also significant.

Technological innovation has unequivocally been a strong growth driver, but there is often capital misallocation associated with the hype of technology, as occurred most obviously amid the tech bubble period. The Moore’s Law curve, still very much intact today, has expanded processing power at ever cheaper rates and is leading to further disinflation while still producing growth. The conclusion drawn from these longer-term trends is that growth is intact but it is also important to understand the disinflation component.

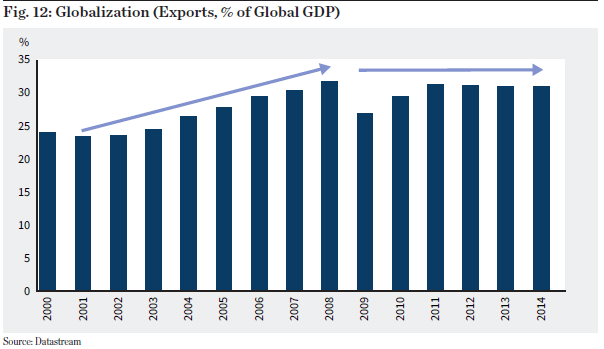

The question remains: have these growth and disinflationary forces exhausted themselves? In the aftermath of the 2008 crisis, at least two of the three, globalization and deregulation, appear to have stalled. In Figure 12, global trade volumes are shown as a proxy for globalization. Following a decade of strong gains where global trade grew well in excess of global GDP, trade growth has slowed to a rate approximating global GDP growth.

Lack of progress on deregulation, which falls under the auspices of general economic policies, was well summarized by the International Monetary Fund’s José Viñals at a recent gathering in London. He accurately noted that, for the past five years, of the three major policy pillars, monetary policy has been the only game in town. This is true across much of the world, as most national governments focused on making sure that their domestic economies could weather the storm of demand destruction post the 2008 crisis.

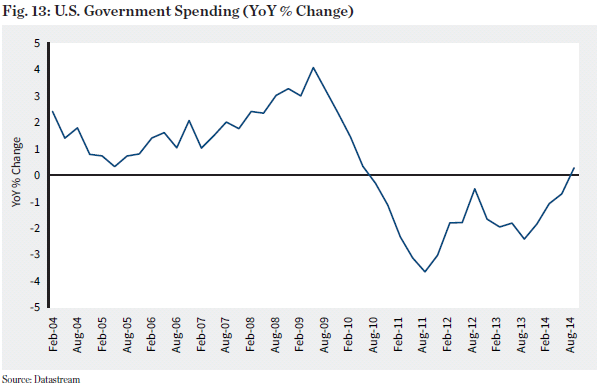

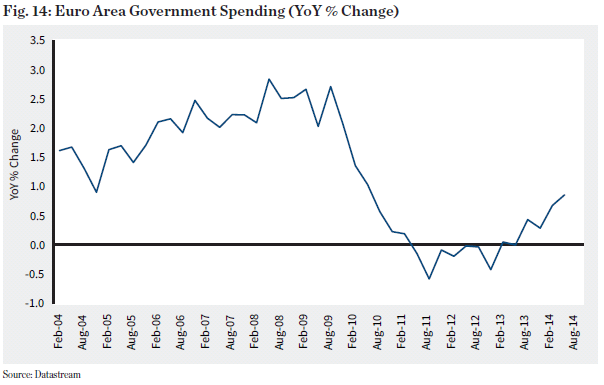

But, five years after the financial crisis, things seem to be changing. Fiscal consolidation is over in both the U.S. and the Euro Area. As shown in Figures 13 and 14, government spending on both sides of the Atlantic declined sharply through 2011 and is now beginning to contribute positively to growth.

Globalization Trends

There are signs of reviving globalization, despite the fact that the last round of Doha negotiations at the World Trade Organization failed at the last moment in 2014. There are several transformational regional agreements in the final stages of negotiation following many years of work. Specifically, the Trans-Pacific Partnership (TPP) spans three continents and includes the U.S., Japan, Australia, Canada, Mexico, Peru, Chile, New Zealand, Malaysia, Singapore and Vietnam. Together, these economies account for 40% of global GDP. Further significant dismantling of trade barriers in goods and services, as well as intellectual property, will have a measurable boost to trade.

Less frequently discussed, but no less important in terms of its economic impact, is the Transatlantic Trade & Investment Partnership (TTIP), which is a regional agreement between the U.S. and the European Union. Taken together, these economies account for 45% of global GDP. Most negotiations on this have been completed and the lawyers are putting the finishing touches on the final text. If ratified, the benefits are estimated in the hundreds of billions of euros or dollars over the next 15 years. This would not only benefit the two economies in question, but the world at large.

