“Any science or technology which is sufficiently advanced is indistinguishable from magic.”

– Arthur C. Clarke

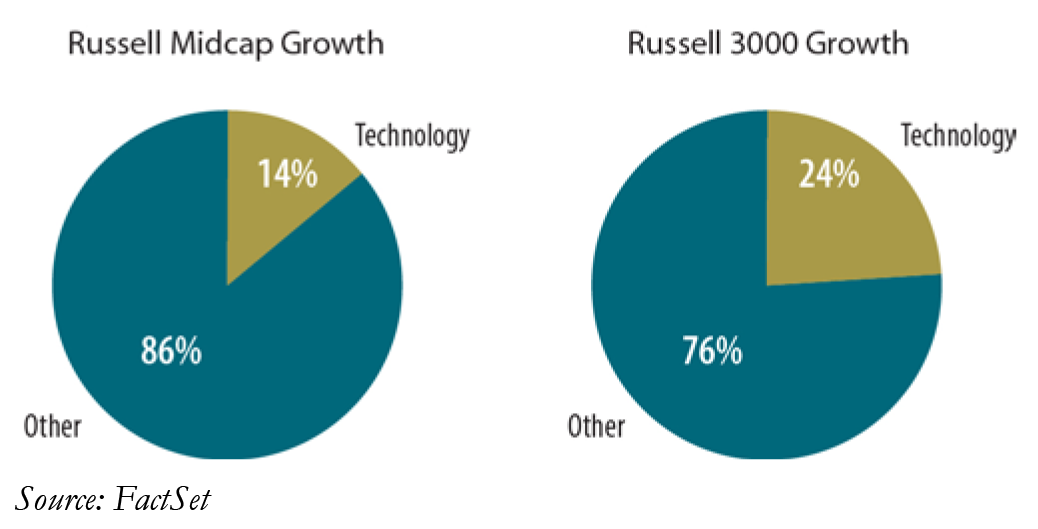

Technology is an important sector for growth portfolios - it carries a significant weight in major growth benchmarks, and more importantly, tends to be a ripe area for stock picking. The technology sector represents nearly 15% of the Russell Midcap Growth benchmark and 24% of the Russell 3000 Growth benchmark (see graphs below). The percentage is even higher when including Internet stocks that are categorized into the Consumer Discretionary sector. The technology sector is laden with innovative companies that are disrupting many areas of the market, and generating long-term growth and returns for investors along the way. Fortunately for American investors, the U.S. continues to be the global innovation leader, consistently churning out new technology companies that increase efficiency and competitiveness of corporations, and change the way consumers live, buy and communicate.

Mid Cap Growth Technology Approach

Mid-cap technology companies typically have proven technology, a developed customer base, seasoned management teams, and already feature solid profit margins. Yet, they are small enough to have the potential to generate meaningful growth (in excess of 20% in many cases) for an extended period of time. As such, we believe the mid-cap range offers a large, high-quality opportunity set in the technology sector. Additionally, mid-cap tech companies make attractive acquisition targets for larger tech companies and less often, private equity buyers.

The technology sector consists of a number of diverse industries including software, IT hardware, communications technology, telco equipment, and semiconductors, each of which has unique characteristics and a different set of winners and losers. Certain internet companies, which we view as being part of technology, are categorized by the indices into consumer discretionary.

At an industry level, in the Baird Investment Management (BIM) Mid Cap Growth strategy, we favor enterprise software and internet companies over IT hardware and communications/telco equipment companies, as they tend to feature faster growth, higher levels of recurring revenue, and solid balance sheets, and hence make better long-term investments. We also favor the semiconductor space, given high barriers to entry, recent consolidation, and above-GDP market growth given increasing use of silicon in a broad range of applications such as autos, and industrial machinery (see chart below).

