Alternative Investments: Incorporating a Turnkey Solution

Executive Summary

Alternative investments have been gaining wide acceptance in many investors’ portfolios as a way to provide diversification. In a recent alternative investment survey of U.S. institutions and financial advisors, Morningstar and Barron’s found that professional buyers had “continued enthusiasm” for many varieties of alternative strategies, which suggests that “demand may strengthen in the future.”1

While interest in alternatives remains strong, incorporating these strategies into portfolios introduces two primary challenges: 1) understanding the complexity of these strategies and 2) determining the appropriate allocation of alternatives in a diversified portfolio.

In this white paper, we discuss the complexities of alternative investments and how turnkey solutions can provide increased flexibility and access to numerous alternative investment strategies.

Alternative Investments’ Role in Asset Allocation

Increasingly, many investors, and the advisors who serve them, appreciate the benefits of alternative investments in a diversified portfolio. Liquid alternatives—alternative investments in a mutual fund format—seek to deliver returns using complex strategies while providing daily pricing, increased liquidity and more portfolio transparency.

Modern Portfolio Theory

Given their non-traditional approach and their ability to invest in areas and in ways traditional investments cannot, alternative investments have the potential to provide increased diversification—and as a result, an improved risk/reward profile—in an overall portfolio.

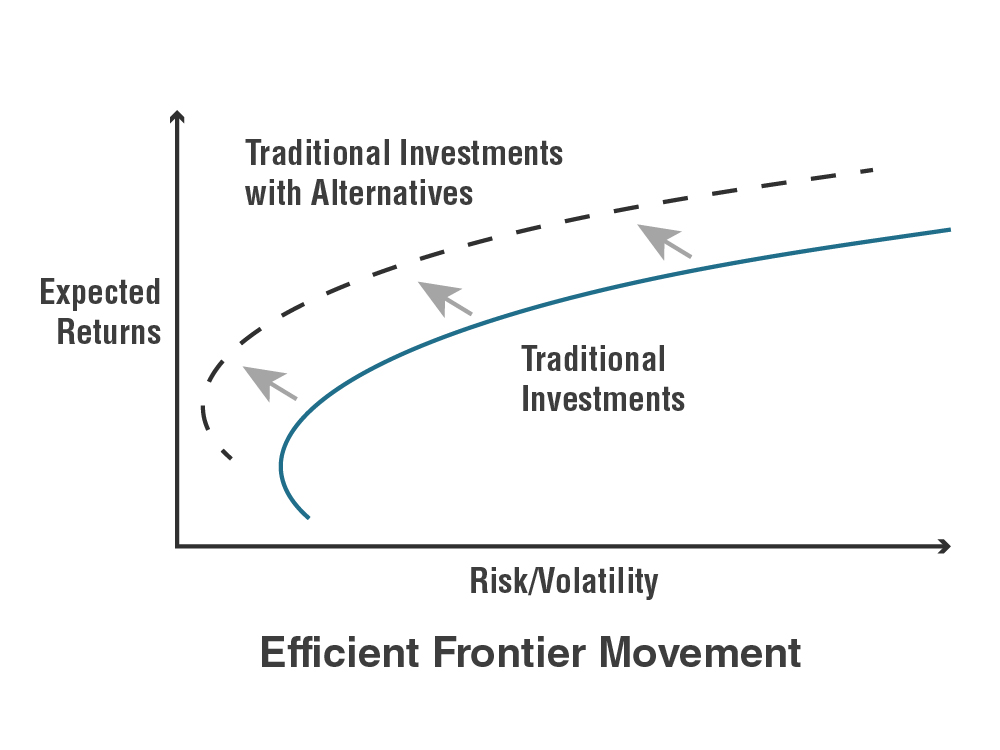

Nobel Prize winning Economist Harry Markowitz is renowned for his research on the Modern Portfolio Theory and created the theory of the Markowitz Efficient Frontier. As shown in Graph 1, the solid line represents the efficient frontier along which portfolios of varying percentage mixes of traditional investments such as stocks and bonds fall. Each point along that solid line indicates the highest expected return for every level of risk. Any traditional portfolio of stocks and bonds that falls below the curved solid line is considered inefficient and offers either more risk for each level of return or more return with higher risk.

When alternative investments were added to a traditional stock and bond portfolio, the curved line moved up and to the left. The curved dashed line shows how expected risk decreases while expected returns increase.

Graph 1: Expected Risk vs. Expected Returns

The efficient frontier illustrates the primary reason for incorporating alternative investments in an overall portfolio: Alternative investments have historically improved the return while decreasing the risk, i.e., have successfully made the portfolio more “efficient.”

However, many investors mistakenly assume all alternative investments are designed as alpha generators. Rather, many alternatives attempt to perform differently from the stock and bond market, which provides the opportunity to outperform in down periods. This outperformance during an overall stock market decline can result in potentially smoother returns over time. These smoother results may act to increase returns while reducing risk in an overall portfolio.

