We have written a number of articles over the years detailing our research into alternative strategies funds and, more broadly, the long-term role of alternatives in a balanced portfolio. This latest piece highlights the important, diversifying role alternatives could play over the next few years, as we continue to find ourselves in an environment with low expected returns from core asset classes such as investment-grade bonds and U.S. stocks.

If there is a recession or economic shock that leads to increased risk aversion among investors, core bonds have historically performed well in absolute terms (generating solid gains) and very well relative to riskier assets like stocks that may be down 20%–30% or more. We’d expect a similar performance pattern this time around if and when stocks fall into a bear market. So core bonds have a very important risk-management role, particularly in our more conservative portfolios, where our 12-month downside risk thresholds are lower.

|

|||

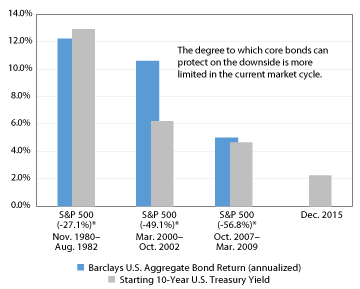

| Source: Morningstar Direct. Data as of 12/31/2015. *Cumulative price return during the period. |

However, given the very low current yield on core bonds, their potential return is lower than in previous periods when the yield was much higher, while the short-term downside risk for equities remains as high as it has ever been. (For example, we assume 12-month declines of 25%–30% for global stocks in our “severe stress test” scenario.) So even though core bonds may still mitigate some of the shorter-term downside risk from stocks in our portfolios, the degree to which they can do so is more limited in the current market cycle. This past year was a good example of this, with core bonds barely positive while global stocks were negative.

Moreover, looking out over our tactical five-year time horizon, expected returns for core bonds are very low, in the 0%–2% range. That is a high price to pay (in terms of low longer-term returns) for the risk-reduction benefits of core bonds, even as valuable as those benefits are for more conservative investors and in managing our balanced portfolios to their 12-month downside loss thresholds.

Compounding the problem, even our base case scenario for U.S. stocks results in low single-digit expected returns for the S&P 500. While that return may exceed what we may earn from low-risk core bonds, we find it insufficient to fully compensate us for the volatility and downside risks as equity owners. It is well below the upper-single-digit-type returns we are looking for, at a minimum, from our equity investments.

So we are in a situation where our two primary asset classes, U.S. stocks and U.S. core bonds, look unattractive relative to their respective return-generation and risk-reduction roles in our portfolios. This has been the case for the past several years and is what initially led us to research and invest in alternative strategies that we think are more compelling on a risk/return basis. Currently, we own two types of strategies: arbitrage/event-driven strategies and managed futures strategies.

Arbitrage and Event-Driven Strategies

Arbitrage, and event-driven investing strategies more generally, fits well in a mutual fund context. Event-driven investing attempts to profit from exploiting price inefficiencies resulting from some corporate action that the manager believes will be transformative to a company and is not currently reflected in the market(s) for the security. Events can include mergers, acquisitions, spin-offs, refinancings, litigation, etc.

The current environment for arbitrage and event-driven investing has been largely unfavorable, with a number of high profile deals failing to go through and low interest rates impacting returns. However, we expect the arbitrage funds we invest in to provide better returns than core bonds over the long term but with somewhat higher risk, and comparable returns to U.S. stocks over our five-year tactical horizon but with much less risk.

Managed Futures Strategies

Managed futures is a systematic alternative investment approach that seeks to take advantage of price trends across a wide range of global futures markets. (A futures contract is a standardized agreement between two parties to buy and sell an asset for a certain price at a date in the future.) These trends exist due to the behavior of market participants, are often extended through the under- and over-reaction to changes in fundamentals, and may be exaggerated further by anchoring and/or herding behavioral biases. Therefore, we expect the existence of trends to persist, and not be arbitraged away. Strategies include the use of stock index, interest rate, currency, energy, and commodity futures. These funds generally buy futures contracts for assets that have been rising and sell contracts for assets that have been falling.

We expect managed futures’ performance pattern to be very different over time from the other pieces of our portfolio (i.e., they should have very low or no correlation to stock and bond markets and will therefore be a powerful long-term portfolio diversifier and overall risk reducer), and therefore should be complementary. Historically, they have provided return ballast during severe equity market declines. We also expect the managed futures funds we own to generate attractive long-term returns relative to their volatility as well as compared to a mix of stocks and bonds. We view managed futures as a long-term position that should improve our portfolios’ risk-adjusted returns across a wide range of potential scenarios.

Continuing Research

Returns from the current lineup of alternative strategies funds we’ve invested in have so far been consistent with our expectations. Nevertheless, we continue to cast a pretty wide net in the alternatives space, looking for funds with the potential to add return and/or reduce risk in our client portfolios, across a variety of different strategies. Given our aforementioned negative view on expected returns of traditional asset classes, we believe the potential diversification benefits of alternative strategies are extremely attractive.

|

© Copyright 2002-, Litman Gregory Analytics, LLC |