Uncertainty Now; Opportunity Later: 2015 Economic & Stock Market Outlook, Mid-Year Update

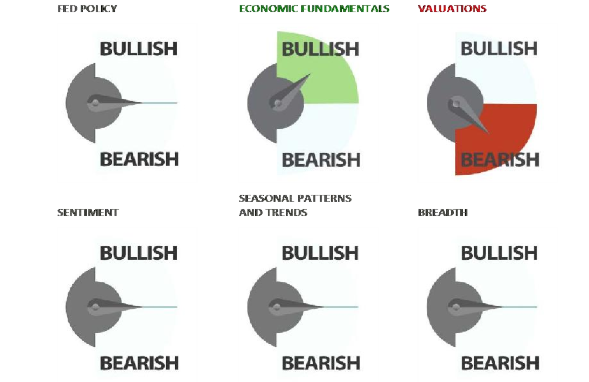

The weight of the evidence has slipped to neutral at mid-year as the bullish influences from Fed Policy and Seasonal Patterns/Trends present at the beginning of 2015 have waned. Sentiment has made a round trip from neutral to bearish and now back to neutral, while breadth rose from neutral to bullish and is now back to neutral. This is not inconsistent with a stock market (using the S&P 500 as a proxy) that has struggled to sustain gains. In such an environment, investors should be selective in looking for opportunities, be cautious of crowded trades, watch relative trends, and wait for confirmation.

The message at mid-year is caution now, but opportunity later. To be sure, we do not know how the second half will unfold, but it is not difficult to envision a more constructive environment as we move through the second half. If and when the Fed finally raises rates, conviction in a gradual tightening process could raise Fed policy back to bullish, and better seasonal patterns (and perhaps improved momentum) could be in store in the fourth quarter. On the other hand, a quick return of investor optimism and/or further breadth deterioration could add downside pressure in the near term.

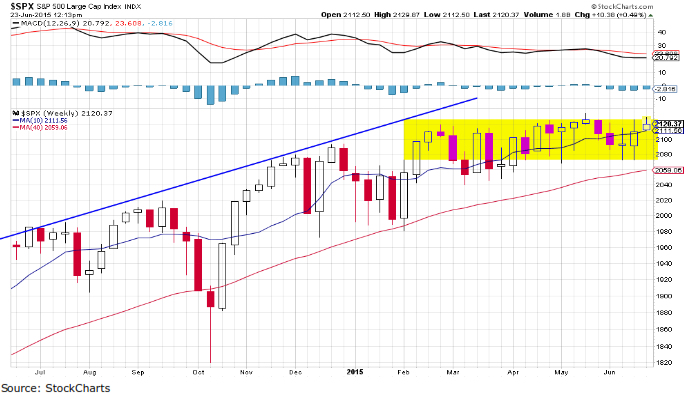

Chart 1: Uncertainty has risen as the S&P 500 has settled into a broad trading range