Last month, China signed a free trade agreement with Australia that has been in the works for nearly a decade. It is a major step toward fully liberalizing bilateral trade between these two countries.

Globalization efforts do appear to be reviving. No fewer than a dozen bilateral and regional trade deals are currently in various stages of negotiations. While change is slow, structural changes are cumulative and we believe that these agreements in aggregate can have a meaningful impact over time.

Structural Reforms

The outlook on deregulation, or structural reforms, is also improving with several developments that promote growth and are disinflationary. Significant reforms are being seen in India, where the current Prime Minister Narendra Modi was elected in 2014 on a strong reform mandate. Modi appears to be delivering on his promise of less government “There are signs of reviving globalization...” and more governance. In an effort to lessen bureaucracy and streamline the provision of services, Modi’s government is prioritizing the digitization of permits requests and the centralization of subsidies distribution. We believe these microeconomic reforms will reduce the costs of doing business, as they limit opportunities for corruption and more efficiently deliver funds to end consumers without “bleeding” to endless layers of bureaucracy. In this way, these reforms are highly disinflationary.

In China, the current leadership consolidated power faster than most outside observers thought possible, taking concrete steps toward breaking up the triumvirate of state owned enterprises (SOEs), local governments, and large state-owned banks. If implemented, these reforms could pave the way for continued growth in China for years to come.

Reforms are not limited to emerging market economies as advanced economies are also making strides, perhaps most notably Japan. The key structural change that is a significant focus of Prime Minister Shinzo Abe’s efforts is inflation. There are early signs of success and we are already seeing positive signs of corporate performance in response.

Even the Euro Area is undertaking major initiatives. This is not limited to the recently announced infrastructure spending initiative in Europe, which so far has included few details and garnered little enthusiasm from the private sector. Fifteen years after the introduction of the single currency, there will finally be a banking union. As of November 2014, there is now a single, pan-European banking regulator, hastening the development of a fully integrated financial services market. All of these reforms are growth-promoting and disinflationary to the extent that they take costs out of the production of goods and services.

Investing in Growth in a Non-Inflationary World

How does one invest in growth in this noninflationary world? Our approach remains the same. Our philosophy has always been focused on seeking high quality growth companies that can deliver strong corporate performance. We remain focused on companies that we believe have the ability to generate free cash flow from both the top line and operational leverage on the margin side, which can then be reinvested back in the business or returned to shareholders.

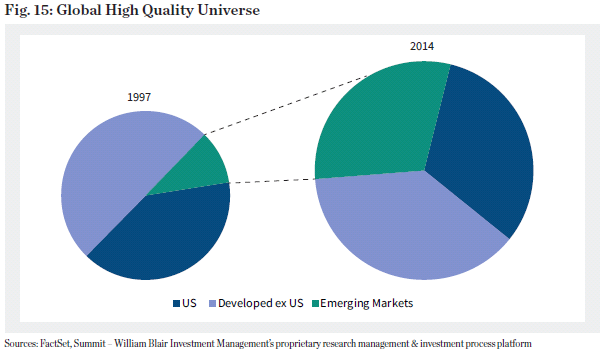

Our continued focus on quality growth brings us to emerging markets (EMs). During the decade preceding the financial crisis, most major EMs undertook significant macroeconomic restructuring. Inflation and fiscal spending were brought under control, current account deficits were eliminated or reduced, and external debts were repaid. This paved the way for sustained rapid growth and has resulted in significant changes to the composition of the global high quality universe.

In 1997, as shown in Figure 15, our investable universe of high quality companies included just over 1,300 names, only 10% of which were from EMs. Today, not only has the universe doubled in size, but the number of high quality companies in EMs has risen seven-fold, and is now on par with the number of high quality companies in the U.S.

This macro restructuring and non-inflationary growth led to a rapid rise of the middle and lower middle class where the propensity to consume is many times greater than in developed economies. It is also where large groups of people are demanding continued non-inflationary growth. This was at the heart of the 2014 protests in Brazil. Political ramifications of the rise of the middle class in EMs are evident from India and Indonesia to Mexico, and perhaps less obviously, Brazil. As a result of their restructuring, many EMs are in a stronger position to control their economic development. In our view, the vigor with which they are able to implement reforms will largely determine the continued evolution of their economies and their growth trajectory.

