We are regularly asked for our take on the broad macroeconomic topics of the day. Two of the more noteworthy big-picture subjects we have been asked about recently are the Greek debt crisis and the timing of the U.S. Federal Reserve rate hike. In most cases, we don’t believe we have new insights to add beyond the reams of commentary these topics typically inspire, and given the dynamic nature of these two topics, it is quite possible that new information will unfold as we publish this or shortly thereafter. However, we believe that walking through these examples will shed light on our current portfolio management priorities as well as the timeless strategies we apply throughout all investment environments.

We'll discuss three general points for each:

- How we think about these types of complex, overarching situations where the outcome is a true unknown

- How we are currently taking into account the outlook for Greece and for interest rates within our portfolios

- Our view on the situations themselves

The Greek Debt Crisis

As we write this, Greece is in the headlines as the deadline ticks closer for a broader debt default, if not outright exit from Europe’s Economic and Monetary Union, and the parties appear far apart in reaching a compromise. It’s possible that significant uncertainty will remain at least until July 20, the date Greece owes the European Central Bank a €3.5 billion bond payment. And even if there is a default at that point, the full implications (political as well as economic) will remain unclear for a long time to come.

It’s fascinating to watch this game of chicken play out on the global stage. Innumerable articles have been written on the various potential outcomes and consequences for financial markets and economies. But the truth is no one knows how the negotiations will actually play out.

This latest Greek crisis provides us with an opportunity to highlight how we think about these types of overarching, large-scale, and often complex events in the context of our investment process and portfolio management approach. (Other examples include the potential impacts and outcomes from national elections, central bank actions, and geopolitical conflicts). That is to say, we don’t make big portfolio bets on particular outcomes (e.g., Greece leaving the eurozone) unless we have

- a high level of conviction regarding a particular outcome and

- a high conviction view of how that outcome translates into a specific actionable investment opportunity and

- our view is meaningfully different from the consensus view already reflected in current financial asset prices and yields.

It’s very unlikely that all three of those necessary conditions will hold long enough for us to gain the necessary levels of conviction to act. Instead, our approach is to consider a range of potential outcomes (or macro risks) and then build portfolios that we believe are resilient and robust across this range.

Using the Greece situation to illustrate, our overall portfolio positioning is based on our expectations for returns and risk across a range of broad economic scenarios we consider to be reasonably likely. The range of scenarios includes best, worst, and baseline cases and, as a result, implicitly incorporates a range of outcomes from the negotiations with Greece. In other words, our current allocation is not based on an assumption that Greece would or would not default, nor on the duration of their tenure in Europe’s Economic and Monetary Union. The recent negative developments in Greece were already subsumed within the scenarios we evaluate. So as the events currently play out they have not led us to change our asset allocation positioning, although we expect some of our active bond and stock fund managers are responding more tactically to the recent events and attendant market volatility.

IMPLICATIONS FOR OUR POSITION IN EUROPEAN STOCKS

Our assessment remains that expected returns for European stocks are very attractive relative to U.S. stocks looking out over the next five years. Despite a rebound earlier this year, European stock market valuations and corporate earnings (which are well below their long-term trend) still have room to improve, both on absolute terms and relative to the United States. For example, the chart below shows the wide gap in net profit margins of non-financial companies in the eurozone compared to the United States. We don’t believe this wide a disparity is sustainable and believe it will adjust in favor of Europe over the next several years, whether or not Greece defaults or remains in the euro currency union.

|

|||

| Source: Capital Economics. |

The Greek situation may clearly lead to more market volatility over the near term, certainly on the downside if events unfold worse than the market currently expects. (Of course there is also potential for the market to be surprised on the upside if there is an unexpected agreement. Even if that happens, we think there is value to our clients in sharing our thought process and approach in the midst of the extreme uncertainty over the outcome of the negotiations.) However, we believe we have adequately factored a reasonable worst-case outcome into our 12-month downside stress test scenarios for our portfolios. (Specifically, in one such scenario we assume European stocks drop 25% over the 12-month time frame.) And we have not changed the longer-term assumptions that underlie our five-year expected return calculations.