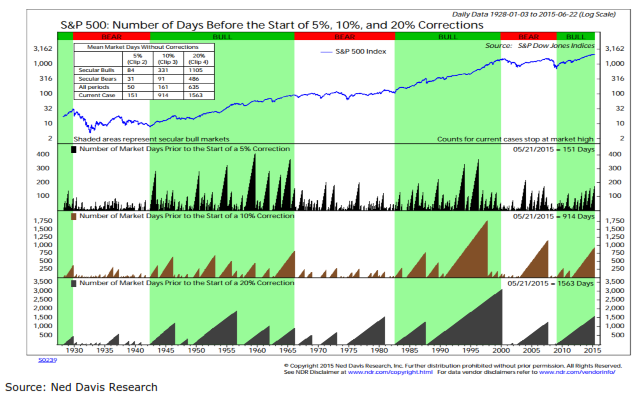

Chart 2: A correction is overdue, but that alone does not mean one is imminent

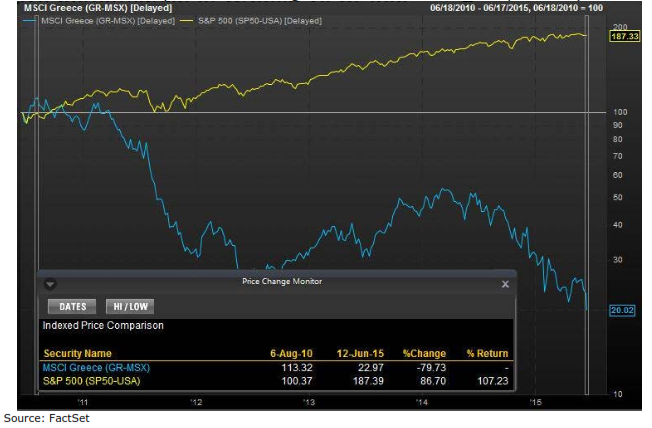

Chart 3: Should the focus really be on something [Greece] that is down 80% over the past five years?

Chart 4: Weight of the evidence has cooled to neutral on downgrades of Fed Policy & Seasonals

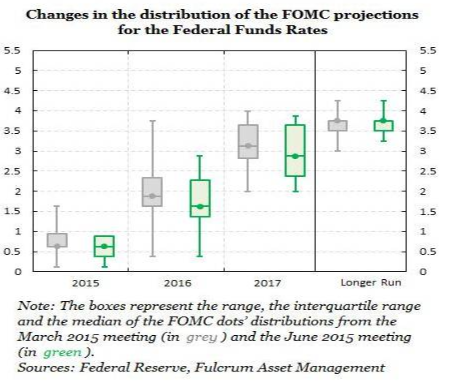

Chart 5: The Fed continues to expect to raise rates this year, but the path is lower for longer

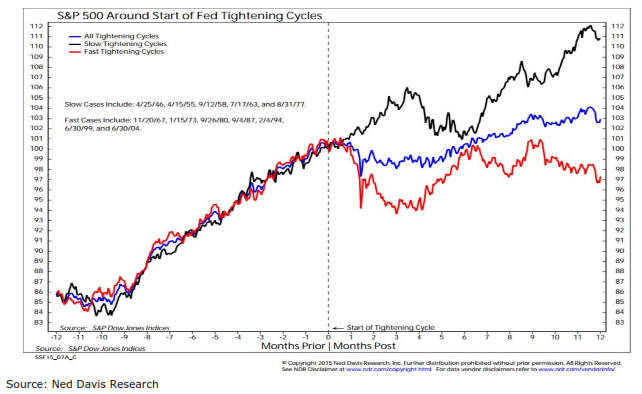

Chart 6: Too much can be made of the actual lift-off date, as stocks tend to weather it well

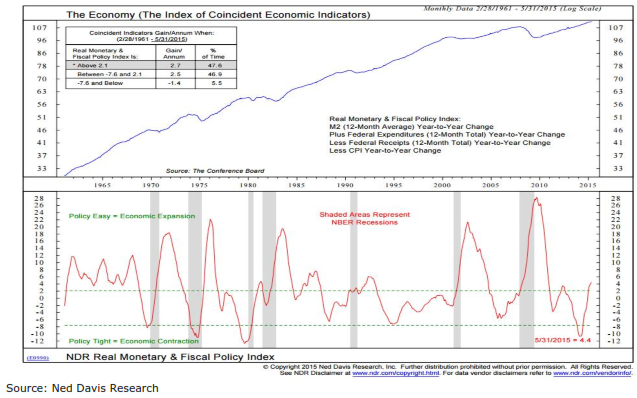

Chart 7: The overall policy back backdrop has become more supportive of economic growth