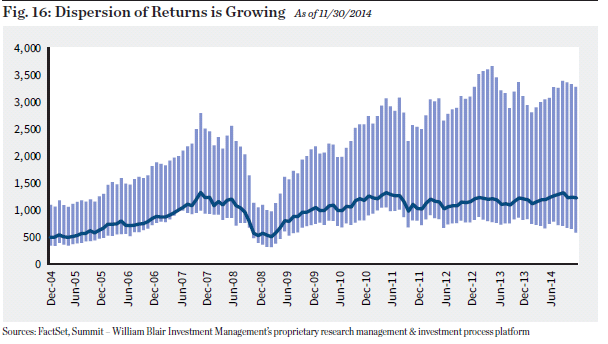

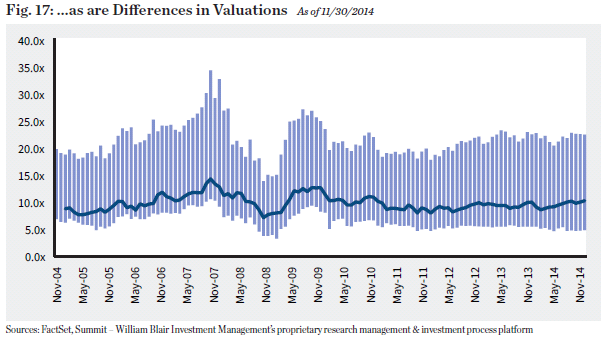

Now more than ever the EMs are a heterogeneous lot of countries with very different economic and growth trajectories. For example, the prospects for India are significantly different than those for Russia. We believe the market now understands this as Figures 16 and 17 display the trends in the dispersion of returns and valuations. Whereas 10 – 15 years ago most of the EMs were traded or valued as a single asset class, the dispersion of the returns has expanded and the market is much more aggressively trying to differentiate between really true, sustainable quality companies and those that are not. The market appears to be paying for this as the differences in valuation are also notable.

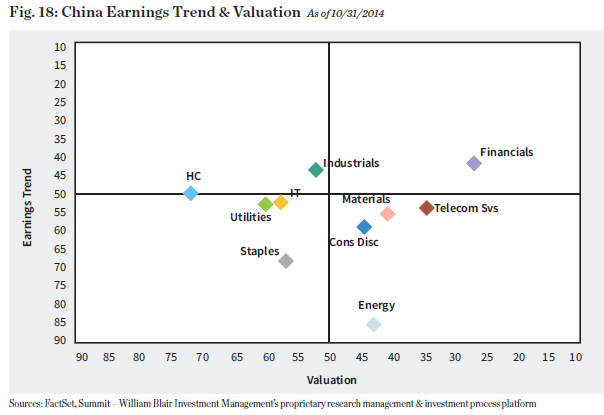

Substantial dispersion can also be seen in Figure 18 by looking at the earnings trend/ valuation lens used by William Blair to evaluate stocks, sectors and countries. This illustrates how China, a market that was much more homogenous itself 10 – 15 years ago, now exhibits substantial dispersion across sectors in terms of valuation and earnings trends.

India

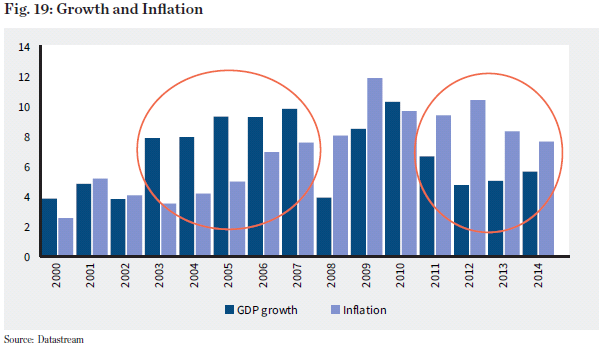

In the case of India, the goal of the near term reforms is to change the mix of economic growth and inflation. As shown in Figure 19, in the years preceding the financial crisis, India experienced strong growth and relatively low inflation. Over the past five years, the picture has completely reversed, with prices growing at or near a double-digit pace, while the economy grew at half the pace of the 2000s. Although inflation fell noticeably in the second half of 2014, Reserve Bank of India Governor Raghuram Rajan has yet to cut interest rates. Rajan’s actions suggest that the government is serious about reining in inflation to pave the way for productive investment and growth. For growth to accelerate, India needs massive private and public investment. Ultimately, the objective is to incentivize investments and to bring investment growth to generate further output gains.