OUR TAKE ON GREECE

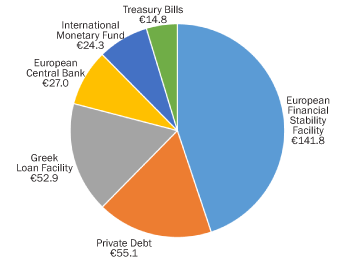

It’s important to keep Greece’s economic impact in perspective and to note that the risk of a Greek default in terms of its broader economic impact is reduced today relative to prior flare-ups of this question (though not eliminated, of course). As economist David Rosenberg wrote in his June 16, 2015, “Breakfast with Dave” column, “Remember that we are talking about a $240 billion economy here or 2% of the eurozone GDP [0.3% of global GDP].” Moreover, more than 80% of the total €315 billion Greek debt is held by government-related/taxpayer-supported entities, such as the ECB, International Monetary Fund, and the European Financial Stability Facility, according to data from Capital Economics. From a financial standpoint, these entities could handle a default although there would be political ramifications (just as there will be ramifications if Greece is bailed out again). Only 18% of Greek debt is held by the private sector and private banks, which is where the potential for financial contagion was a big concern just a few years ago. What’s more, these private sector-held bond maturities don’t start coming due until at least 2017. As such, according to Capital Economics’ June 16 European Economics Update, defaulting on this privately held debt would provide minimal benefit to Greece’s overall debt financing burden, yet would adversely impact the Greek banking sector, and so “for these reasons the Greek government has pledged that it will not default on its privately held debts.” In his June 18 column, Rosenberg also highlights some other key differences between the risks stemming from a Greek exit now versus a few years ago. “This is not 2010, nor is it 2012, when there was no ECB quantitative easing, when the peripheral euro area economy was far weaker, and the banks were saddled with Greek debt on their balance sheets.”

|

|||

| Source: Capital Economics. |

So for now we agree with the assessment that even if Greece exits the eurozone the risk of a financial contagion (e.g., “another Lehman” or a repeat of the subprime mortgage crisis) is low. However, markets may overreact if Greece looks increasingly likely to exit, and European stock prices could take a short-term hit. Indeed, the blue-chip EURO STOXX 50 Index has already dropped around 9.1% in local currency (euro) terms (as of 6/30/15) from its April high as concerns about the Greece negotiations have amplified.

That’s not to say that our assessment of the impact of Greece on our European asset class analysis can’t or won’t change. If, for example, Greece does default and leaves the currency union, and this leads to a significant increase in our assessment of the contagion risk that other peripheral European countries (such as Spain or Portugal) might do the same, then that could impact our scenario assumptions and/or expectations for risk and return, which would likely lead us to adjust our portfolio positioning. Of course, the financial markets will be reacting to (and pricing in) these developments in real time as well.

The Fed’s Much-Discussed Rate Hike

Another source of uncertainty and potential market volatility is Fed monetary policy. While we acknowledge that central bank actions (as well as Fed governors’ speeches) obviously do impact financial markets on a day-to-day basis, we also firmly believe it’s foolhardy for long-term investors to base investment decisions or portfolio allocations on short-term predictions of central bank behavior. (The same general rationale applies to what we wrote above in the context of the Greece crisis.) More specifically, as we’ve noted before, it’s pretty clear the central bankers themselves often don’t know what they’re going to do next or when they’re going to do it. And it’s often not obvious what the market’s reaction will be. Even Fed Board Chair Janet Yellen acknowledged this recently. When she was asked about the potential for market volatility if and when the Fed raises rates, she responded, “I think our experience suggests that it’s hard to have great confidence in predicting what the market reaction will be to Fed decisions, and there have been surprises in the past.” So while the guessing game over when the Fed will start raising interest rates can be entertaining (at least for economists), it’s largely irrelevant to our investment approach.

