|

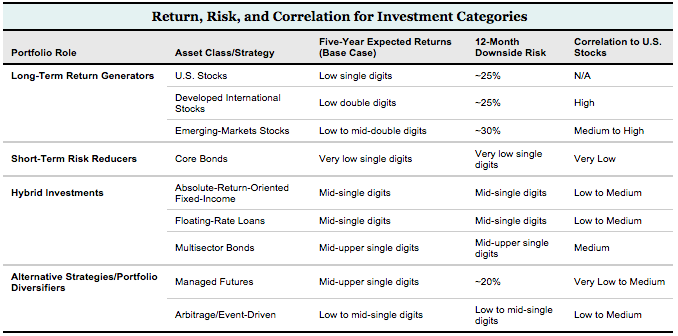

We often write about how our tactical asset allocation investment process seeks to use shorter-term market price volatility to our long-term advantage. Of course, while it is easy enough to say volatility creates opportunity, the reality is that volatility can be stressful and painful when you are actually experiencing it in your portfolio. We currently construct client portfolios utilizing four different categories of investments, each playing a specific role: longer-term return generators, shorter-term risk reducers, hybrid investments (which have elements of both return generators and risk reducers), and diversifying alternative strategies. Careful consideration of the return, risk, and correlation of each component helps us meet our goal of building portfolios that are unlikely to exceed their 12-month downside loss thresholds, which vary depending on a client’s risk tolerance. We think it is instructive to outline how we define and employ these various types of investments. LONGER-TERM RETURN GENERATORS We’ll start with the longer-term return generators. These are investments or asset classes that we own because of their ability to generate longer-term growth of capital, well in excess of inflation. U.S., developed international, and emerging-markets stocks are our portfolios’ primary long-term return generators. The key words here are longer term. We expect these investments to have higher shorter-term volatility and significant downside risk (potential losses); this comes with the territory when owning stocks and other investments that offer higher return potential. As we invest in more volatile but higher-returning asset classes and strategies, we are also increasing the portfolio’s downside risk exposure, at least over the shorter-term. Therefore, we are always weighing and balancing an investment’s potential contribution to our portfolios’ short-term downside risk against our assessment of its longer-term return prospects. Unfortunately, there is usually no free lunch in this regard: asset classes and strategies that have higher long-term expected returns typically come with more volatility and short-term risk. It is therefore critical that a stock investor has the ability to withstand meaningful market volatility and shorter-term losses in the pursuit of superior longer-term investment returns. This is precisely why our more conservative risk-averse portfolios have lower allocations to stocks, and we also make an effort to moderate the risks of specific types of stocks by diversifying our holdings across all of our portfolios.