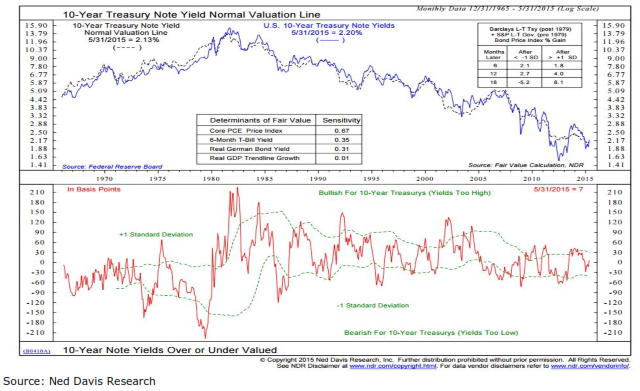

Chart 8: Based on key drivers, bond yields are about where they should be

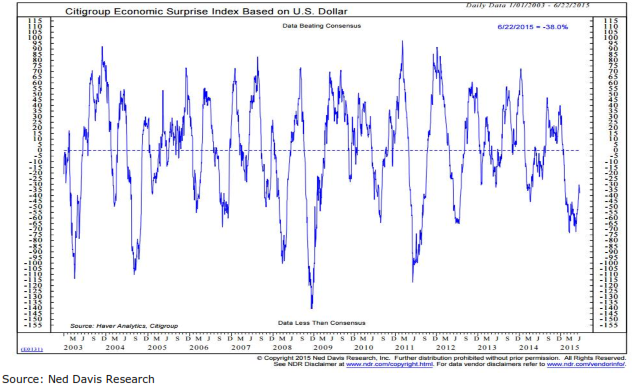

Chart 9: Economic performance has not matched expectations, but then it rarely does

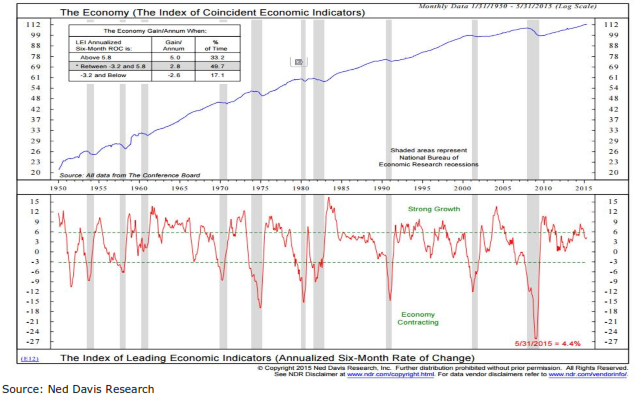

Chart 10: Leading indicators suggest the economy remains on solid footing

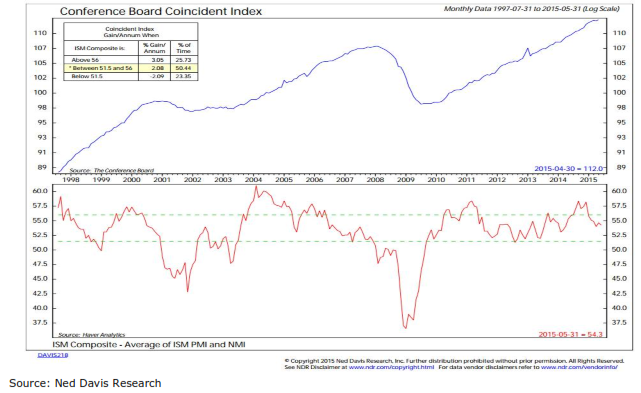

Chart 11: Business activity has moderated but not warning of weakness for the economy . . .

