After spending over 32 years working in and around the financial services industry, I have come to a realization about one of the most important attributes for investors.

This lesson has been slow in coming and sometimes painful. Specifically, this attribute concerns the self-knowledge that: one really never understands everything that goes on in the markets, that the learning process is never fully complete, and that personal bias and opinion can often be detrimental to the health of one’s portfolio.

We see this play out in many ways just about every week:

-

Markets are unpredictable, often perplexing and confounding. As I write a weekly chart analysis for Proactive Advisor Magazine, a trend that comes to the fore seems often to reverse itself by the time we go to publication three days later. It is one reason sentiment readings are often viewed as contrarian signals—“the crowd” is frequently a step late and often wrong.

-

Markets are full of a combination of “known knowns,” “known unknowns,” and “unknown unknowns.” You do not have to look any further than the millions of dollars of paper losses by the airline industry on oil futures hedges over recent months to see how even the most expert of analyst communities can totally miss predicting a major move.

-

Markets will always cycle up and down, often for seemingly unfathomable reasons. The recent drama playing out regarding Greece’s financial state, the volatile situation in Ukraine, and any number of serious geopolitical issues in the Mideast have been largely minimized by the markets for the past three weeks, surprising many financial commentators. As one financial advisor I recently interviewed put it, “The market will have another serious correction, that is a certainty—I just do not know when or what will cause it.”

So what is the answer for dealing with all of this continual uncertainty?

Quantitatively-based, active investment management, which strives to take emotion and opinion out of the investing equation, would seem to be a logical answer. Models and algorithms that seek to allocate to asset classes and sectors according to what is happening in the markets, and not what “should” be happening, form the basis for the strategies offered by Flexible Plan Investments, Ltd. These models may not be on the right side of every short-term wiggle in the markets, but over the long haul, it is all about improving the probabilities for investors’ success and attempting to capture a reasonable portion of major trends, whether they be to the upside or downside.

Combining all of these themes into one, I recently read something that may not be totally new in terms of content, but I did not know it came with a formal name. An article in the February issue of “Technically Speaking” (published by the Market Technicians Association) examines “Rohrbach’s First Lesson of Investing.”

I had never before heard of James Rohrbach, but he is apparently a fairly well-recognized newsletter publisher focusing on market timing signals. Although it may never be immortalized in investing history books, his “lesson” says, “When you make an investment that is not going the way you thought it would, sell it and take the loss.” I am not sure I agree 100% with this message, and think it is all about time frames and the bigger picture, but I do agree with the spirit of the thought. And it would be hard to disagree with the behavioral finance explanation behind his particular system for active management:

“Taking a loss at the right time may be the best decision anyone can make. Market timers smile more and outperform the buy-and-hold crowd because the market does take big drops now and then. They (timers) sleep well, and you can’t put a price tag on that. There are only two good feelings in investing: one is being in the market when it is going up, and the other is being out of the market when it is going down."

If only it were that easy!

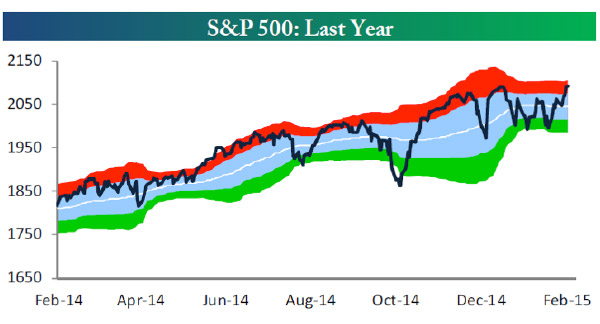

The new record-setting levels for the S&P 500 attained last week are a case in point on the inherent puzzling nature of the markets. Jerry Wagner, president of FPI, has said for some time that the equity bull market is intact until key technical levels are consistently violated for a significant period of time—but it has been a somewhat uncomfortable and volatile ride for several months now.

Last week saw the market shrug off those international factors cited above, and some lackluster US economic data, instead focusing on possible optimistic outcomes to Greece and Ukraine, Germany’s better-than-expected economic numbers, and oil’s continued recovery. Earnings season has had many pockets of strength, and that, combined with increased M&A activity, propelled several sectors and individual stocks higher.

The Wall Street Journal noted over the weekend that NASDAQ Index “heavyweights” such as Apple (AAPL), Amazon.com (AMZN), and Cisco Systems (CSCO) all have exceeded Street earnings expectations for Q4 and pushed the NASDAQ Composite ahead of the S&P 500 and Dow (DJIA) for 2015. The NASDAQ also outperformed last year, and as of last Friday (2/13), stood only about 3% below its all-time highs achieved on March 10, 2000. (Note: Cynics are quick to point out the disproportionate impact of Apple’s blockbuster earnings results on the overall S&P 500 Q4 numbers.)

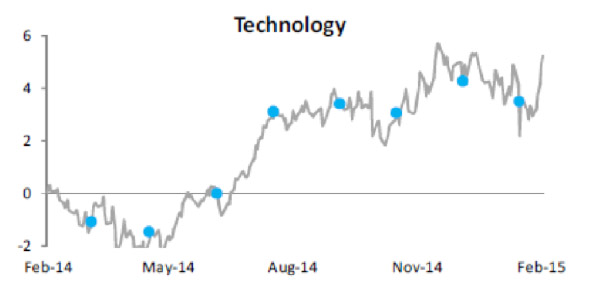

Bespoke Investment Group said in its weekly analysis that “this earnings season can be called the ‘comeback quarter,’ because many of the 2013 momentum stocks that had really gotten beaten down over the last six to nine months (including many technology names) have roared back to life.” The charts below show the recent trajectory of the S&P 500 and a relative strength chart for technology stocks, indicating the almost parabolic rise for the tech sector over the past few weeks.

Relative Strength Analysis

Source: Bespoke Investment Group (Note: Rising lines mean the sector is outperforming the S&P 500, and vice versa for falling lines. When readings are above 0, the sector is outperforming the S&P 500 at that point over the last year. Blue dots represent Fed Days.)

With the NASDAQ 100 (QQQ) recording gains of 5.7% for the month of February, up 3.7% last week, and essentially trading flat as I write this midday on Tuesday (2/17), perhaps there is a good chance Bespoke’s analysis will still be on the mark by the time you read this. Of course, in this world of constant uncertainty, I am not necessarily counting on it.

Have a great week,

David