Executive summary

• The traditional roles of fixed income and equities no longer apply: Many investors look to the equities markets for bond-like yields, and some fixed income securities have produced returns that equity investors would envy.

• The hunt for yield has intensified, driving some investors to stampede beyond equities and into various markets, and spawning a “bondification” of growth asset types.

• Drivers for the search for yield are societal forces—changes in demographics—and don’t appear to be going away anytime soon.

• As a result of these secular changes, not only speculators are chasing yield; investors of all stripes are assuming and rationalizing risks.

• Amid this backdrop, active management and diversification can play a bigger role than ever for fixed income investors, with solutions blending asset types, geographies, currencies, and durations a sign of the new times.

The inability to generate meaningful income from interest-bearing investments has become a defining characteristic of an investing generation. It’s one thing that the European Central Bank (ECB) and Bank of Japan (BoJ) recently have doubled down on their unorthodox policies of negative interest rates, where commercial banks pay a fee to hold reserves and investors lock in a small loss when holding debt to maturity. But the negative yield phenomenon — once generally unthinkable and confounding to economists — has spread. Some corporate bond issuers have tested negative-yielding debt last year, and 14 countries including Japan and many in Europe offered negative-rate debt as of June 2016. (Source: The Organization for Economic Cooperation and Development (OECD).)

We live in a low and often negative-yielding interest rate world – one that can look self-sustaining. As The Economist recently put it, the promise of continual central bank action makes the linkage of borrowing and interest rates an almost quaint notion.

How did we get to such a strange place, and what are professional investors to expect from fixed income when looking at the long term? In this paper, we’ll touch on negative interest rates as a societal issue and a financial one, discuss what it means for fixed income as an asset class, and remind you that there’s always a way forward.

Unorthodox monetary policies, low and negative rates, and more have led to the hunt for yield, bringing investors further and further out on the risk spectrum. How did we get here? More importantly, where do we go from here?

An environment that has driven the chase for yield

A portfolio role reversal

For years, the principles of bond investing were used to provide steady and predictable income, with coupons cushioning price volatility. By contrast, stocks were typically used by investors looking for growth and willing to assume more risk, occasionally having dividends amplifying returns.

Today, with ultralow short-term interest rates—rates that have even gone negative in a number of economies—the traditional investing roles don’t seem to apply. More investors are tending to look to bonds for potential appreciation and to equities for income. For example, global bonds in 2016 were generating some of their strongest performance since 2009, with the Bloomberg Barclays Global Aggregate Index returning 6.8% through Oct. 31, 2016, even after suffering a 2.8% loss in an October rout. However, two weeks later, after the surprise of the U.S. presidential election, this index was down to 3.95% for the year (as of Nov. 15, 2016).

Generally, the bond return has not been coming primarily from yield or the income component—yields have been the big casualty of the low interest-rate environment. In fact, in examining the returns of long-dated government bonds in June 2016, The Wall Street Journal estimated that 90% of the return on those government bonds was attributable to capital gains, while more than half the return for high yield bonds during the same period came down to coupon payments. Ordinarily, it would be the other way around, with investors looking to high yield for more capital appreciation because high yield as an asset class is considered closer to equities.

Meanwhile, investors have flocked to certain equities for the bond-like qualities of steady payments—particularly those known for their dividends. These dividendpaying equities tend to have lower volatility, may hold up better than other types of stocks in a market selloff, and as their nomenclature implies, typically provide income quarterly. In the first part of 2016, investor inflows into real estate investment trusts (REITs), telecommunications, and utilities—some sectors that can have dividend-yielding stocks—helped those sectors gain more than 10%. One major fund company was forced to close its biggest dividend stock fund to new assets after the fund doubled in size in just three years. Investor interest in REITs reached such lofty heights that the S&P 500® Index added a real estate sector in September, the first sector addition to the index since 1999.

