When I think of doubles, on the positive side I think of my years of playing doubles tennis, Miguel Cabrera winning a Tigers game with one, Stevie Ray Vaughan’s Double Trouble band, and even those commercial spots that started in 1959. You know the ones I’m talking about – the Doublemint® gum commercials.

When they first came out in the ‘50s, they had a catchy little jingle: “Double your pleasure, double your fun with Doublemint, Doublemint, Doublemint gum.” The ads always featured twins and were popular until 2011 when Wrigley finally dropped the twins from its commercials (those original twins are approaching 80 now). See the 70’s and 80’s peak in popularity version here. (BTW, in the original commercials, the girls were not allowed to actually chew the gum. In later versions, the young ladies could chew, but had to be taught how to gracefully place it in their mouths to do so.)

Most of the negative connotations of the word “double,” until lately, centered on the entertainment industry. The title “Double Trouble” has been nothing but for the artists behind the two films (1967 and 1992 versions) and one TV series (’84-’85 and starring a pair of former Doublemint twins) that used that title. In every case, it led to bad reviews and ratings (even though the earliest version featured “the King,” Elvis Presley).

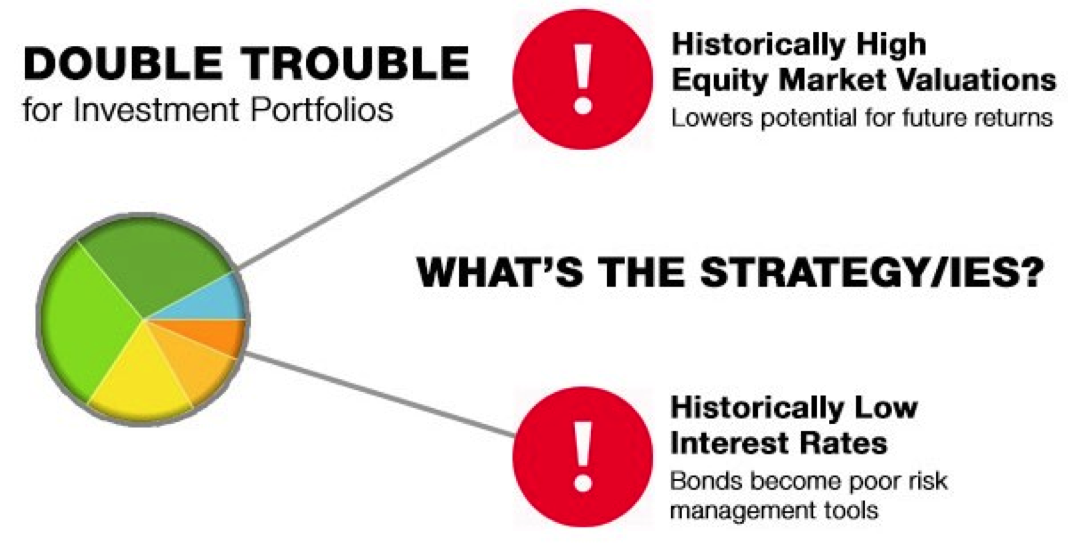

At our Sales Conference last week, one of the Regional Sales Managers (RSMs) showed off a chart that caught my attention and was entitled “Double Trouble.” And rightly so, as it shows that in the world of investments we have reached a point where we have stocks hitting new heights, with valuations believed by many to be too high to support further advancement. On the other hand, bond yields are at new record lows – a near “zero percent world” they call it. As such, rates have nowhere to go but up, and since bond prices go in the opposite direction as bond yields – bond prices will move lower.

The late, great market technician, David Elliot, used to lecture on a chart formation called an “ice hole failure.” I always think of the Houdini biopic when I think of this formation.

The master of illusion once did a stunt in Pittsburg where he jumped into a frozen river, handcuffed and chained within a steel box. He went under the ice, escaped in Houdini fashion, and then swam to the surface only to discover that he had floated downstream and the ice was solid above him. Fortunately, he was Houdini, and breathing from trapped air pockets under the ice, he was able to sustain himself until he found the original ice hole. Anyone else would have perished and sunk to the bottom.

That’s the same way David Elliot’s “ice hole failure” pattern works. When the price of a stock or bond falls through its 50-day moving average, it, at first, recovers back to the level of the moving average, but when it can’t find a way to break through, it sinks even lower.

Unfortunately, both stocks and bonds are exhibiting this pattern.

Source: Bespoke Investment Group

So we have “double trouble.” The two most popular asset choices seem to be primed for a fall. And I could pile on and point out that we really have a triple play (I love those baseball analogies), as the third most popular asset class, “commodities,” has already been falling for over a year.

What’s an investor to do? David Elliot would be the first to point out that these failure patterns do not assure that a decline is coming (like anything in the market, they don’t always work out).

And I’m here to tell you that based on over 40 years of market experience, I know that there is no cut-off or time schedule that you can rely on to trigger a sell or buy when markets are over or under valued. Markets can remain at such extremes longer than most expect! The great economist, John Maynard Keynes, was supposed to have said, “The market can stay irrational longer than you can stay solvent.”