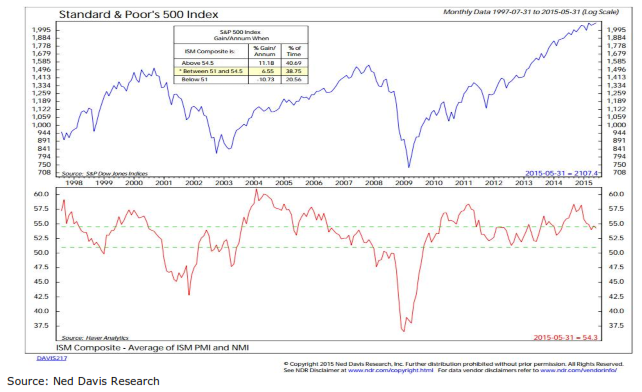

Chart 12: . . . or for stocks

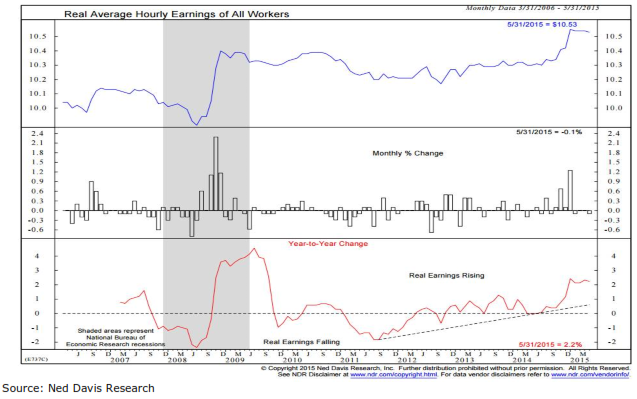

Chart 13: Improvement in wage growth speaks to a broadening economic recovery

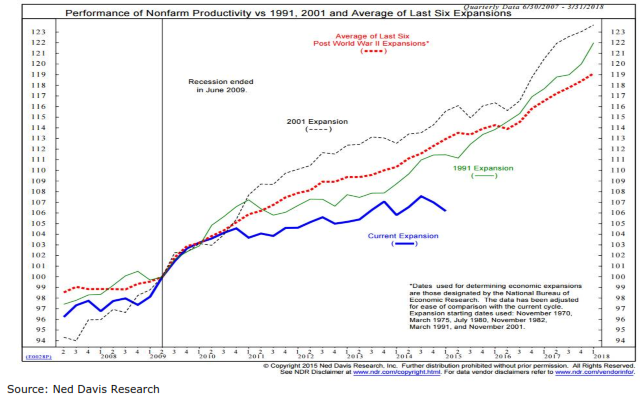

Chart 14: Rising wages could turn focus back to improving productivity

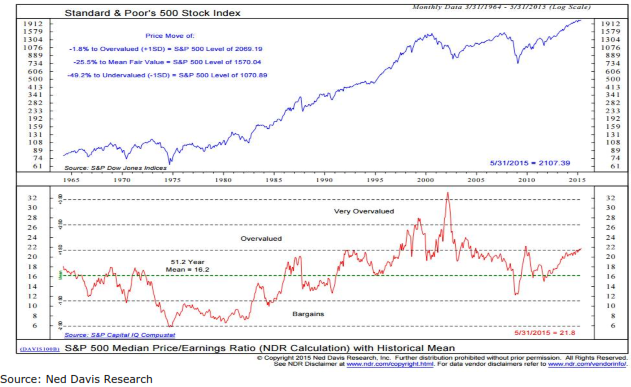

Chart 15: Stock market valuations are stretched

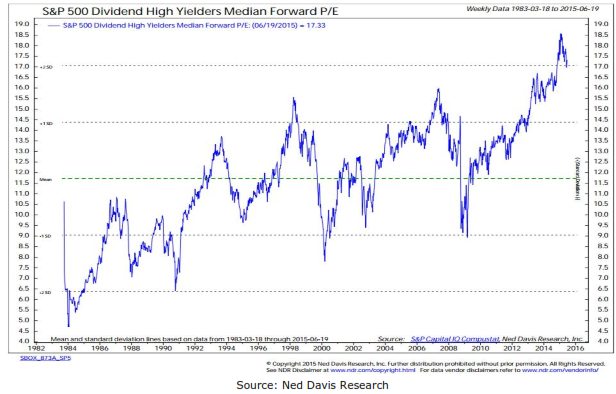

Chart 16: The reach for yield has left that market segment significantly over-valued

Chart 17: When sector adjustments are made, Europe’s valuation advantage disappears