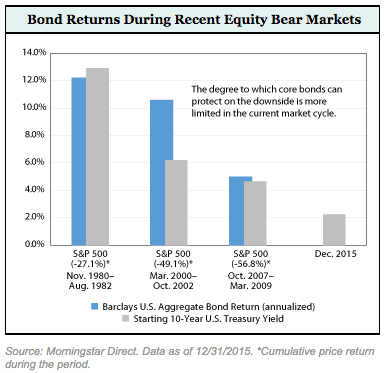

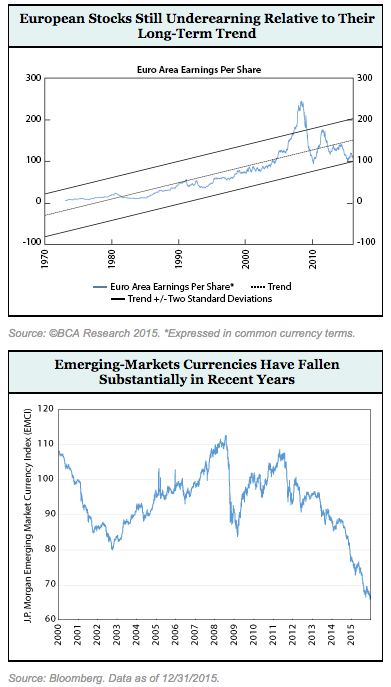

Our investment thesis for European and emerging-markets stocks has not changed materially since we initiated the positions earlier this year. In a nutshell, our analysis suggests both markets are undervalued (current prices are depressed) relative to their normalized earnings potential looking out five or so years. Therefore, we expect to benefit from both stronger-than-expected earnings growth and some valuation (P/E multiple) expansion, generating the double-digit type of expected returns noted above. When investing in non-U.S. assets, currency effects can be a shorter-term wild card (and we have hedged half of our European stock position in an effort to neutralize the currency translation impact). But on a fundamental, longer-term basis, the euro and emerging-markets currencies appear more likely to be undervalued versus the dollar than overvalued (i.e., currency movements may be a tailwind to dollar-based returns going forward after having been a drag on returns the past few years). Yet, we are also very cognizant of the risks and weigh these alongside the attractive return potential we see. Consequently, we have been cautious in establishing our tactical positions, and we have a high hurdle before we will add to them. Given the ongoing volatility in emerging markets in particular, this has been a wise approach. Ultimately, we expect our clients to be rewarded by these holdings, but we also want our clients to be cognizant of (and prepared for) potentially more downside, despite already having suffered through a big emerging-markets drop. There are of course other much more positive or benign shorter-term scenarios and, again, we own these asset classes based on our assessment of their strong long-term return potential. To take one example of a positive short-term scenario that is plausible, Capital Economics Group forecasts a 20% gain for emerging-markets stocks (in dollar terms) in 2016, driven by receding fears about China’s economy and an end to the slump in commodity prices (see Capital Economics’ “10 Key Calls for 2016”). We’d certainly welcome that outcome, but we were not betting on it (nor on any 12-month outlook) when we established our tactical positions. We are confident we will get paid (with outsize returns) for our current allocations to European and emerging-markets stocks. But we also know that we don’t know precisely when those markets will turn around. As the old saying goes, “They don’t ring a bell at the bottom of the market” (or the top for that matter). It requires patience—another core element of our investment process—to hold onto (and potentially add more to) these long-term return generators during the periods when they seem only to be downside-risk generators. Conversely, when it comes to U.S. stocks, which have been the star performer over the past five-plus years, our tactical outlook over the coming five years is much less positive compared to emerging-markets stocks and European stocks. Unlike in those markets, our analysis suggests U.S. valuations are high. And with U.S. corporate profit margins also above normal, we see potential for disappointing earnings growth and valuation multiple contraction. (As noted earlier, earnings growth has disappointed recently, but multiples have risen.) Our base case scenario results in low single digit expected returns for the S&P 500. While that return may exceed what we earn from low-risk core bonds (to be discussed next), we find it insufficient to fully compensate us for the volatility and downside risks as equity owners. It is well below the upper-single-digit-type returns we are looking for, at a minimum, from our long-term return generators. Therefore, we are tactically underallocated to U.S. stocks in our portfolios. Again, our position here is not based on a short-term view of the market, or a prediction that a drop in U.S. stocks is imminent, or even that U.S. stocks will necessarily trail non-U.S. stocks in 2016 (although it is very tempting to say they are due!). Financial market history is a history of cycles (or like the swings of a pendulum), moving from one extreme to another. Market history teaches us that undervalued assets can get even cheaper (fall further), and overvalued markets can overshoot even further on the upside. That is simply the reality that comes with being a long-term equity investor. Valuation is a very poor short-term market indicator. But over the longer term and over full market cycles (five to 10-plus years), valuation is a powerful driver of returns. Buying undervalued assets pays off over time, but you need to withstand the discomfort that typically accompanies it as you wait for markets to turn in your favor. SHORTER-TERM RISK REDUCERS  To mitigate the shorter-term uncertainty, volatility, and downside risk that comes from owning stocks, our balanced portfolios also have dedicated exposure to core investment-grade bonds. If there is a recession or economic shock that leads to increased risk aversion among investors, core bonds have historically performed well in absolute terms (generating solid gains) and very well relative to riskier assets like stocks that may be down 20%–30% or more. We’d expect a similar performance pattern this time around if and when stocks fall into a bear market. So core bonds have a very important risk-management role, particularly in our more conservative portfolios, where our 12-month downside risk thresholds are lower. However, given the very low current yield on core bonds, their potential return is lower than in previous periods when the yield was much higher, while the short-term downside risk for equities remains as high as it has ever been. (For example, we assume 12-month declines of 25%–30% for global stocks in our “severe stress test” scenario.) So even though core bonds may still mitigate some of the shorter-term downside risk from stocks in our portfolios, the degree to which they can do so is more limited in the current market cycle. This past year was a good example of this, with core bonds barely positive while global stocks were negative. Moreover, looking out over our tactical five-year time horizon, expected returns for core bonds are very low, in the 0%–2% range. That is a high price to pay (in terms of low longer-term returns) for the risk-reduction benefits of core bonds, even as valuable as those benefits are for more conservative investors and in managing our balanced portfolios to their 12-month downside loss thresholds. So we are in a situation where our two primary asset classes, U.S. stocks and U.S. core bonds, look unattractive relative to their respective return-generation and risk-reduction roles in our portfolios. This has been the case for the past several years and led us to research and invest in other asset classes and strategies that we think are more compelling on a risk-return basis. These other funds play a “hybrid” role in the portfolios, somewhere between stocks and core bonds. We have also invested in select alternative strategies, including managed futures in 2015, which are quite different from traditional stock and bond funds. We discuss these two other categories next. HYBRID INVESTMENTS: PART RISK REDUCTION, PART RETURN GENERATION As the primary examples of what we consider hybrid investments, we have allocated a meaningful portion of our portfolios to a diversified group of fixed-income funds representing a variety of investment categories. (This group encompasses our multisector, absolute-return-oriented, and unconstrained bond funds: Loomis Sayles Bond, Guggenheim Macro Opportunities, and Osterweis Strategic Income). We are also invested in floating-rate loan funds. We believe these investments have the potential to generate returns over the next five years that are several percentage points above the core bond index and in line with or better than our base case return expectations for U.S. stocks. Importantly, these funds should have much less volatility and downside risk than stocks. However, in most scenarios, these funds will have higher volatility and short-term downside risk than core bonds, due to their credit exposure (e.g., below-investment-grade) and, in some cases, non-dollar currency exposure. While we’ve generally had positive return contributions from these types of funds over our holding periods, in 2015, we experienced more of the risk than the return from our flexible, absolute-return-oriented, and unconstrained bond fund positions. They underperformed core bonds, typically generating small losses (though Loomis Sayles Bond, a fund that offers higher return potential but has a higher risk profile, was down 7% for the year). This is within the range of our downside expectations for these funds, given their flexible mandates and exposures, and is also consistent with the hybrid risk-management/return-generation role they play in our portfolios. Floating-rate loans did a bit better last year—they were down slightly—but still well below our five-year expected return of 6%–7%. ALTERNATIVE STRATEGIES/PORTFOLIO DIVERSIFIERS The final piece of our portfolio is allocated to alternative strategies. These investments also play a dual role of return generator and portfolio risk diversifier. (These investments are considered “alternative” because they should have different return drivers and risk exposures than traditional stock and bond funds.) Within our alternative strategies allocation we own two types of strategies: arbitrage/event-driven strategies and managed futures strategies. Our risk and return expectations are quite different for the two, but broadly speaking we believe these investments will both add valuable diversification benefits (i.e., they will perform differently from the rest of our portfolio holdings) and will also be additive to our balanced portfolio returns over the next five years. Our risk and return expectations for the arbitrage funds are roughly similar to our expectations for the hybrid funds discussed above: better returns than core bonds over the long term but with somewhat higher risk, and comparable returns to U.S. stocks over our five-year tactical horizon but with much less risk. However, the arbitrage funds have lagged core bonds (and stocks) over the past few years. While we have confidence in the managers we’ve selected, we continue to scrutinize these funds as well as conduct research on other alternative strategies and funds. In a nutshell, we expect managed futures’ performance pattern to be very different over time from the other pieces of our portfolio (i.e., they should have very low or no correlation to stock and bond markets and will therefore be a powerful long-term portfolio diversifier and overall risk reducer). We also expect the managed futures funds we own to generate attractive long-term returns relative to their volatility as well as compared to a comparable mix of stocks and bonds. Our ownership period for managed futures has been extremely short, but so far their performance is consistent with our expectations. PUTTING IT ALL TOGETHER In putting these four pieces together, as always, we are guided first and foremost by each portfolio’s (or client’s) risk threshold. This constrains the amount of higher-risk return generators we will own in our more conservative portfolios. And on the other side of the risk tolerance spectrum, it means we have less need to include short-term risk reducers and give up potentially higher long-term returns in our more aggressive portfolios. From that strategic starting point, we then weigh our estimates of each investment’s five-year-forward returns against nearer-term risks, across a range of scenarios and stress tests we think are reasonable. Based on this, we may make tactical adjustments to the portfolio’s strategic allocation.  Overall, our balanced portfolios are