So, while we’re in “double trouble,” we still don’t want to push away from the investment table too soon and leave too much on the table as a result. It’s at times like these that dynamically risk-managed accounts are most useful. These strategies not only can increase the percentage of your investment in a particular asset class, but can reduce it, as well. They can even go completely to cash during extreme events.

However, as the graphic from the conference asks, “How do you know ‘what strategy or strategies’ to choose to deal with double trouble?” While many will choose an all-purpose dynamic, risk-managed core strategy like our Fusion service, others have differing points of view and may want to tailor the strategy choice to their own view of each market or use a specialized strategy for each.

Firms like Flexible Plan Investment, Ltd. offer a range of strategies, each of which was developed to solve a different portfolio problem. There are tactical or rotational equity strategies to monitor and trade stock market investments, and the same for both the bond and alternative asset world.

The advantage of each of these strategies is that they do not leave the investor struggling in a box under water and ice; instead they all are designed to recognize when the odds for a further advance are smaller than those that call for a downturn. As a result, they allow investors to stay at the table longer and not be frightened away too early, while at the same time providing a pre-designed criteria for a historically probable place to exit.

At the present time, I agree with the expectation of a decline. Yet I don’t believe that the decline we will continue to experience until mid-summer will be so serious that drastic action like going to cash is warranted. Sometimes you can get out at the right time, but getting back in at a lower level when the market turns higher can be very tricky, even for professionals if they are being too short term in their outlook.

I have always focused on the intermediate term. While there have been a number of short-term signals that stocks are getting toppy, I believe we are looking at short-term weakness only. I do not see many signs of an intermediate-term decline of the 20% or greater variety like we saw in 2011. I guess I remain in the “buy the dip” crowd.

Supporting me in this view is the improving economic picture. Whether it is retail sales, employment, housing, or consumer and business confidence measures, all have finally turned higher. Valuations are closer to average levels than they are to bubble heights.

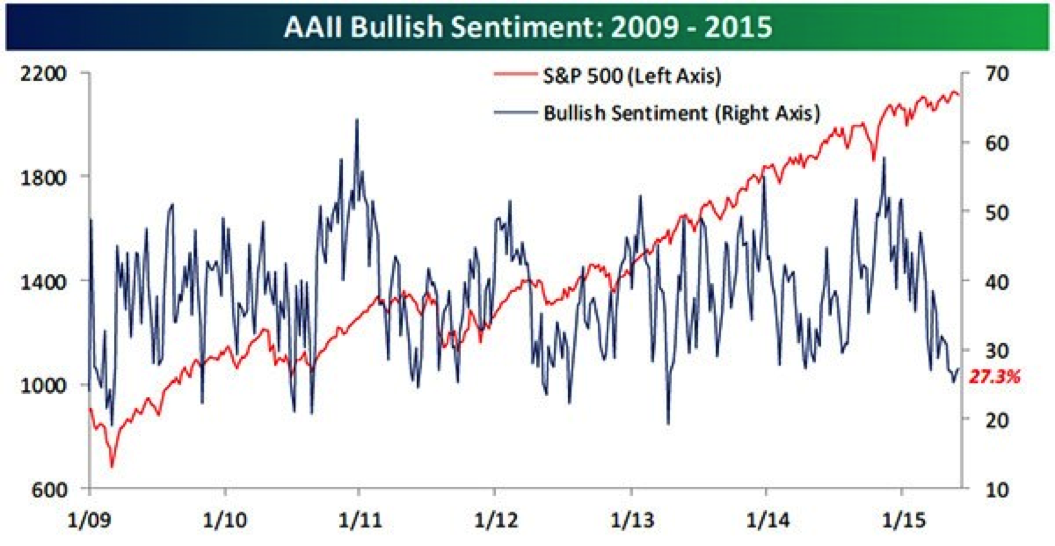

While seasonality is weak until month’s end, investor sentiment shows there are scarcely any bulls to be found. Bullish sentiment, as measured by the American Association of Individual Investors, is practically at levels not seen since the beginning of the bull market in March of 2009! While this can mean short-term weakness, in the longer term it tends to be a great time to buy.

Source: Bespoke Investment Group

Perhaps providing some technical support to offset the “ice hole failure” chart formation is the low-volatility formation that has developed so far this year. Believe it or not, prices have not moved more than 3.5% up or down from their starting price of the year.

We have never before in the almost 95-year history of the S&P 500 had such a condition exist this far into a year (108th day). Our friends at the Bespoke Investment Group report that in the past this has almost always led to higher stock market prices over the rest of the year. Of the ten closest incidents, all but one saw higher prices by the end of the year (average 4.87% higher).

As usual, the indicator picture is mixed, and with a Federal Reserve meeting this week and the prospect of a Greek default hanging over investors, I can understand the concerns. Although, just as these can negatively influence asset prices, the market can be a confounding place to try to predict the future and especially its reaction to any news. How often have you seen good news lead to lower prices and vice versa?

I find with my own investments that leaving the decision making to the quantified methodologies encoded into our dynamic, risk-managed strategies is a wiser course of action. Let them do their job and be the tie breaker when there is double trouble.

Still, I’m not crazy about anything that’s double trouble, unless it’s the Michigan-made craft brew that has won national acclaim – an Imperial IPA from Grand Rapids’ Founders Brewing Company named, you guessed it – Double Trouble.