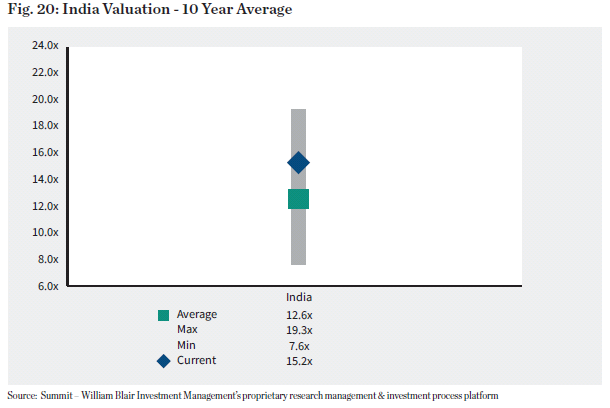

As previously cited, India was the best performing market in 2014, in terms of both bonds and equities. Figure 20 shows that equity valuations are clearly above their 10 year average, but this does not necessarily mean they are overextended. Quality companies, as demonstrated through recent (or historic) corporate performance, are quite abundant in

India. It is not surprising for the technology sector to be a source of high quality companies, with well-known leaders in IT services, but we also see strong corporate performance in pharmaceuticals and the automotive industry.

Although valuations have increased, we believe there is potentially more opportunity from an equity investment perspective, as India is outperforming its emerging markets brethren with respect to earnings. While the spread is not huge we believe it is significant in that there is strong underlying fundamental performance. We will continue to review the fundamental earnings trends and progress on reform measures.

China

Deciphering China’s reform efforts is considerably more challenging. In the initial decades, China’s remarkable growth was based on an intertwined relationship between SOEs, local governments and large, state-owned banks. Such a system was very successful in rapidly mobilizing financial resources and developing infrastructure. At the same time, the private sector developed largely outside of this triumvirate, with little access to capital or resources. The private sector flourished despite these obstacles.

Today, private companies in China account for nearly 90% of employment and the vast majority of corporate profits. It is widely acknowledged that services and consumption are best delivered by market-based mechanisms. Chinese leaders have long recognized this, and efforts to open private sectors to capital more formally while dismantling SOE dominance are well underway.

The reforms over the next several years are complex and interrelated, but fall generally into three categories:

• SOE Restructuring: Provinces have published plans to restructure their SOEs, including asset sales, to the private sector. Several large companies, such as China Telecom and CNOOC, have already published their plans for mixed ownership and consolidation, and many local SOEs have already announced privatization plans. There are nearly 100,000 local SOEs in China, so the amount of assets and companies opening to the market will be significant in the coming years.

“If China is successful in implementing these reforms, we believe they will be strongly growth generative and ultimately disinflationary.”

• Fiscal Reform: In order to restructure and dispose of SOEs, local governments must have sources of financing other than SOE profits and land sales. Effective January 1, 2015, provincial level governments will be allowed to issue debt on behalf of towns and counties, subject to the provincial ceiling. This is the beginning of the municipal bond market in China, which we believe will also pave the way for greater transparency, and ultimately debt sustainability, in local government debt. At the same time, local governments are now expressly forbidden from setting up local government financing vehicles (LGFVs). There are also plans to address the existing stockpile of local government debt.

• Financial Liberalization: These reforms are accompanied by financial liberalization, as insurance companies and other financial intermediaries move in to collect savings and provide services previously reserved for state-owned banks.

This is a highly complex reform process that will take several years to materialize. If China is successful in implementing these reforms, we believe they will be strongly growth generative and ultimately disinflationary.

Japan

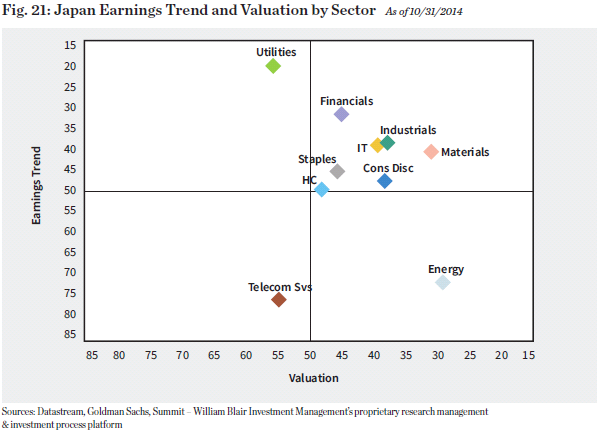

While various portions of the three arrows of Abenomics remain somewhat unfulfilled, the fundamental trends are encouraging. Using our earnings trend/valuation lens, the most interesting region globally remains Japan with strong earnings trends and supportive valuations across most sectors, as shown in Figure 21.

