HEIGHTENED VOLATILITY NEW NORMAL FOR GLOBAL MARKETS

In the second half of Q3, higher volatility was the rule rather than the exception as markets wrestled with the implications of a global economy in flux.

EQUITY MARKETS STRUGGLE TO FIND FOOTING AMIDST FUNDAMENTAL SHIFTS IN GLOBAL ECONOMY

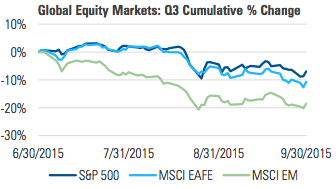

Global equity markets offered few places to hide during the third quarter of 2015. Emerging market equities extended their selloff that began in April, while US and developed market equities joined the fray in August:

Figure 1

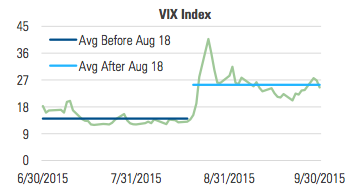

After laying low for much of the summer, volatility reared its head in the middle of August and remained elevated for the rest of the quarter:

Figure 2

MANAGED VOLATILITY PORTFOLIOS

During the latter half of Q3, we estimate that a typical managed volatility growth portfolio saw its hedge fluctuate between 40% and 60%, and exhibited between half and two-thirds of the volatility of its unhedged counterparts. The volatility of volatility touched an all-time high in September, creating one of the more challenging environments for managed volatility portfolios to date.

In a perfect world, a managed volatility portfolio will implement a hedge as volatility rises and remove the hedge as volatility begins to fall. Investors who are comfortable with volatility and don’t use a hedge will always get 100% of the upside and 100% of the downside. The investor who hedges essentially trades some of his upside for a reduction in the exposure to the downside.

One of the reasons a hedge is so appealing is that the extent of the market’s downside is unknowable. There is comfort and sensibility in the limiting of downside exposure, even if it means conceding some of the upside.

These principles can be easy to forget when the market is swinging wildly in both directions. We encourage investors to maintain a long-term view and to stay focused on the value of the hedge and the risk that it seeks to protect against.

MARKET COMMENTARY

CHEAPER OIL’S RIPPLE EFFECT

At the end of September, the price of a barrel of crude oil was $45, less than half its June 2014 price of $95. The implications of such a massive price decline on a commodity so integral to the economy are significant, disparate and far reaching.

In recent years, technology has been a primary driver of oil’s changing supply and demand dynamics. On the one hand, it’s reducing demand by making combustion engines more efficient and by making sources of renewable energy more viable. On the other hand, it’s increasing supply by improving the efficiency of discovery and extraction.

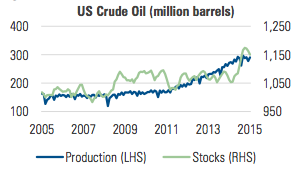

In the US, crude stockpiles have risen as production growth has outpaced growth in demand:

Figure 3

A defining characteristic of these trends is that they are not short-term in nature. Under no apparent threat, they hint at the possibility that the reduction of oil’s value to the global economy may endure.

For consumers, cheaper oil is like a tax cut, but for oil producers it represents a pay cut. The massive geopolitical and economic consequences of persistently cheaper oil will likely be an ongoing source of volatility as markets digest the implications and gain a better understanding of the winners and losers.

In the US, the energy sector has indeed suffered. Its market cap has fallen by nearly 40% and layoffs in the sector have been high. The US economy however, is highly diversified and is capable of enduring such a blow.

The economies of other countries however, especially in emerging markets, are more reliant on the export of oil. With crude oil now yielding half the revenue it did a year ago, many oil-rich EM countries will find it more difficult to service their record high levels of USD-denominated debt.

China’s August intervention in the stock market and devaluation of the yuan were strong signals that the Chinese economy is indeed slowing. As a source of demand for commodities, China does not appear to be a potential catalyst for near term growth.