That is not to say we ignore what the Fed says and does or how the markets react to it. It’s possible a short-term market overreaction might create an investment opportunity based on our longer-term analytical horizon, or a market response might amplify a macro risk that we’d want to protect against. But that’s not the case presently, where the Federal Open Market Committee’s most recent policy statement on June 18 indicated the Fed still expects to hike rates this year. (A historical note: the last Fed rate hike was in June 2006, making this already the longest period between Fed tightening cycles since at least the 1940s.) Yellen also reiterated that the actual decision remains dependent on the Fed’s assessment of incoming economic data, particularly with regard to the labor market and inflation. Yellen was also very clear (again) in stating that even once they begin, the Fed expects the pace of rate increases to be very gradual (although that too could change depending on the data). In the grand scheme of things, the path or trajectory of rate increases is much more important than whether the first 25 basis point rate hike happens in September, December, or early next year. So the bottom line is we aren’t changing our portfolio allocations in response to the latest Fed statements or the market’s reaction to those statements.

IMPLICATIONS FOR OUR POSITIONS IN U.S. STOCKS

As with any market response to new developments regarding Greece’s debt issues, how stocks will respond over the short term if and when the Fed begins raising rates is also an unknown. So, here too we aren’t basing our portfolio positioning on a specific view of the likely outcome. We remain conservatively weighted to U.S. stocks in our balanced portfolios as the potential returns looking out across our five-year investment time period are not high enough to fully compensate us for the risks. Our positioning is not a short-term bet that stocks will drop when the Fed starts raising rates.

In fact, history suggests the beginning of a Fed rate-hike period is unlikely to trigger a major stock market plunge or mark the beginning of a bear market—particularly if the Fed has convinced the markets it will be unusually gradual in its pace of tightening. That said, this has not been a typical monetary policy cycle (to say the least!) and with the federal funds rate pinned at or near zero for six-and-a-half years, the first moves off of that may increase market volatility and could be a catalyst for a market “correction” (i.e., something on the order of a 10% decline). Based on history alone, we are overdue for one. The S&P 500 has now gone almost four years (45 months) without at least a 10% decline, making this the third longest such stretch since World War II. Prior to this recent run, market corrections occurred roughly once a year, on average. We note all of this not as a short-term market prediction, but as a plausible shorter-term scenario to be aware of and prepared for.

|

|||

| Source: Federal Reserve. Data as of 6/19/2015. |

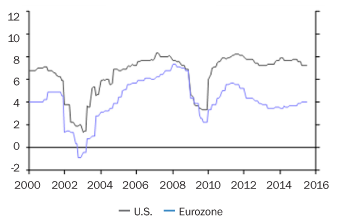

Typically it takes a sustained increase in rates by the Fed for a full-on bear market to ensue (i.e., a 20%–25% or more drop), with such downturns having often occurred only after the Treasury bond yield curve has inverted (i.e., when yields on very short-maturity bonds are higher than yields on long-maturity bonds) and/or the market has started anticipating a recession is in the offing. Right now the yield curve remains relatively steep, with the 10-year Treasury yielding more than two percentage points above 90-day T-bills.

And while there is always the possibility of a severe external shock that causes an abrupt economic contraction and stock market decline, absent something like that, evidence of a potential U.S. recession on the horizon is lacking. We fully acknowledge that most economic models fail to predict recessions, and we don’t rely on such models or on any short-term GDP forecast as part of our investment process. We’re just noting that the conditions for an imminent recession do seem largely absent.

|

|||

| Source: Robert J. Shiller and Standard & Poor's. Data as of 3/31/2015. | |||

|

|||

| Source: Thomson Reuters. ©2015 BCA Research. |

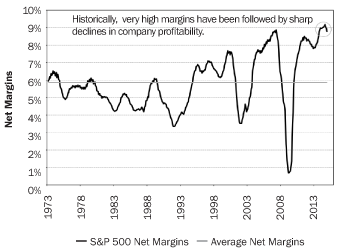

On the other hand, as we’ve discussed before, with corporate profit margins at historically high levels and stock market valuations expensive, the potential for earnings to disappoint the market’s expectations (as reflected in those high valuations) is meaningful. We think that is a likely outcome over our five-year time horizon, and it could happen sooner than later. Counterintuitively, it might even be improved economic growth that is a negative catalyst for stocks to the extent that a strengthening labor market leads to accelerating wage growth, which in turn puts downward pressure on profit margins and earnings.