BIM Mid-Cap Growth – Positioning in the Tech Sector

|

Russell Industry within Tech Sector |

As a % of Tech Sector Weight |

Average Revenue Growth |

Average EBIT Margin |

Average Debt/ EBITA |

|

|

Benchmark |

BIM Mid Cap Growth |

||||

|

Computer Services Software & Systems |

50% |

65% |

18% |

15% |

1.60x |

|

Semiconductors & Components |

23% |

25% |

10% |

20% |

1.64x |

|

Other |

27% |

10% |

7% |

19% |

1.74x |

|

100% |

100% |

With all its positives, technology (mid-cap or otherwise) can also be a difficult sector for investors, given the rapid pace of change, and the large role that sentiment plays in stock valuations. Our mid cap growth investment strategy in technology is consistent with our overall strategy of using bottom-up fundamental research to pick profitable companies with solid long-term growth prospects, robust balance sheets, and strong management teams. In addition to these guiding principles, we believe long-term secular trends are an important driving factor of long-term outperformance in technology. As such, we align our technology portfolio to benefit from key technology trends, some of which we discuss below.

Key Technology Themes

We outline three broad secular technology trends in this whitepaper, each of which has implications across multiple technology industries. We view these as multi-year trends that will enable well-positioned companies to outperform in the long run and attempt to offer incremental perspective that you may not get from your daily news sources. We discuss below how the mid cap growth portfolio is positioned to benefit from each of these trends, and highlight one idea under each theme.

#1: Public Cloud

While it may seem like cloud is an overhyped buzz word and that we should now be moving on and looking at what the next big enterprise technology trend might be, we actually believe that we remain in the early innings of cloud adoption and that we only recently hit an inflection point in acceptance. Industry analysts estimate that cloud still represents less than 10% of enterprise IT spend today, and as such we see a long growth runway for cloud companies.

Enterprise technology goes through a platform shift every decade or so. The mainframe was the dominant technology in the ‘70s, the client-server in the ‘80s, and today it is the cloud. Public cloud saw early uptake by consumers and small businesses, and only since 2010 have large enterprises begun to embrace the cloud. For example, General Electric’s (GE) CIO recently noted that the company plans to eventually reduce its owned and operated data centers by 90% and replace them with public cloud services. U.S. Federal and local governments (and international governments) are even behind in cloud adoption. Federal and local governments are now looking to leverage public cloud services to increase efficiency and reduce cost in a flat budget environment. At a recent conference we attended, the CIO of a large federal department said he expects his cloud spending to go from 2% to over 10% of budget over the next 5-10 years.

We believe enterprise Software-as-a-Service (SaaS) companies offer the best business models in the cloud. These companies deliver software over the internet, and price their software on a recurring subscription basis. SaaS companies eliminate the need for customers to buy and maintain their own hardware, and offer the flexibility to scale up or down as necessary, while paying only for what they use.