Low to Negative Correlation to Stocks and Bonds

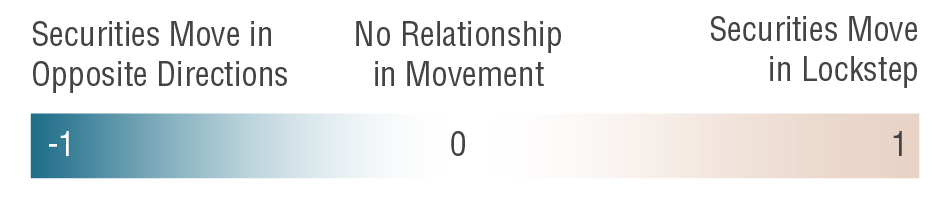

Correlation is one way to measure the degree to which different investments move in relation to each other. A perfect correlation—a security moves in lockstep with another in either an up or down direction—is exactly 1. A perfect negative correlation of -1 implies that two securities move in opposite directions. A correlation of zero means there is no relationship in the movement at all.

The lower the number, the less correlated two investments are to each other. Importantly, the lower the number, the more likely the return and risk characteristics will differ, resulting in higher diversification within the overall portfolio.

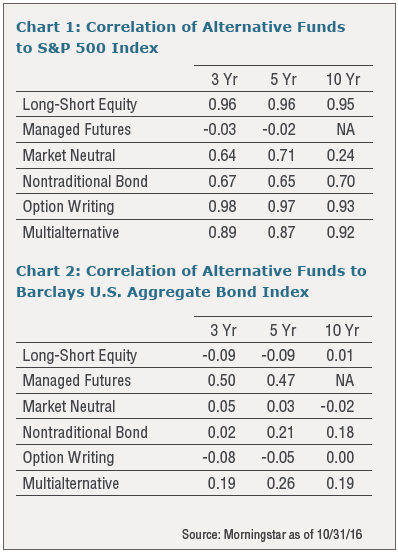

Alternative investment strategies that span multiple asset classes tend to have different up and down movements from the broader equity and fixed income markets. As shown in Chart 1 and Chart 2, over the past three, five and 10 years, funds in different Morningstar Alternative categories have had different correlation—generally low to negative—to the broader equity and fixed income markets.

Graph 2: Correlation Range

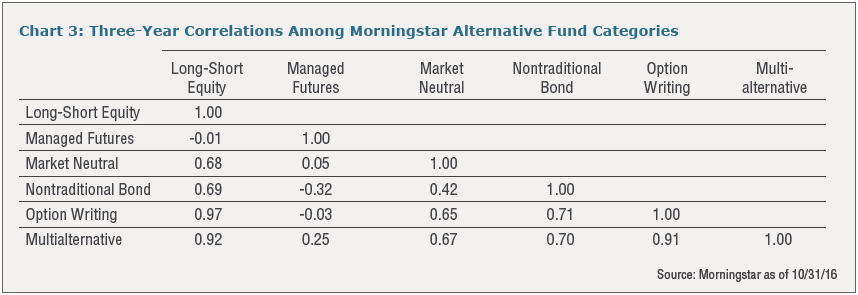

Additionally, different alternative investment strategies have experienced varying correlations to each other. In fact, according to Morningstar data, many strategies have a negative correlation to each other, as shown in Chart 3.

Alternative Investment Allocation in a Portfolio

How much of an overall portfolio should be allocated to alternative investments? Studies suggest asset allocation percentages should be higher than many assume.

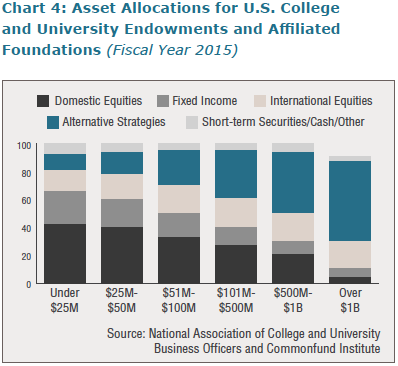

On one end of the allocation spectrum are large endowments and pension funds that have a significantly higher allocations to multiple alternative strategies. According to the National Association of College and University Business Officers and Commonfund Institute, in fiscal year 2015, endowments and foundations of over $1 billion had a 57% allocation to alternative strategies. Smaller endowments that managed less than $100 million held a much smaller allocation to alternative strategies, ranging from 11 to 25%.2