Chart 18: Better earnings growth could relieve some valuation pressures

Chart 19: Heavy household exposure to stocks tends to depress returns going forward

Chart 20: News of less optimism is welcome, but still little evidence of increased liquidity

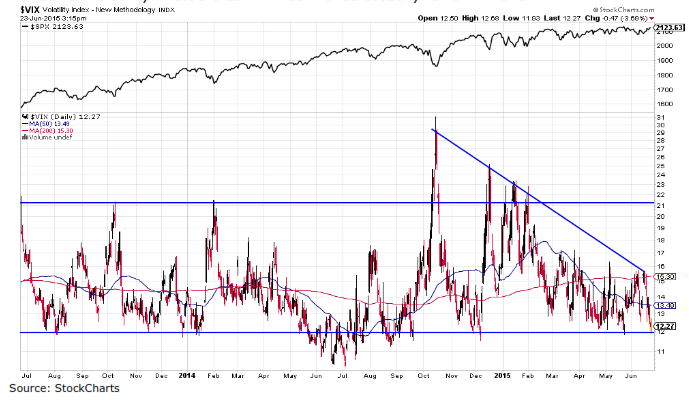

Chart 21: No fear or volatility in stocks as VIX has moved steadily lower in 2015

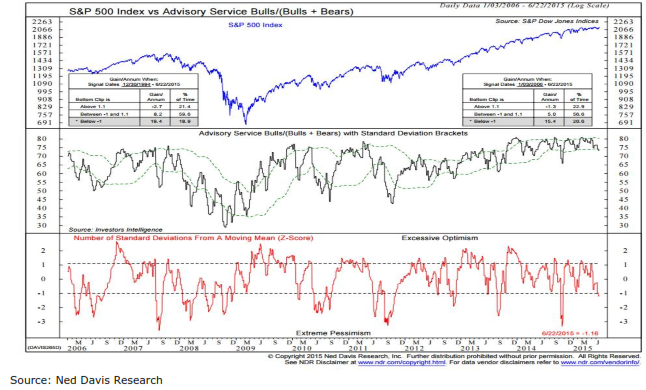

Chart 22: Investor optimism has retreated from recent highs, but is hardly historically low