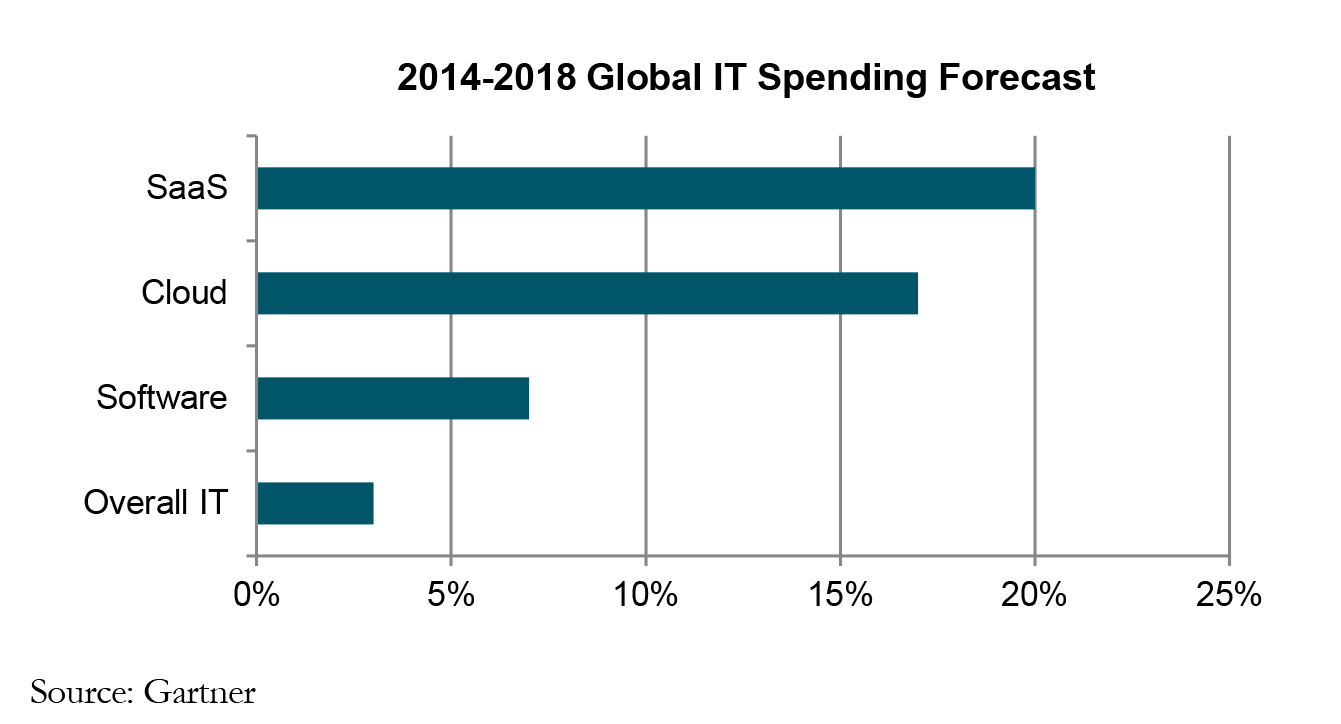

In addition to providing superior technology to customers, SaaS companies also offer a solid business model for investors. SaaS companies typically feature strong top-line growth, high recurring revenue, strong cash, and robust balance sheets. Industry research firm Gartner (IT) forecasts total cloud services spending to grow at a compound annual growth rate (CAGR) of 17%, and SaaS spending to grow at a CAGR of 21% for 2014- 2018, reflecting our own positive view of long-term growth opportunities in this space.

We view ServiceNow (NOW) as a high-quality SaaS company that is well-positioned to benefit from the shift to cloud. The company offers software to service-oriented departments in large enterprises, including IT, facilities and human resources. ServiceNow has an excellent competitive positioning as the dominant cloud enterprise SaaS vendor in its markets. We believe the company has strong competitive barriers given the company’s best-in-class software, delivery infrastructure, and high-quality customer base. ServiceNow also features a solid business model with over 80% recurring revenue, and over 90% renewal rates. The company generated over 60% revenue growth in 2014 driven by healthy new customer adoption, and expanding use with existing customers.

We view ServiceNow (NOW) as a high-quality SaaS company that is well-positioned to benefit from the shift to cloud. The company offers software to service-oriented departments in large enterprises, including IT, facilities and human resources. ServiceNow has an excellent competitive positioning as the dominant cloud enterprise SaaS vendor in its markets. We believe the company has strong competitive barriers given the company’s best-in-class software, delivery infrastructure, and high-quality customer base. ServiceNow also features a solid business model with over 80% recurring revenue, and over 90% renewal rates. The company generated over 60% revenue growth in 2014 driven by healthy new customer adoption, and expanding use with existing customers.

#2: Mobile

The first thought that comes to mind when we discuss investing in mobility is likely mobile devices. While mobile phone and smartphone penetration is expected to continue to increase, average selling prices are actually on the decline, and smartphone shipment growth is expected to slow to single digits from the current rate of 20%+ growth by 2018. As such, we believe the best way to play this trend in the mid-cap space is actually not through mobile device vendors, but rather via semiconductor and Internet companies.

Mobility is an important trend in the semiconductor space, creating massive growth opportunities for suppliers to handset vendors and to telecom infrastructure providers. Among suppliers to handset manufacturers, a number of semi vendors are positioned to continue to benefit from the success of key players such as Apple. Additionally, the dollar content for certain semiconductor suppliers goes up meaningfully with each generation of phones, and mobile phone technologies shift from feature phones to smartphones, from 2G to 3G, and 3G to 4G, especially in emerging markets. Additionally, as developing markets (primarily China and India) build out their 4G coverage, and U.S. and Europe continue to invest in 4G (and 5G in the future), semiconductor companies that supply chips to telecom base-station manufacturers should also benefit. New technology features that are being added to mobile devices include fingerprint sensing and wireless charging, which offers new opportunities for well-positioned semiconductor companies.