Low rates make yield scarce

One main driver of this role reversal in asset classes has been the dearth of yield from traditional fixed income sources. With low interest rates, and even negative rates in a growing number of cases, yield had become increasingly scarce, especially through 2016 with the increasing prevalence of central bankemployed negative rates in many countries. As the OECD noted in its June 2016 economic outlook, negative policy interest rates have passed through to both short-term market rates and, in most countries, to longer-term bond yields. At midyear, negative interest rates were in place in 14 countries including Germany, Japan, Switzerland, Denmark, Italy, and the Netherlands. That’s unprecedented in centuries of financial history. By July 2016, it was estimated that about half a billion people in one-fourth of the world were living in economies with rates that were in the red. (Source: Bloomberg.)

While the United States appears poised to lift rates slowly and cautiously, the global low rate environment seems to be here to stay for a while. In some ways, central banks may be finding it harder to stay focused on their own economies without taking into account a challenged global landscape. For example, the U.S. Federal Reserve indicated early in 2016 its intention of steady increases in the federal funds rate, and then spent most of the year putting off increases. The delays occurred even in the face of improving economic data. At times the Fed cited the state of the global economy for its caution.

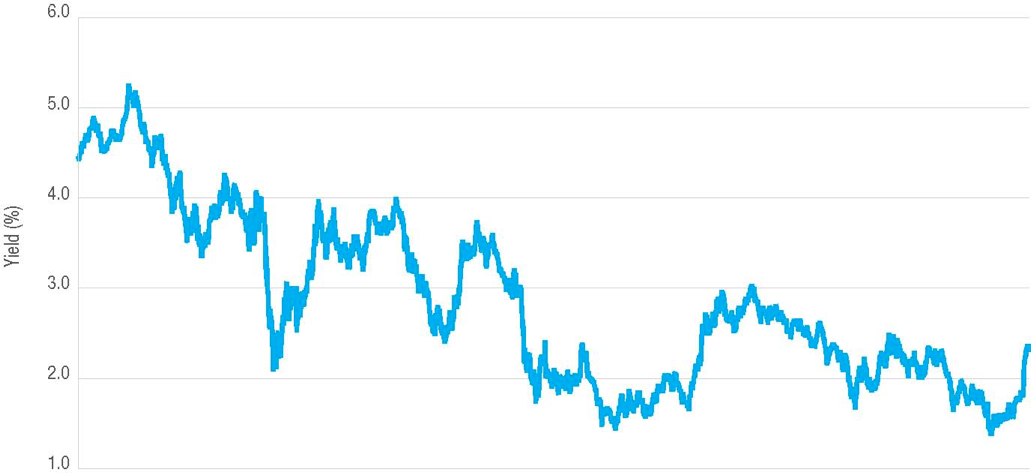

Where can you find reasonable yield?

Yield on 10-year U.S.

Treasury debt Below historical averages

At the same time, other central banks that have instigated negative rates, such as the ECB and BoJ, have engaged in such unprecedented stimulus that some observers feel it may be difficult for them to reverse course and simply start raising rates. While an increase in rates outside the U.S. isn’t entirely out of the question, central banks seem to be committed to their policies or have had other untoward events affecting their decisions. For example, following Brexit, the U.K.’s vote to leave the European Union, expectations for a rate rise in England shifted from late in 2016 to no sooner than 2020. The BoJ in September hinted that it may further lower its rates—again, rates that already were in negative territory.

The hunt for yield

With most observers expecting interest rates to stay low for the foreseeable future, investors are hunting for yield wherever they can find it. It may be a classic case for behavioral finance studies for decades to come: Market participants have exhibited herd mentality, chasing returns and seemingly turning their back on risk management.

Like moths to a light, the more capital that rushes into these assets, the dimmer their prospects seem to become. In February 2016, for example, high yield bonds briefly posted double-digit yields before record inflows pushed those yields down to about 6%. Emerging market bonds also were targeted for their relatively high yields, which promptly fell as investors poured in.

The uncertainties of finding sufficient yield in traditional asset classes have had more investors, especially institutional investors such as pension plan managers and insurers, turning to alternative sources. Alternative asset classes gaining favor among such groups have included private equity, private real estate, and multi-asset credit solutions, as well as some other nontraditional debt investments.