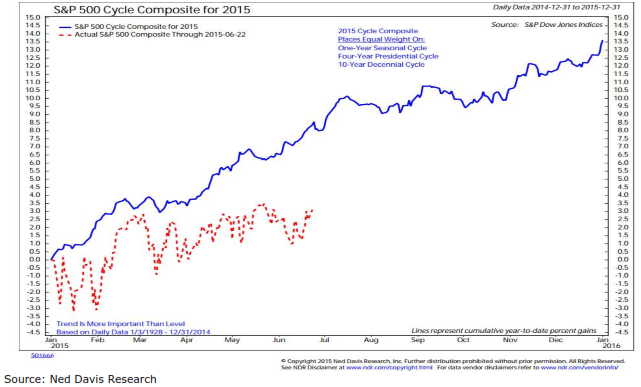

Chart 23: Expected seasonal tailwind for 2015 has not materialized

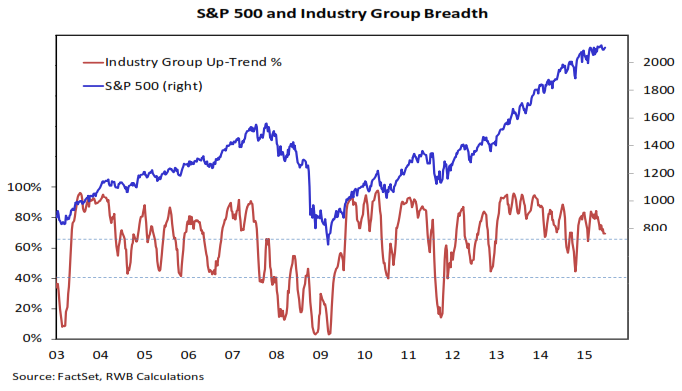

Chart 24: Industry group trend has faltered after early-year improvement

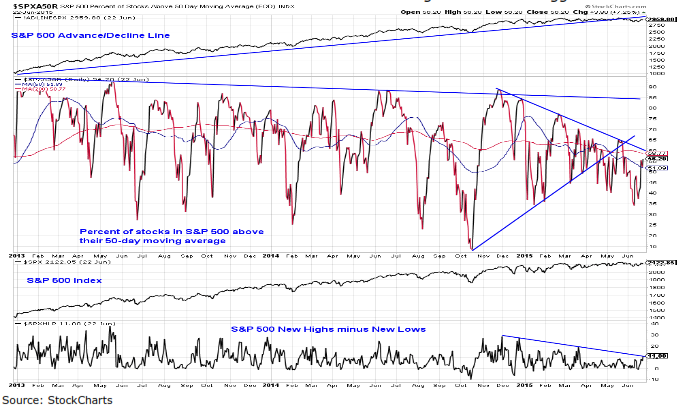

Chart 25: Breadth trends for the S&P 500 have cooled as the average stock has struggled

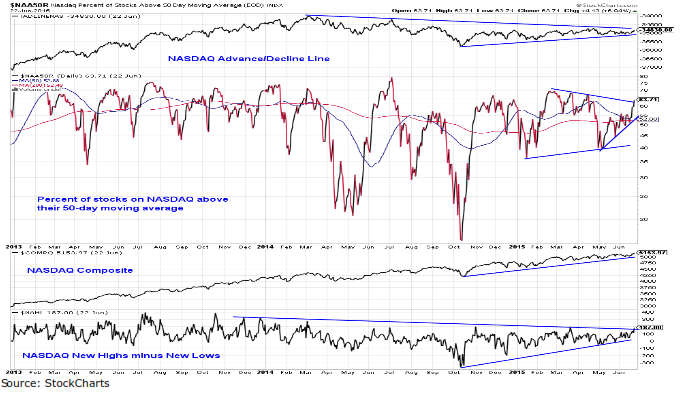

Chart 26: NASDAQ breadth trends are improving and on the cusp of breaking out

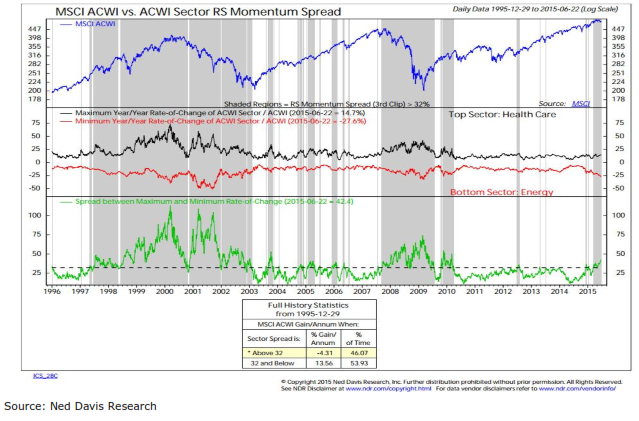

Chart 27: The dispersion of sector-level returns suggests stocks are out of gear

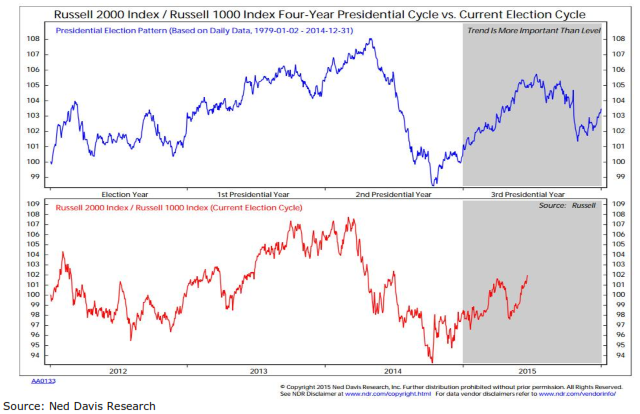

Chart 28: Small-cap leadership emerged in late-2014 and has persisted in 2015

Chart 29: Seasonal patterns could be a significant headwind for small-caps in the second half