ARE RATES DRIVING RISK-TAKING OR IS RISK-TAKING DRIVING RATES?

No investor or entrepreneur ever has perfect knowledge of the future, but some environments are naturally more conducive to risk taking than others. In the current environment, low longer-term interest rates imply that investors’ growth expectations are low, and by extension, their appetite for risk.

Through their rate reduction efforts, the world’s central banks have attempted to encourage investment and risk-taking. The reduced cost of borrowing, however, has not resulted in greater optimism, suggesting that a return to stronger growth will require something beyond what monetary policy can offer.

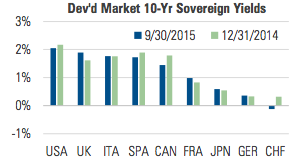

Long-term interest rates around the globe remain in a historically low range. At the end of the quarter, investors were accepting a yield of 0.36% on the 10-year German bund, while just across the border investors were paying for the privilege of lending to the Swiss government. How pessimistic must an investor be to accept a negative yield for 10 years?

Figure 4

In the US, Federal Reserve officials continued to articulate that the time is now appropriate for raising the fed funds rate. Nevertheless, their highly-anticipated September meeting ended with the rate unchanged.

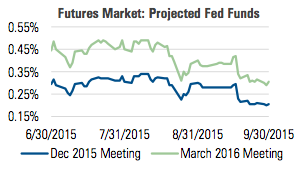

At quarter-end, Bloomberg reported that 84 percent of surveyed economists expected an initial rate increase in December. At the same time, the futures market for fed funds was projecting a different scenario:

Figure 5

The Fed has been explicit about their policy decisions being data dependent and consistent with their dual mandate of maximum employment and price stability.

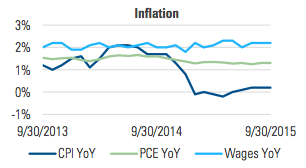

The employment picture has improved markedly, but their two percent inflation target remains elusive and inflation expectations remain low:

Figure 6

By publicly and repeatedly endorsing the idea of a rate hike in the face of almost zero inflation, but then failing to follow through with a move, the Fed contributes to a heightened sense of uncertainty. It also sends an implicit and contradictory message that the economy may not be as strong as they say it is. This in turn reduces investor appetite for risk and contributes to market volatility.

Low commodity prices, waning growth in China, a sputtering global economy and a strong US dollar are all keeping a lid on prices. With that in mind, it’s difficult to see how a December rate hike could be based on legitimate and genuine concerns about inflation.

Given these and other ongoing conditions, we expect volatility to remain elevated through the end of the year and into next.

While shifts in the global economy contribute to volatility, they are also a manifestation of what Joseph Schumpeter called “creative destruction.” We believe investors should maintain exposure to the market, being ready to benefit from the opportunities that arise as the old replaces the new; but they should do so in a way that recognizes the risks and actively seeks to mitigate them.

Unless otherwise noted, all data is sourced from Bloomberg. Email subscribe@[email protected] to receive Milliman’s commentary.

Milliman Financial Risk Management LLC is a global leader in financial risk management to the retirement savings industry. Milliman FRM provides investment advisory, hedging, and consulting services on $193 billion in global assets (as of July 1, 2015).

Established in 1998, the practice includes over 130 professionals operating from three trading platforms around the world (Chicago, London, and Sydney). Milliman FRM is a subsidiary of Milliman, Inc.

Milliman, Inc. (Milliman) is one of the world’s largest independent actuarial and consulting firms. Founded in Seattle in 1947, Milliman has 55 offices in key locations worldwide that are home to over 2,600 professionals, including more than 1,300 qualified consultants and actuaries.

INVESTMENT PROFESSIONAL USE ONLY

Recipients must make FOR their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

Any discussion of risks contained herein with respect to any product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved

© Milliman Financial Risk Management