The paradox of savings

In a world of unprecedented monetary policies pushing interest rates to even subzero levels, the central banks’ actions are intended to encourage borrowing and spur economic activity. Yet global growth has remained tepid at best. In its July 2016 world economic update following the Brexit shock, the International Monetary Fund forecast world growth for 2016 at 3.1% and slightly more for 2017, at 3.4%. Advanced economies’ projections were lower—1.8% for both 2016 and 2017. (Both were reforecast down 10 to 20 basis points due to the aftereffects of Brexit.)

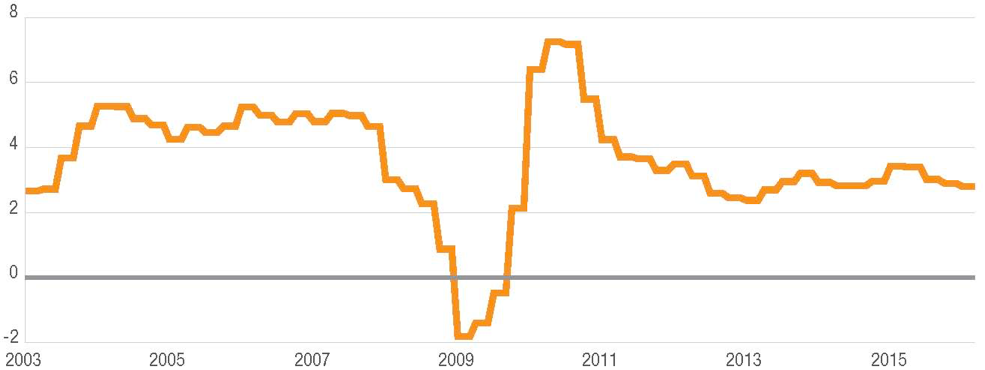

Global growth is sluggish

Global GDP growth (%YoY)

Source: Bureau of Economic Analysis

Unlike how Brexit is generally viewed, the election of Donald Trump to the U.S. presidency has been seen by some as potentially sparking some growth. This is largely because of his proposals for fiscal spending, including infrastructure projects and tax cuts. Globally, there has been something of a consensus movement toward a more fiscal spending approach, as many argue that the monetary policy led by the central banks has run its course. But while a U.S. fiscal stimulus program would likely translate into an improvement of growth domestically, there still are significant hurdles for the larger growth picture. Underlying structural headwinds to global growth—including excessive debt, aging populations changing the demographics, falling productivity, and wealth inequality—would still need to be met.

The lack of reaction to even extreme forms of monetary policy stimulus may be evidence of a big shift: one toward saving. This can be seen in examples ranging from U.S. corporations recently hoarding cash or paying dividends even as their capital expenditures decline year over year, to aging consumers in many developed economies preferring to save for retirement rather than spend, to negative rates serving as disincentives to investing.

In this paradox of savings, monetary policy—regardless of how extreme—may not have the desired stimulus effect because of the refocus on saving rather than on investing.

