Investment manager styles, like markets, move in cycles. So as investment advisors, we try to identify where we are in the market cycle to choose the best managers. Decision making should not be binary – “I like the market or I don’t like the market,” with a resulting buy or sell decision. In downturns, the normal reaction is to sell out of the market rather than looking at how to stay in the market and become more defensive.

In fact, being out of the market negatively impacts results over time.

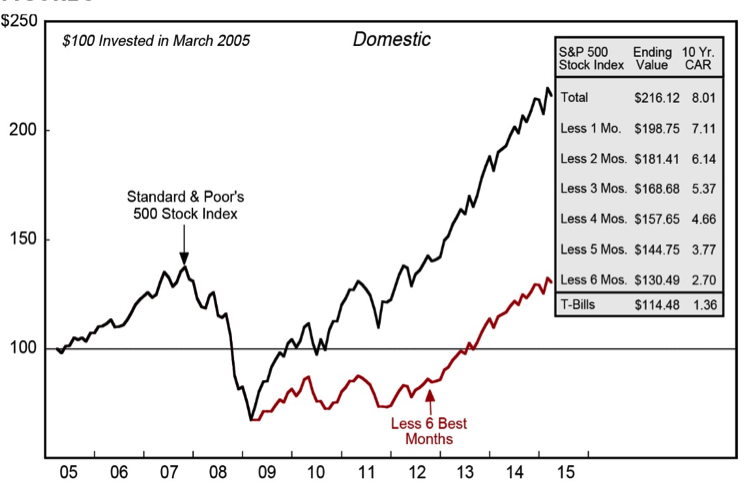

Figure 1

Source: Crandall, Pierce & Company

If we look at attempts at market timing, you can see in Figure 1 the returns for the S&P 500 Index over the last 10 years when the market returned 8% over that period. If you missed just the one best month, the return drops to 7.1%. If you missed just the top 6 months of the 120 months in this period, the return drops to 2%. Trying to time the market by getting in and getting out doesn’t make sense. Instead, we make an effort to allocate to different approaches or styles to manage downturns, rather than selling out completely.

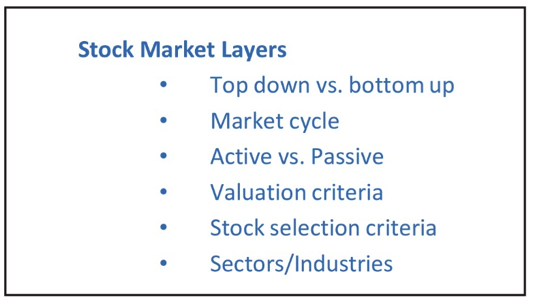

When we consider the variety of investment strategies and different approaches managers take, we see the market in various layers (see Figure 2). Each of these layers offers a method to express what is happening in the market at that time.

Figure 2

Source: Cleary Gull

ON THE ECONOMIC CYCLE

We begin by looking at where we are in the economic cycle. With the exception of commodities, most asset classes have done pretty well over the past couple of years, with both U.S. stocks and bonds up dramatically. Even real estate has gone up significantly. But how each asset class performs varies based on where we are in the cycle.

If we review the last five stock market declines of 15% or more, some patterns begin to emerge. Before a downturn, we see a relative outperformance by intermediate bonds as an asset class. However, after the downturn, we see that intermediate bonds fall to the bottom in relative performance and that intuitively makes sense. But perhaps less obvious, small cap stocks underperform in the three months before a drop, while after the drop, it is one of the best relative performers as an asset class. Another similar cycle can be seen in the relative out-performance of growth stocks compared to value stocks after a major downturn.

ON ACTIVE VS. PASSIVE MANAGEMENT

When the market is on an upswing, people get focused on how well the S&P 500 Index has performed, and lean toward passive management, which simply tracks an index’s performance. But here again, it’s not just a binary decision, it’s not either/or. At Cleary Gull, we use both active and passive strategies, depending on the cycle. We ask ourselves whether we should be using more of one or the other at a given time in the markets, based on market breadth.

Figure 3

Source: Haver Analytics, Morningstar, Fidelity Investments

Figure 3 compares the relative breadth of the U.S. stock market to the rolling performance of active strategies. Historically, active stock management does better when there is more relative breadth in the market. When breadth is higher than 65%, active managers have outperformed the index 100% of the time and by an average excess return of 130 basis points. Active managers have done better from just before the peak through the trough. This is an example of a “layer” we will use as we construct portfolios over time.

ON DIFFERENT STYLES OF MANAGEMENT

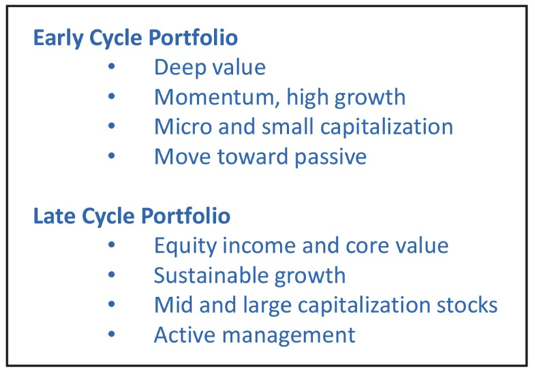

Another lever we can use is the combination of different management strategies in a portfolio. Again, we do not use an all in/all out approach, but by looking at the economic cycle, we can lean a portfolio in the direction of a more favorable or a more defensive positioning. An early cycle portfolio may differ significantly from a late cycle stock portfolio. In an early cycle portfolio, we have seen micro- and small-cap stocks do very well, as we saw in 2009. Particularly, small cap value stocks tend to do well in the early part of a cycle. As momentum builds, passive investments start to make more sense as all stocks tend to be rising. Passive investments historically do better than active in the early part of a market cycle.

In the late part of a market cycle, we see a relatively big change in historic performance, where small cap stocks fare less well than large cap stocks. Companies paying dividends have also done better in this stage. People begin to look for Growth At Reasonable Prices (GARP) strategies, which tend to perform better as people become concerned about earnings growth and profit margins. In the late part of the market cycle, breadth tends to be wide, with more stocks outperforming the index; and, active managers start to do better.

There are many layers to the stock market and many different strategies designed to take advantage of valuation differences. Our job is to understand economic and market cycles and to inform our thinking about how to construct a portfolio using those different strategies. It is very difficult to both be right often enough and make money over time by using an all-in/all-out market timing strategy. Instead we use these different layers in portfolio construction to lean in or lean out as we feel appropriate.

Source: Cleary Gull

ABOUT THE AUTHOR

Mr. Andrew is President and Chief Investment Officer of Cleary Gull. Cleary Gull (www.clearygull.com) is an SEC-registered investment advisory firm providing financial advice through two operating divisions: Investment Advisory Services and Investment Banking Services.