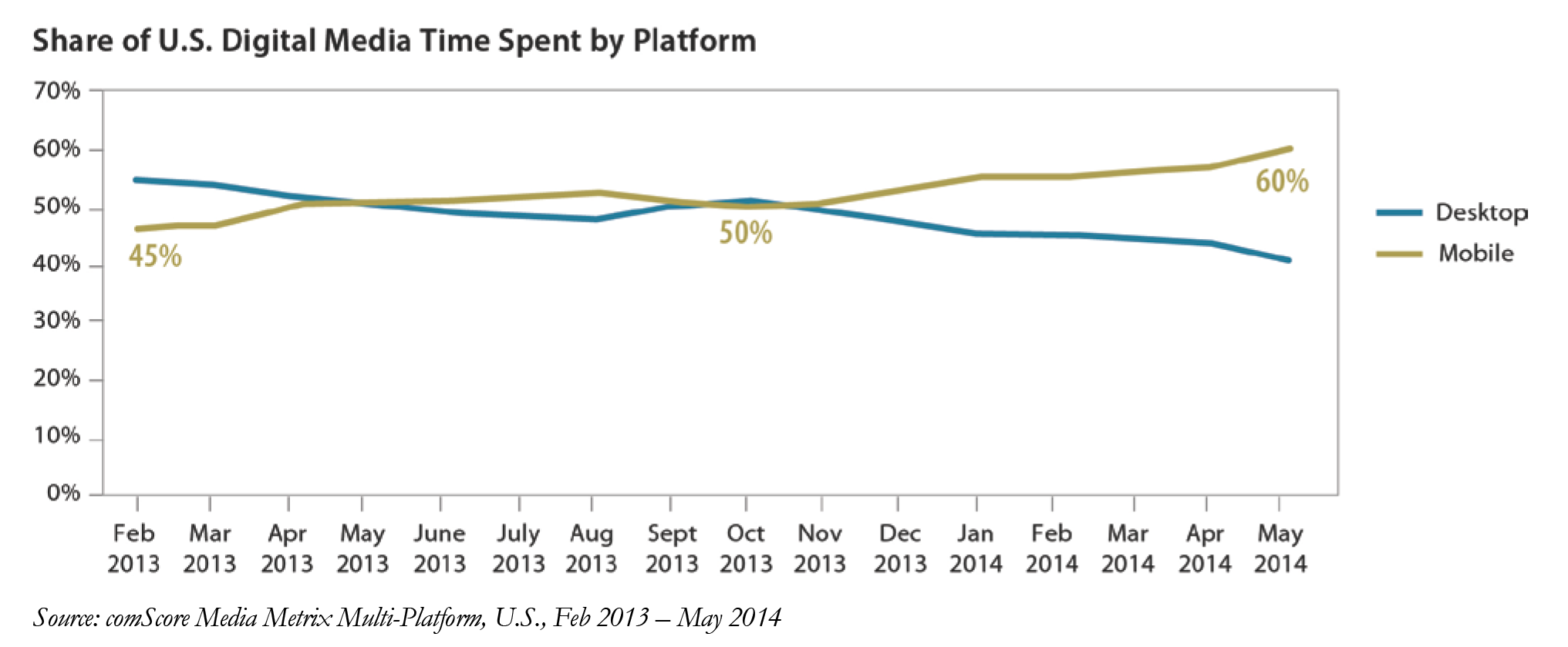

In the Internet sector, over the last five years, there has been a drastic change in how consumers use the web. Today, 60% of digital time is spent on mobile devices (see graph below) in the United States. However, mobile is less than 20% of online spending. As such, companies are shifting their digital marketing spend from desktop to mobile. This trend has meaningful implications for the Internet space, rewarding companies that can continue to grow in an increasingly mobile world while punishing those that are tied to traditional ways of consuming the Internet i.e., PCs and laptops.

Skyworks (SWKS) is an example of a semiconductor company benefiting from growing mobile consumption. Skyworks is a radio frequency (RF) chip vendor that is seeing strong growth from content gains in next-generation phones from Apple, Samsung and Chinese handset vendors. As smartphones try to cater to an increasing number of technologies (2G, 3G, 4G, etc.) and a broader range of frequencies, the complexity of the RF technology is increasing exponentially. This increasing complexity works in Skyworks’ favor as the company has stronger competitive positioning at the high end, in addition to seeing increasing dollar content per device. Additionally, the company is well-positioned to benefit from the Internet of Things (IoT) trend as a supplier of chips for wi-fi connectivity.