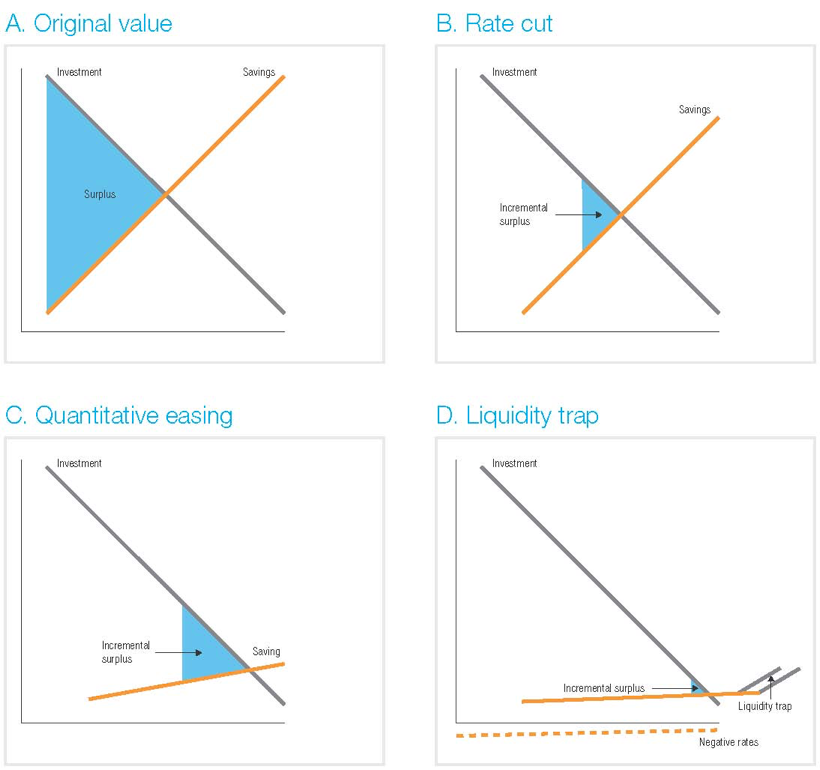

More savings means less investing—and possible liquidity trap

While central banks have tried to stimulate investing with monetary policies, these efforts can also have the effect of diminishing the amount available for investing—as this savings-investment diagram series hypothetically illustrates.

With Chart A below showing the original value created by the difference between the investment return and the cost of borrowing, the orange savings line falls further with successive stimulus efforts of a rate cut (Chart B) and quantitative easing (Chart C). The available surplus grows smaller and smaller as the savings line approaches the lower boundary of zero—ending in a liquidity trap, where cash injections from monetary policy efforts become ineffective, resulting in a lack of interest in borrowing.

The savings lever falls with lower and lower rates

In this theoretical example, the orange savings line falls with each step of a loosening monetary policy, leading to a liquidity trap. Charts are for illustrative purposes only and are not intended to convey the results of any particular investment.

The big societal driver of saving: Demographics

Several societal factors are influencing the propensity to save, including the long shadow cast by the global financial crisis of 2008–2009, which has left some investors still apprehensive about unbridled markets. In addition, the global financial crisis has propelled the world, we believe, into a general over-reliance on monetary policy in the hope of more spending through economic stimulus, but the outcome has been that most central bank action has only helped to push rates lower and lower.

One of the main drivers, however, lies in demographics. Simply put, people are living longer than they work and need to save for that longevity.

Longevity in much of the world’s population generally has been increasing. In 1960, the average American could expect to live only one to two years after retirement at age 65, with an average life expectancy of 66.6 years. Women could expect to live an extra eight years to about 73. By 2010, a 65-year-old male retiree could expect to live more than 11 years, and women more than 16. (Source: National Center for Health Statistics)

With populations in many developed countries expected to live longer, with access to better healthcare and other factors, those consumers tend to save, and save for a longer retirement. This phenomenon can even affect a developing market country like China. There, without a broad-based retirement system, the family would act as a safety net. But because of their past one-child policy, workers in China have had to make up their saving gaps themselves.

Individual investors are finding they need to adapt to a low-yield, low-growth environment for the fixed income portion of their portfolio. For the current workforce, that might mean saving more or prolonging retirement by working longer. Retirees might continue to crave the downside protection and steady stream of income that are hallmarks of traditional fixed income investing, but this may prove difficult as they increase their exposure to fixed income in a yieldchallenged environment. Some are increasingly looking to other types of assets that might generate palatable returns, but that, of course, have commensurate higher risk.

Adapting to low yields can also be more of a hurdle for investors in various geographic regions, where there are different mindsets about investing. For example, it’s common for investors in the U.S. to have retirement accounts allocated at between 60% and 100% equities, depending on their age and propensity to risk. In Europe, however, investors tend to be heavily weighted toward fixed income. In Germany, for instance, even when yields have been in negative territory as they were in 2016, a traditional portfolio is still considered to be 70%–80% fixed income with only 20%–30% in stocks. In an environment where yields are likely to remain low for a while, many investors may need to readjust their thinking as well as their expectations.