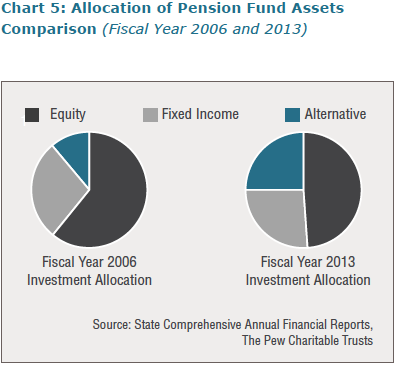

Pension funds have also diversified away from stocks and bonds with the goal of creating a more efficient portfolio. In fiscal year 2013, state pension funds, on average, had a 25% allocation to alternative investments. This figure is more than double the percentage only seven years ago, when it was 11%.3

While endowments and pension funds are managing millions—or in some cases, billions—it is unlikely the individual investor saving for retirement would hold a high allocation in alternative investments. However, allocations have been steadily climbing for individuals as well. According to the survey by Morningstar and Barron's, advisors have allocated between 6% and 20% to alternative investments on average, but “over the past few years more advisors have been increasing their alternative allocations to the 11% to 15% range.”4

While allocations need to be a separate consideration for each investor depending on individual investment goals, financial situation and risk profile, research has found that a small allocation of around 5% may have nearly no effect on the risk/return profile of a portfolio. Rather, alternative investments have the most desired effect when the allocation is more meaningful.

Importantly, due to alternative investments' defensive stance and lower correlation to the overall markets, they may be appropriate for investors nearing retirement who want to narrow their variation in returns. Historically, in a significant market decline, alternatives have helped cushion the fall.

Whereas many investors assume alternatives are turbo-charged performance enhancers, the majority of these investments are likely appropriate for risk-averse investors.

Benefits of a Fund of Funds Approach

Unlike traditional stock and bond investments, alternative investment products vary significantly in investment strategies. Since 2008, total assets in liquid alternative investments, which are alternative investments in a mutual fund format, have increased nearly 380% to $178 billion, with the number of funds growing by almost 185% to 484.5

With hundreds of funds from which to select, the process of researching, analyzing and selecting the appropriate alternative investments can be time consuming and cumbersome. In addition, due to the complexity of these funds, the due diligence process needs to be highly specialized.

In a fund of mutual funds format, the complexity is removed, as alternative investment managers have been researched, screened and selected in this integrated solution. The turnkey solution that results can yield the following benefits:

- Access to Numerous Strategies. The portfolio provides access to a wide-range of alternative strategies hand-selected across all subcategories.

- Professional Management and Due Diligence. A fund of funds is managed by an experienced investment team with the resources, expertise and knowledge to employ quantitative and qualitative factors when selecting experienced management teams with established track records.

- Additional Liquidity. Generally, a direct investment in an alternative strategy could have less liquidity than a mutual fund. By purchasing these strategies through a fund of funds, investors have an additional layer of liquidity and transparency.

ABOUT THE AUTHOR

Brad H. Alford, CFA Chief Investment Officer

Alpha Capital Management

Brad Alford is the portfolio manager of the Value Line Defensive Strategies Fund. He has over twenty-five years of investment management experience. Previous positions include Managing Director at Atlantic Trust; Director of Investment Advisory Services at MyCFO; Managing Director of the investment division for the $2 billion Duke Endowment, where he expanded its alternative asset portfolio from $100 million to more than $1 billion; and Director of Endowment Investments for the Emory University Endowment with assets in excess of $4 billion.

Mr. Alford holds a BS in Corporate Finance and an MBA from the University of Alabama. In addition, he completed the Senior Investment Manager Program at Princeton University and holds the Chartered Financial Analyst (CFA) designation.

1 “2014-2015 Alternative Investment Survey of U.S. Institutions and Financial Advisors,” Morningstar and Barron’s, July 2015.

2 "Asset Allocations for U.S. College and University Endowments and Affiliated Foundations, Fiscal Year 2015." National Association of College and University Business Officers and Commonfund Institute, 2016.

3 "Making State Pension Investments More Transparent." The Pew Charitable Trusts, February 2016.

4 “2014-2015 Alternative Investment Survey of U.S. Institutions and Financial Advisors,” Morningstar and Barron’s, July 2015.

5 Benjamin, Jeff. "Morningstar to create new style box for liquid alt funds." InvestmentNews, October 20, 2016.

You should carefully consider investment objectives, risks, charges and expenses of Value Line Mutual Funds before investing. This and other information can be found in the fund’s prospectus and summary prospectus, which can be obtained free of charge from your investment representative, by calling 800.243.2729, or by clicking on the applicable fund at www.vlfunds.com. Please read it carefully before you invest or send money.

The S&P 500 Index consists of 500 stocks traded on the New York Stock Exchange, American Stock Exchange and the NASDAQ National Market System and is representative of the broad stock market. This is an unmanaged index and does not reflect charges, expenses or taxes. The Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS. This is an unmanaged index and does not reflect charges, expenses or taxes, which are deducted from the Fund’s return. It is not possible to directly invest in an index.