Skyworks (SWKS) is an example of a semiconductor company benefiting from growing mobile consumption. Skyworks is a radio frequency (RF) chip vendor that is seeing strong growth from content gains in next-generation phones from Apple, Samsung and Chinese handset vendors. As smartphones try to cater to an increasing number of technologies (2G, 3G, 4G, etc.) and a broader range of frequencies, the complexity of the RF technology is increasing exponentially. This increasing complexity works in Skyworks’ favor as the company has stronger competitive positioning at the high end, in addition to seeing increasing dollar content per device. Additionally, the company is well-positioned to benefit from the Internet of Things (IoT) trend as a supplier of chips for wi-fi connectivity.

#3: IT Security

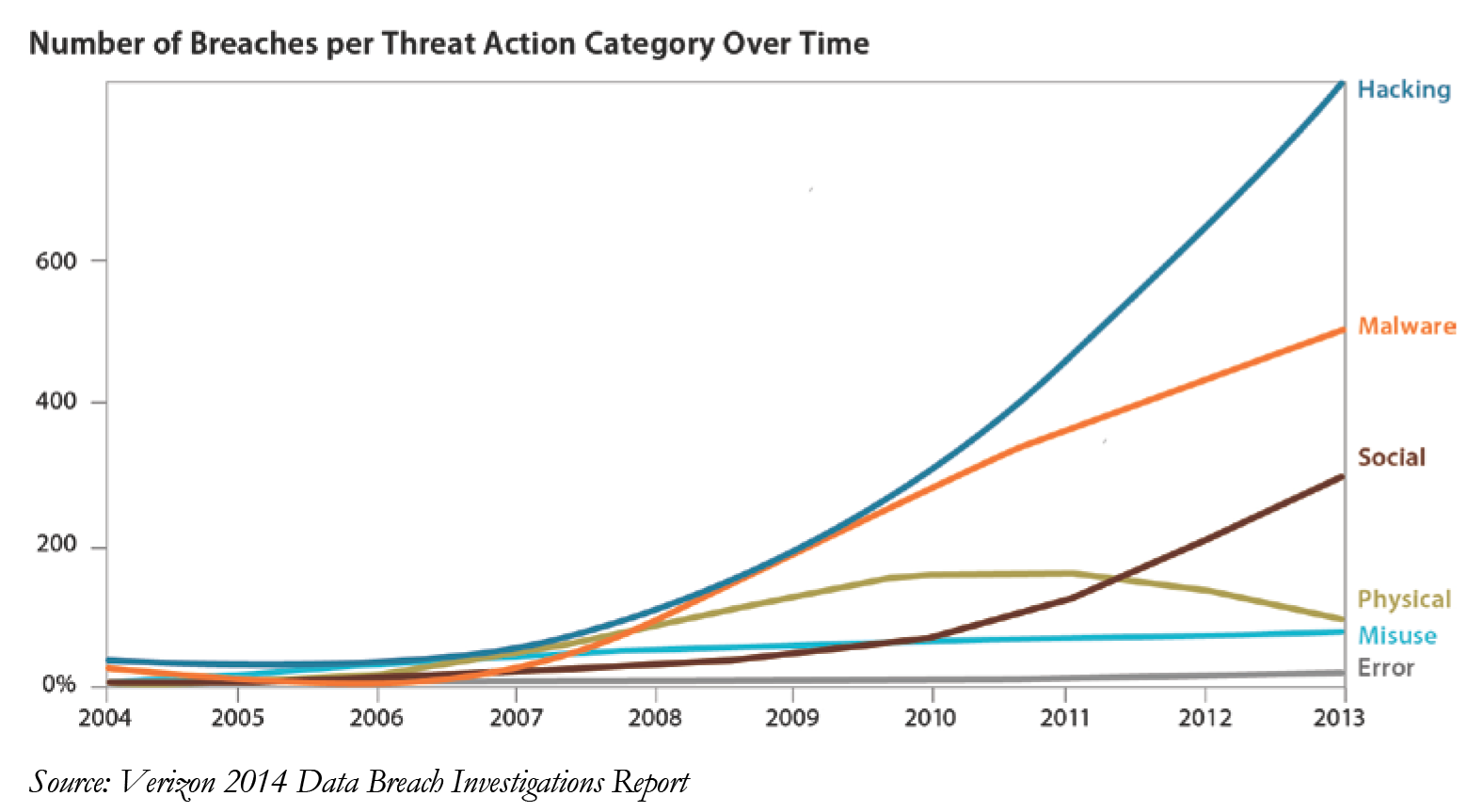

A company’s most valuable information is now likely being stored digitally. This information can include customer credit card numbers, employee and customer personal data, financial forecasts, and executive email communications. Additionally, a company’s network is mostly likely connected to the internet, making these digital assets available to digital criminals anywhere in the world. Meanwhile, hackers are becoming increasingly sophisticated and are receiving ample funding to carry out malicious attacks.

Targeted and successful attacks on large companies like Target, Home Depot, J.P. Morgan and Sony Pictures, have demonstrated the far-reaching consequences of a security breach, and have elevated the importance of IT Security to CEO- and board-level discussions. Given the increasing complexity of company networks and the growing complexity of attacks, we believe IT security will remain a priority for CIOs and CEOs, and see a growing share of IT spending. IT security is a large $70B market, and is expected to grow faster than IT spending, at a CAGR of 8% during 2014-2018 according to Gartner.

Among IT security vendors, we like Fortinet (FTNT), which is a UTM (Unified Threat Machine) vendor that offers multiple security features in a single machine, including network firewall, web filtering, and VPN among others. The company leverages its own custom chip to offer the best price-performance among security vendors. Fortinet had traditionally focused on Small-and-Mid-sized businesses, but has seen increasing traction in the enterprise market in recent quarters. Fortinet is seeing accelerating revenue and billings growth driven by stepped-up sales and marketing spending, as well as the strong security spending environment.