The economic effect of aging Japan

The combination of an aging population and shift to savings can affect an economy–even for years as seen in the example of Japan. Population growth in Japan began shrinking in the mid-1990s and has remained negative since then—coinciding with Japan’s 20-plus years of prolonged recession. (Source: Macquarie)

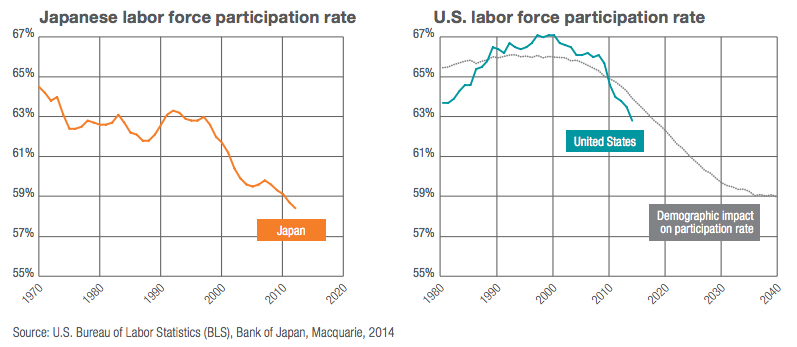

This kind of impact of aging populations can make economies like the U.S., which has a larger base of younger workers, not entirely immune. This chart shows falling U.S. labor participation rates over a decade and how they compare with the Japanese experience.

Will U.S. labor force participation follow a path similar to Japan’s?

Source: U.S. Bureau of Labor Statistics (BLS), Bank of Japan, Macquarie, 2014

Institutional investors’ low yield high risk dilemma

As individual investors save more, and cash piles up and is recycled into global capital markets, the net effect is helping to keep rates depressed and investors chasing yield in a vicious cycle. With these protracted low and negative rates, the financial strain is not only affecting institutional investors, including definedbenefit pension plans and insurers—it’s creating a dilemma for them. With low benchmark bond yields, these investors could face falling short on the returns needed to meet funding obligations to match their expected liabilities, or else taking on so much risk that it could prove perilous for their portfolios.

Paying for the future value of pension and insurance assets has been made more difficult by changing demographics—longer retirements and more retirees pressuring pension plan funding, for example. However, low interest rates and yields have made funding harder without even taking demographics into account. That’s because bond yields are generally used as the discount rate for institutional investors. The cost of a pension may not fall due for decades, so pension plans must discount that future cost to figure out how much to set aside. Higher discount rates means lower costs at present—and lower yields translate to more current funding needed.

A low discount rate increasing the present value of liabilities of pensions and insurers can also affect aspects such as meeting regulatory minimums and funding requirements. In the U.S., there have been indications of these stresses in both public and corporate pension plans. For example, the benefits consulting firm Mercer reported a combined deficit for S&P 1500 company pension plans of $568 billion as of June 30, 2016, a $164 billion increase from year-end 2015. And in an October 2016 report, Moody’s Investors Service said that total unfunded liabilities for U.S. state public pensions will balloon by 40% to $1.75 trillion through fiscal 2017, up from $1.25 trillion in 2015.

Casting the net wider into risk

As a result of these factors, institutional investors are attempting to capture a return profile that could meet liabilities. Also, some have restrictions on how much they can invest in negative-yielding debt. That leaves many of these investors not only searching further afield for securities that could meet their mounting obligations, but also pushing boundaries on risk as they do so.

The research firm Callan Associates conducted a recent analysis that showed investors need to take on almost three times as much risk as they did only 20 years ago to achieve a 7.5% return, once a benchmark that many institutions strived to attain. In 1995, a portfolio composed entirely of fixed income was projected to earn 7.5%. Today, though, the low-rate environment means that stocks and alternatives such as private equity need to do much more of the lifting to reach that mark, dropping the fixed income allocation down to 12%.

In this balancing act of risk and return, institutional investors have been exploring more equity solutions, real estate, and alternative investments. Non-traditional debt instruments have been appealing to this group, including private placement and infrastructure debt. Even taxable municipals have attracted an audience of non-U.S. investors in the global low-yield environment.