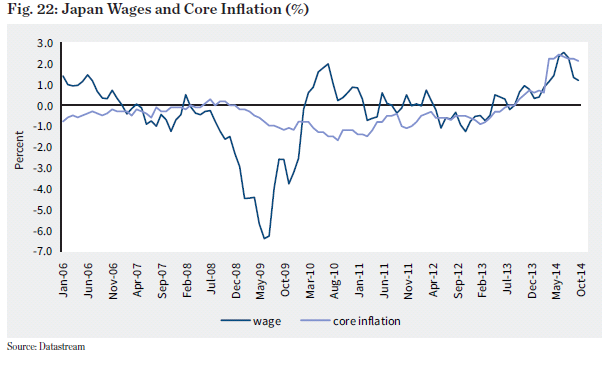

As seen in Figure 22, wages and core inflation are a key part of our positive view on Japan.

With regard to retail sales, efforts to move the buying public in Japan away from the caution previously exhibited were not helped by the sales tax increase in the spring of 2014. The result has been the postponement of the second tax increase, which could be positive for the economy more broadly.

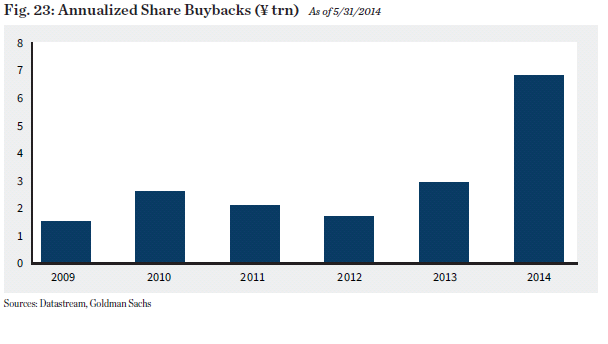

Annualized share buybacks (Figure 23) illustrate how corporate performance has shown significant improvement in the past six months. The virtuous circle in Japan, in which higher return on equity is sought by management and rewarded by the market, is a significant change in the mental approach toward investment in Japan. Improved corporate performance evidenced by higher earnings, better dividends, and share buybacks that have been significantly ahead of market expectations, has given us confidence that reforms are already producing results. We are particularly encouraged by the recently launched JPX-Nikkei 400 Index targeting high ROE companies with good governance standards, and the Government Pension Investment Fund’s doubling of its target equities allocation in an effort to improve prospective returns.

United States

Finally, the U.S. enjoyed good performance in 2013 and 2014 driven by multiple expansion. While earnings have been catching up, U.S. valuations are extended versus the rest of the world. We believe that is fair since corporate performance has been much better in the U.S. than it has been in many other places. We are quite cognizant of the fact that reform, especially on the banking side, happened earlier and much more efficiently in the U.S. than it did anywhere else – most notably Europe. This is evident in the returns profile and GDP growth which is significantly ahead of what we have seen in other markets, particularly Europe.

With respect to the earnings outlook, there has also been considerable discussion that U.S. corporate profit margins will come under pressure. To the extent that we are not seeing wage growth being a significant impediment to corporate profit margins, we believe U.S. corporates will likely sustain their profitability profiles.

Summary

We anticipate the world economy in 2015 will remain resilient, but with a moderate growth profile overall. IMF data project global GDP growth around 3.3% – 3.5%; satisfactory in an historical context. The U.S. and Europe are expected to benefit from dissipating fiscal drag, while the Japanese tax increase postponement should have a positive impact. Emerging markets should benefit from lower commodity prices, stable developed market demand and domestic reform efforts.

Disinflation is likely to continue as we expect globalization, structural reform efforts, and technological changes to lead to lower prices. The emerging markets will continue to be important to investors, but differentiation among countries, sectors and companies will be critical to success. In our view the emerging markets are not a homogenous group: the prospects for India are significantly different than those for Russia.

As always, we will continue to seek sustainable corporate returns. We strongly believe that companies that demonstrate high returns on investment are better positioned to navigate this environment, and have better potential to provide a solid foundation for our portfolios.

Important Disclosures

This material is provided for information purposes only and is not intended as investment advice nor is it a recommendation to buy or sell any particular security. Any discussion of particular topics is not meant to be comprehensive and may be subject to change. Data shown does not represent the performance or characteristics of any William Blair product or strategy. Any investment or strategy mentioned herein may not be suitable for every investor. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Past performance is not indicative of future results. Information and opinions expressed are those of the author and may not reflect the opinions of other investment teams within William Blair & Company, L.L.C.’s Investment Management division. Information is current as of the date appearing in this material only and subject to change without notice.