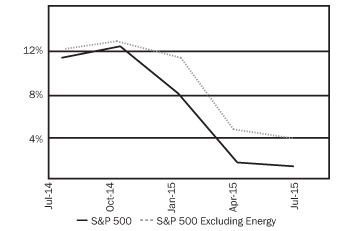

Looking back at what we’ve seen so far this year, S&P 500 profit margins, while still high, have turned down over the past two quarters, as shown in the chart at right. Further, as the chart below shows, S&P 500 earnings growth expectations have been steadily coming down since last year. The strong dollar has been a key driver of that, as an estimated 30%–40% or more of S&P 500 earnings come from non-U.S. sales. (Foreign earnings in weaker currencies are worth less when translated back into dollars. A strong dollar is also a competitive headwind for U.S. companies versus their global peers).

Meanwhile, wage growth is still below levels that Yellen has signaled she wants to see but may be showing early signs of accelerating. Average hourly earnings increased at a 2.3% year-over-year rate in May, the highest increase in five years.

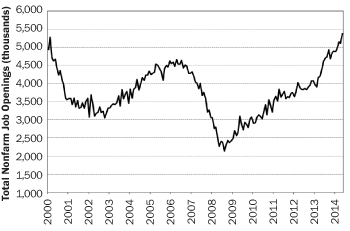

And as the chart below shows, the Employment Cost Index has increased at a 2.6% year-over-year rate. There are also various indicators of labor market strength, such as the Job Openings and Labor Turnover Survey data showing 5.4 million job openings—an all-time high. So we may be moving closer to the point in the cycle where “what’s good for Main Street is not so good for Wall Street,” after many years of the converse (i.e., all the quantitative easing has boosted financial markets and asset prices much more than it has helped the real economy).

Moreover, while we are not worried about inflation at this point, if there is an inflation surprise (e.g., due to unexpectedly strong demand growth) that leads the Fed to raise rates more aggressively than they and the markets currently anticipate, that would undoubtedly be bad for the stock market.

|

|||

| Source: U.S. Bureau of Labor Statistics. Data as of 3/31/2015. | |||

|

|||

| Source: U.S. Bureau of Labor Statistics. Data as of 4/30/2015. |

Ultimately, rising interest rates should become more of a headwind for stocks as (1) bonds become relatively more attractive as a competing investment, (2) higher interest expenses for businesses negatively impact profit margins (after being a positive factor with rates at rock-bottom levels), and (3) equity investors use higher rates to discount corporate earnings implying lower net present business values. But, again, these are forces that could unfold over time and, as such, are factors we consider in our five-year economic scenarios versus trying to brace for them in the very near term.

Concluding Comments

Overall, the point is that we can lay out plausible arguments for why stocks might drop in the short term or, alternatively, why there is no obvious catalyst for them to drop—if there was an “obvious” catalyst then presumably the market would already be accounting for it in current asset prices. But we’d argue this is true at any time in any environment; when it comes to a volatile asset class like stocks, almost any outcome is possible over a short time frame (i.e., how many people predicted the S&P 500 would rise 32% in 2013 or fall 38% in 2008?). So we don’t invest based on short-term forecasts . . . of anything. That’s also why it’s so important to have a long time horizon when owning stocks, because there are inevitably going to be shorter-term (negative) surprises. (Negative surprises shouldn’t be surprising.) And when these surprises occur, investors should be prepared for increased market volatility given that markets often overreact to transitory/shorter-term news or outcomes. In those moments, it’s useful to remember that volatility is the shorter-term discomfort an investor must often experience in order to earn attractive longer-term returns from owning stocks. For it’s exactly those volatile market movements that can create compelling longer-term investment opportunities: tactical asset allocation fat pitches for us, and great stock- and bond-picking opportunities for our managers.

—Litman Gregory Research Team (7/6/15)

© Copyright 2002-, Litman Gregory Analytics, LLC