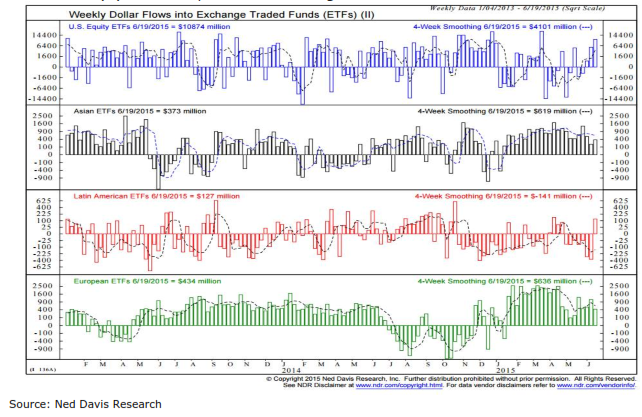

Chart 30: After an early-year hiatus, funds are flowing back to the U.S.

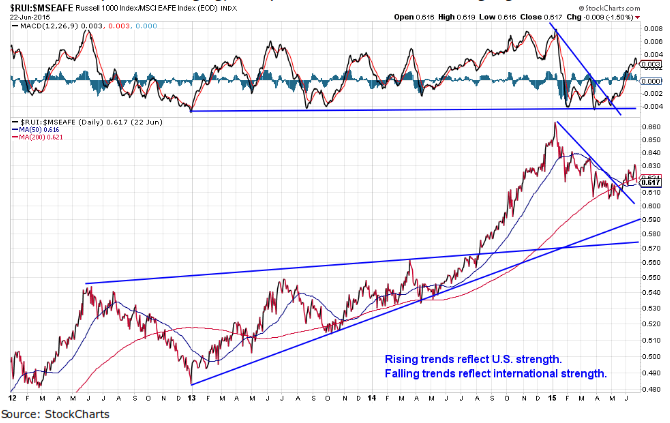

Chart 31: U.S. leadership is re-emerging, with price and momentum turning higher

Appendix – Important Disclosures

Disclaimers

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy.

Foreign and emerging market securities may be exposed to additional risks including currency fluctuation, political instability, foreign taxes and regulations and the potential for illiquid markets. Historically, small and mid-cap stocks have carried greater risk and have been more volatile than stocks of larger, more established companies.

ADDITIONAL INFORMATION ON COMPANIES MENTIONED HEREIN IS AVAILABLE UPON REQUEST.

The Dow Jones Industrial Average, S&P 500, S&P 400, MSCI EAFE, Lehman U.S. Aggregate Benchmark, Lehman Municipal Bond Benchmark, Russell 1000, Russell Mid Cap, Russell 2000, and Russell 3000 are unmanaged common stock indices used to measure and report performance of various sectors of the stock market; direct investment in indices is not available.

Baird is exempt from the requirement to hold an Australian financial services license. Baird is regulated by the United States Securities and Exchange Commission, FINRA, and various other self-regulatory organizations and those laws and regulations may differ from Australian laws. This report has been prepared in accordance with the laws and regulations governing United States broker-dealers and not Australian laws.

Other Disclosures

UK disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W Baird Limited holds an ISD passport.

This report is for distribution into the United Kingdom only to persons who fall within Article 19 or Article 49(2) of the Financial Services and Markets Act 2000 (financial promotion) order 2001 being persons who are investment professionals and may not be distributed to private clients. Issued in the United Kingdom by Robert W. Baird Limited, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB, and is a company authorized and regulated by the Financial Conduct Authority. For the purposes of the Financial Conduct Authority requirements, this investment research report is classified as objective.

Robert W Baird Limited ("RWBL") is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the Financial Conduct Authority ("FCA") under UK laws and those laws may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.

Copyright 2015 Robert W. Baird & Co. Incorporated.

www.rwbaird.com