As positioned, we believe our portfolios could generate solid returns over our five-year horizon. Despite our lower U.S. stock allocation, the portfolios are not without risk, which stems from our larger foreign stock positions as well as our hybrid and alternatives investments. In the event of a global stock market selloff, we will experience short-term pain. But extending our time horizon beyond the short term (which by definition is what one needs to do as an investor rather than a speculator), we believe we are being well compensated for the risks we are taking in those areas. —Litman Gregory Research Team © Copyright 2002-, Litman Gregory Analytics, LLC |

Over the last few years, we’ve experienced more of the negative effects of risk assets with our investments in non-U.S. stocks, emerging-markets stocks in particular. But with prospective returns in the low double digits in our base case five-year scenario for European stocks, and comparable or higher return estimates for emerging-markets stocks, we believe we are being well compensated for their risk and that exposure to these markets will pay off over time. Hence our decision to modestly increase our allocations to both in 2015.

Over the last few years, we’ve experienced more of the negative effects of risk assets with our investments in non-U.S. stocks, emerging-markets stocks in particular. But with prospective returns in the low double digits in our base case five-year scenario for European stocks, and comparable or higher return estimates for emerging-markets stocks, we believe we are being well compensated for their risk and that exposure to these markets will pay off over time. Hence our decision to modestly increase our allocations to both in 2015.