The Federal Reserve (Fed) is expected to increase its Fed Fund rates during the second half of 2015. Although the timing and extent of the short-term rate increases are not known, we believe that the impact on Real Estate Investment Trusts (REITs) shares could be muted as:

1) Strong fundamentals and use of fixed rate debt may continue to bolster free cash flows and dividends

2) Cap rates (a key denominator to estimate underlying net asset values) may be less sensitive to short-term rate increases than long-term rate trends.

A favorable environment for free cash flows.

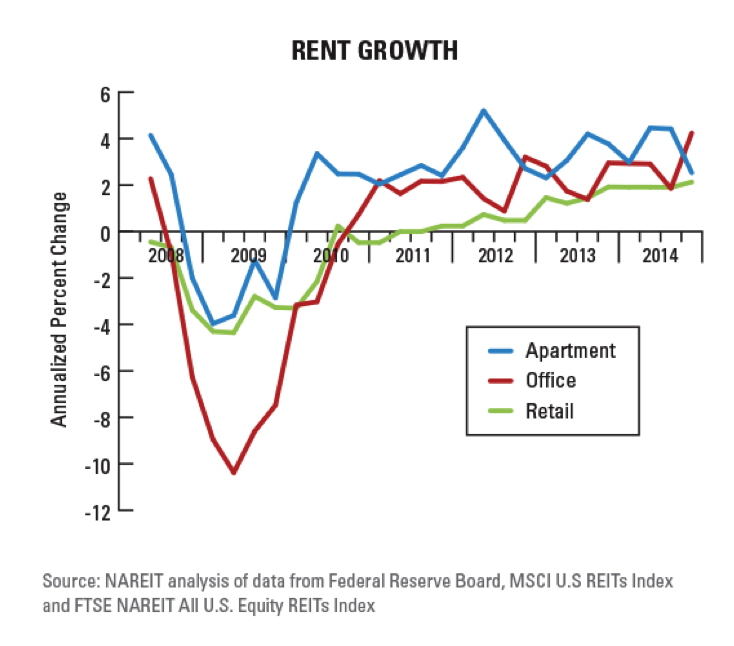

Since 2011, as reflected in the graph, rental growth across all sectors have averaged 2-3% per year as demand has recovered while supply growth has been muted.

We believe that these fundamentals have the potential to stay strong in a rising short-term rate environment: An increase in short-term rates may have a negative impact on the pricing of short-term construction loans and keep supply under control while demand is still expanding. In addition, most REITs are less sensitive to higher short-term rate increases. They took advantage of a booming unsecured debt market in 2010-2015 to issue unsecured bonds and replace LIBOR-based bank loans with long-term, fixed-rate debt. They have also kept construction activity under control and limited the use of short-term, variable-rate construction loans. As a result, the financing costs may not increase and we believe that the REITs’ ability to generate free cash flows and pay dividends should not be impaired by a rise in short-term interest rates.

Cap rates are more sensitive to long-term rate increases.

REIT shares tend to trade close to their Net Asset Values (NAVs). NAV in turn is defined as Net Operating Income/Cap Rate - Liabilities. A cap rate is a key metric to assess the value of a property. A higher cap rate may lead to lower property value. Although cap rates are determined by transactions and market participants, we believe that short-term interest rate increases may not have a sizable impact on them. In fact, private real estate investors use medium/long-term Internal Rates of Returns (IRRs) and assumptions on long-term costs of financing to assess valuation and derive cap rates. As a result, if the Federal Reserve increases short-term rates and long-term rates do not move, cap rates may stay low.

We believe that the sharp decline in REIT shares in Q2’15 (-10%) may constitute a buying opportunity. Investors may have anticipated a negative impact of higher short-term rates on REITs but, as in 2004 when REITs declined sharply in March before rebounding strongly, operational results and property markets may still be very strong.

Boris E. Pialloux, CFA

Disclosures:

The opinions expressed herein are those of Trust & Fiduciary Management Services, Inc. (TFMS) and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. TFMS reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Trust & Fiduciary Management Services, Inc. is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about TFMS including our investment strategies, fees and objectives can be found in our ADV Part 2, which is available upon request. TFMS-15-10