Among IT security vendors, we like Fortinet (FTNT), which is a UTM (Unified Threat Machine) vendor that offers multiple security features in a single machine, including network firewall, web filtering, and VPN among others. The company leverages its own custom chip to offer the best price-performance among security vendors. Fortinet had traditionally focused on Small-and-Mid-sized businesses, but has seen increasing traction in the enterprise market in recent quarters. Fortinet is seeing accelerating revenue and billings growth driven by stepped-up sales and marketing spending, as well as the strong security spending environment.

Conclusion

To wrap up, we believe the mid-cap space offers a rich opportunity set for picking technology stocks, given the more mature and proven stage of the companies which also have a long runway for growth. Technology is an important sector for growth investors given the significant allocation in benchmarks, as well as the opportunity to add alpha with long-term secular growth stories.

In our BIM Mid Cap Growth portfolio, we recognize in our approach to technology investing the important role that secular trends play in driving long-term growth while also staying true to our investment philosophy of being long-term focused and picking high-quality stocks that feature strong profit margins and solid balance sheets.

The Baird Mid Cap strategy is available as a separately managed account (SMA) and a mutual fund. Investors should consider the investment objectives, risks, charges and expenses of the SMA and the fund carefully before investing. This and other information can be found in the SMA’s ADV or the fund’s prospectus or summary prospectus. An ADV may be obtained by calling 800-444-9102 and a prospectus or summary prospectus may be obtained by visiting bairdfunds.com. Please read the ADV and prospectus or summary prospectus carefully before you invest or send money.

The Baird Mid Cap Fund focuses on growth style stocks and therefore the performance of the SMA and fund will typically be more volatile than the performance of SMAs or funds that focus on types of stocks that have a broader investment style. The fund may invest up to 15% of its total assets in U.S. dollar denominated foreign securities and ADRs. Foreign investments involve additional risks such as currency rate fluctuations and the potential for political and economic instability, and different and sometimes less strict financial reporting standards and regulation.

This is not a complete analysis of every material fact regarding any company, industry or security and the mention of specific securities is not intended as a recommendation or offer for a particular security. Further, the opinions expressed here reflect our judgment at this date and are subject to change. Baird makes a market in the securities of ServiceNow, Skyworks and Fortinet. Please select these links for performance current to the most-recent quarter end for the SMA and the fund.

©2015 Robert W. Baird & Co. Incorporated. Member SIPC.

First Use: 04/2015