How low yields could reinforce the need for active fixed income

A number of forces have contributed to low yields: aging populations shifting the savings dynamic, the lingering ills of the global financial crisis, and unprecedented central bank policy pushing rates lower still. Against this backdrop, fixed income investors may feel that there are not many good choices. They could add exposure to higher yielding assets but then they also are increasing risk and volatility to their portfolios. They might extend the duration of their fixed income assets and try to wait it out until interest rates pick back up—with any significant increases considered unlikely. Or they might move into lower credit quality, or into less liquid types of investments such as direct loans or infrastructure debt, all of which can increase risk.

Despite its relatively low yield and reliance on price appreciation, fixed income appears to play a strong role in investors’ portfolios. Bonds, in our view, are still likely to have more downside protection than stocks or private equity, which historically have shown far more volatility than fixed income. There also continues to be a key place for fixed income in portfolio diversification—even though there have been recent periods when correlations between bonds and stocks have increased, they are far from perfectly correlated.

How do investors gain confidence that the fixed income assets in their portfolio can continue following these same patterns—and act as bonds—even as they pursue riskier, higher yielding corners of the fixed income market? The answer may lie in active management of fixed income allocations.

Leading active managers take a disciplined approach, focus on solid fundamental work, and effectively manage the risks related to extending durations, moving down the spectrum in credit quality and locking up capital in less liquid assets. As such, they can assemble a basket of securities with the goal of helping to spread risk while offering the potential for above-market returns even amid low yields.

For some investors, the current unusual low-yield environment may call for investments that combine goals, strategies, and asset classes. For these types of complex investments—for example, those that are multi-asset, cross-geography, a blend of short and long duration, and even denominated in different currencies—investors may want to consider actively managed funds as well. These blended funds might have exposure to municipal and emerging market bonds as well as high yield bonds. If constructed properly, based on fundamental research and an eye toward negative correlation and diversification, these funds could find yield in a yield-starved market.

Conclusion

Fixed income investing in recent years has been turned on its head as yields have plummeted, bond prices have soared, and income has taken a back seat to appreciation. In some cases, investors have abandoned fixed income assets in favor of alternatives offering the potential for higher, long-term returns—without fully considering the risks involved.

Even in a protracted low-yield environment, fixed income still deserves a place in investor portfolios, owing to the traditional benefits it provides in the form of downside protection and diversification. Sticking with the asset class should not mean sacrificing returns and investor obligations or objectives. There are ample opportunities to pursue higher yield within the fixed income spectrum. The key is to seek those opportunities in a disciplined and methodical way that puts a premium on sound research and risk management—the hallmarks of leading active managers.

The views expressed represent the Manager’s assessment of the market environment as of January 2017 and should not be considered a recommendation to buy, hold, or sell any security, and should not be relied on as research or investment advice.

Views are subject to change without notice and may not reflect the Manager’s views.

Investing involves risk, including the possible loss of principal.

Past performance is no guarantee of future results.

All charts throughout are for illustrative purposes only.

The S&P 500 Index measures the performance of 500 mostly large-cap stocks weighted by market value, and is often used to represent performance of the U.S. stock market.

The Bloomberg Barclays Global Aggregate Index provides a broad-based measure of the global investment grade fixed-rate debt markets.

Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index.

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations. Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

High yielding, non-investment-grade bonds (junk bonds) involve higher risk than investment grade bonds.

REIT investments are subject to many of the risks associated with direct real estate ownership, including changes in economic conditions, credit risk, and interest rate fluctuations. A REIT fund’s tax status as a regulated investment company could be jeopardized if it holds real estate directly, as a result of defaults, or receives rental income from real estate holdings.

Diversification may not protect against market risk.

All third-party marks cited are the property of their respective owners.

Neither Delaware Investments nor its affiliates noted in this document are authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited (MBL). MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities, unless noted otherwise.

Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

© 2017 Delaware Management Holdings, Inc.