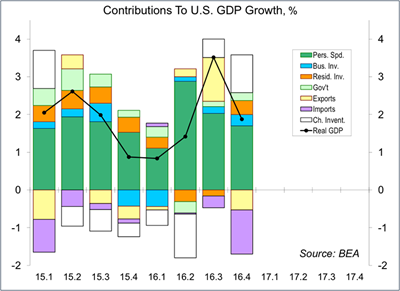

Real GDP rose at a 1.9% annual rate in the initial estimate for 4Q16, with the headline growth figure held down by a wider trade deficit. That does not mean that foreign trade is a drag on the U.S. economy. President Trump has inherited an economy that is in good shape. However, the federal budget situation, manageable right now, is set to become more troublesome in the years ahead – and that is before tax cuts and any additional spending on defense and infrastructure.

Inventories and foreign trade account for more than their fair share of volatility in quarterly GDP figures. Private Domestic Final Purchases (PDFP), which exclude net exports and the change in inventories, is the best measure of underlying domestic demand. PDFP rose at a 2.8% annual rate in the advance estimate for 4Q16 (+2.4% y/y). Inventory growth picked up further, adding a full percentage point to headline GDP growth. Net exports subtracted 1.7 percentage points. Soybean exports (mostly going to Mexico and China) surged in 3Q16 and only partly unwound in 4Q16. Imports, which have a negative sign in the GDP calculation, rose at an 8.3% annual rate, subtracting 1.2 percentage points from GDP growth. That is a sign of strength in the domestic economy, not weakness.

Much has happened since the new administration has hit the ground. Rather than prioritizing the many things they want to accomplish, they will try to do everything at once. This leaves Washington observers struggling to keep up. There is a lot of confusion about how it all works. While some have teeth, most of the recently issued executive orders are merely guidelines for what President Trump wants Congress to do (for example, Congress has to allocate spending to build the wall).

As many have noted, a misstep on foreign trade remains one of the biggest potential risks for the new administration. Trump was expected to moderate his rhetoric once in office and the business leaders surrounding him were expected to educate him on the importance of trade to the U.S. and global economies. To the horror of trade experts, none of that is happening. Seventy years of global economic progress appears poised to be turned on its head in just under a week.

Trump shares many of the public’s misconceptions on trade. It is not a zero-sum game. While there are winners and losers with global trade, the U.S. and its partners are better off overall. When NAFTA was proposed, supporters and opponents squared off on the implications for jobs, debating whether it would add or subtract jobs. Most economists would say neither. Employment would likely be little changed. It’s the type of jobs that would differ. Shed the low-end stuff and replace it with higher-end jobs. We have struggled with the replacement part, to be sure, but half of the manufacturing jobs lost over the last 15 years have been due to technology improvements.

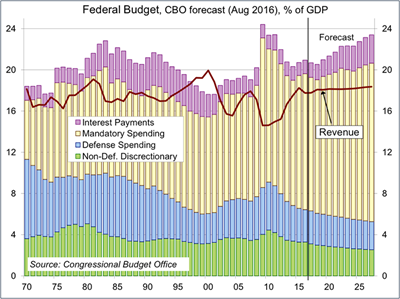

The Congressional Budget Office released revised projections last week. Based on current law, the federal budget deficit is set to hit $1 trillion in just six years, reflecting increased spending on entitlements and interest payments. Note that if we leave entitlements and defense spending unchanged (you can’t do anything about interest payments), you could cut everything else to zero and still have a deficit. If you want to cut taxes and boost defense spending, the deficit will rise more rapidly.

When the federal budget deficit hit $1.4 trillion (10% of GDP) in FY09, we noted that the increase was due to the severity of the recession. The budget deficit was really a long-term problem, and that’s still the case, but strains getting are closer.

A showdown with China seems inevitable, but the Trump administration has chosen to go after Mexico first. Mexico is seen as a weak negotiator and will serve as an example to follow (this is what we are told). Yet, U.S. consumers and businesses will end up paying the bulk of any increase in tariffs.

© Raymond James

© Raymond James

Read more commentaries by Raymond James