Puerto Rico last week declared a form of bankruptcy under Title III of the Puerto Rico Oversight, Management, and Economic Stability Act (PROMESA) after a stay on litigation expired and negotiations with creditors broke down. In many ways these filings may mark “the end of the beginning” (as Churchill once said) of this chapter for Puerto Rico, as the commonwealth moves to write down a majority of its roughly $73 billion of financial debt. While consensual restructurings are still possible for some classes of claims, Title III is the fastest means to usher Puerto Rico into the next phase of its credit cycle: recovery.

Impact on muni markets

PIMCO sold the last of its Puerto Rico government debt from municipal-focused client portfolios in 2013.1 We believed then that the property rights on the island’s bonds were inadequate and that pensions might be prioritized above debt in distress. In addition, we held a view that a federal intervention would be necessary in the event of a default (using the auto industry bailouts during the global financial crisis as a guide for what might happen to creditors). We do see pockets of opportunity in select revenue bonds and have added a small amount of Puerto Rico enterprise debt to municipal high yield portfolios (but remain void of Puerto Rico primary government debt).

Here are some of our initial takeaways:

Puerto Rico’s Title III filing is an idiosyncratic event that will not have an impact on the broader municipal market. PROMESA has no application to U.S. states, and we do not foresee any state seeking a financial debt restructuring. In addition, the macroeconomic issues contributing to Puerto Rico’s crisis are not in evidence on a similar scale elsewhere in the U.S. municipal market.

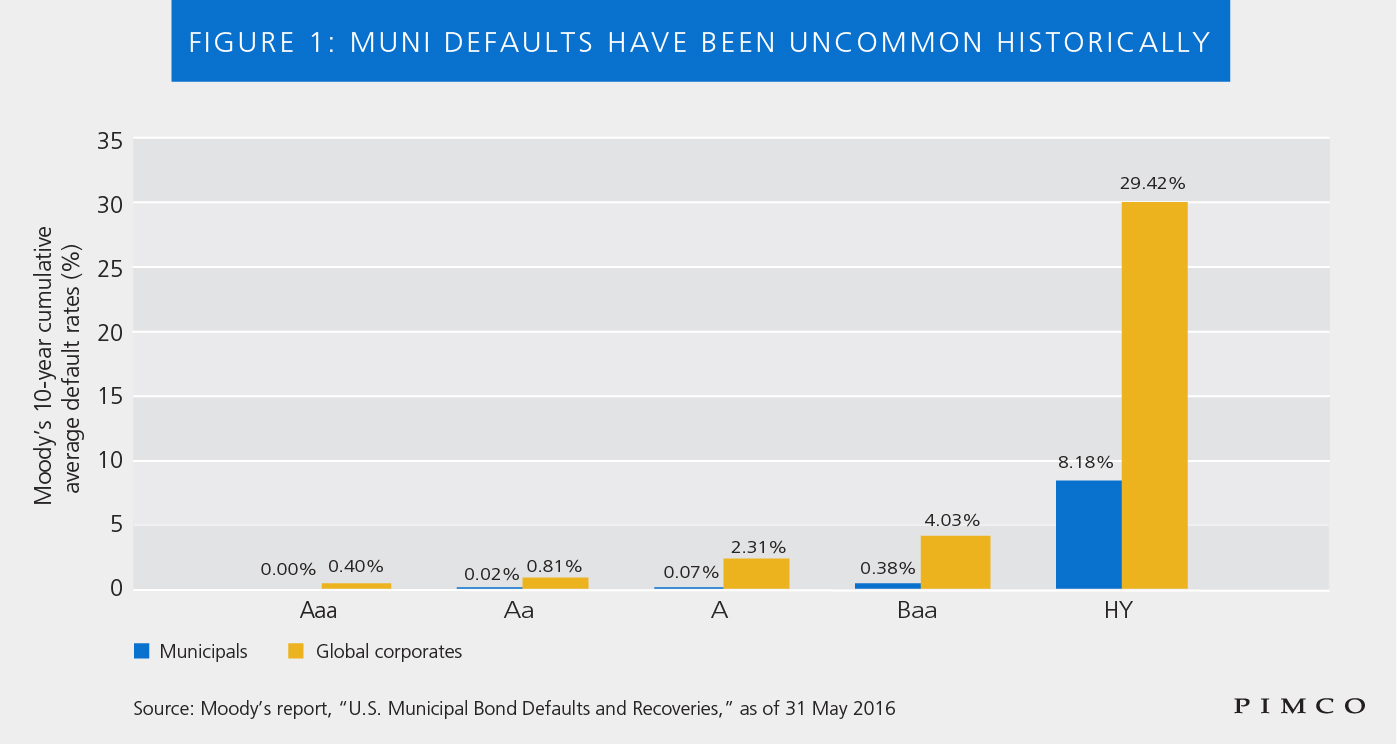

However, Puerto Rico’s experience does reinforce an important theme for municipal bond investors, learned during the Detroit bankruptcy: GO bonds are not immune if an issuer suffers financial distress, and they may be subject to impairment absent a statutory lien. This insight is among several reasons why PIMCO municipal portfolios continue to favor larger relative allocations to essential-service revenue bonds, which contain security features that we view as more defensible in a bankruptcy. We note that defaults of municipal bonds have been uncommon historically, especially relative to corporate debt (see Figure 1).

Haircuts on aggregate primary government debt, including GO bonds and COFINA bonds, will likely be more severe than what current market prices imply. We would have expected a larger drop in bond prices year-to-date considering the PROMESA Financial Oversight and Management Board announced a “once-and-done” approach to addressing Puerto Rico’s fiscal difficulties. Investors should bear in mind that the 10-year fiscal plan certified by the board projects that cash flow available for debt service will cover less than 25% of the scheduled amount due, even if fiscal measures are successful. And while the board is responsible for filing a restructuring plan, it will likely allow the government to craft the initial proposal. This puts creditors at a disadvantage because they may not propose alternative plans.

Recent commonwealth proposals also reveal that Puerto Rico does not consider the COFINA bonds a valid claim on sales tax revenues, nor does it recognize the seniority of the senior COFINA securities over the junior liens. Reducing the stock of COFINA debt might allow the island to lower the sales tax levy, which is already very high, to the benefit of consumers on the island.

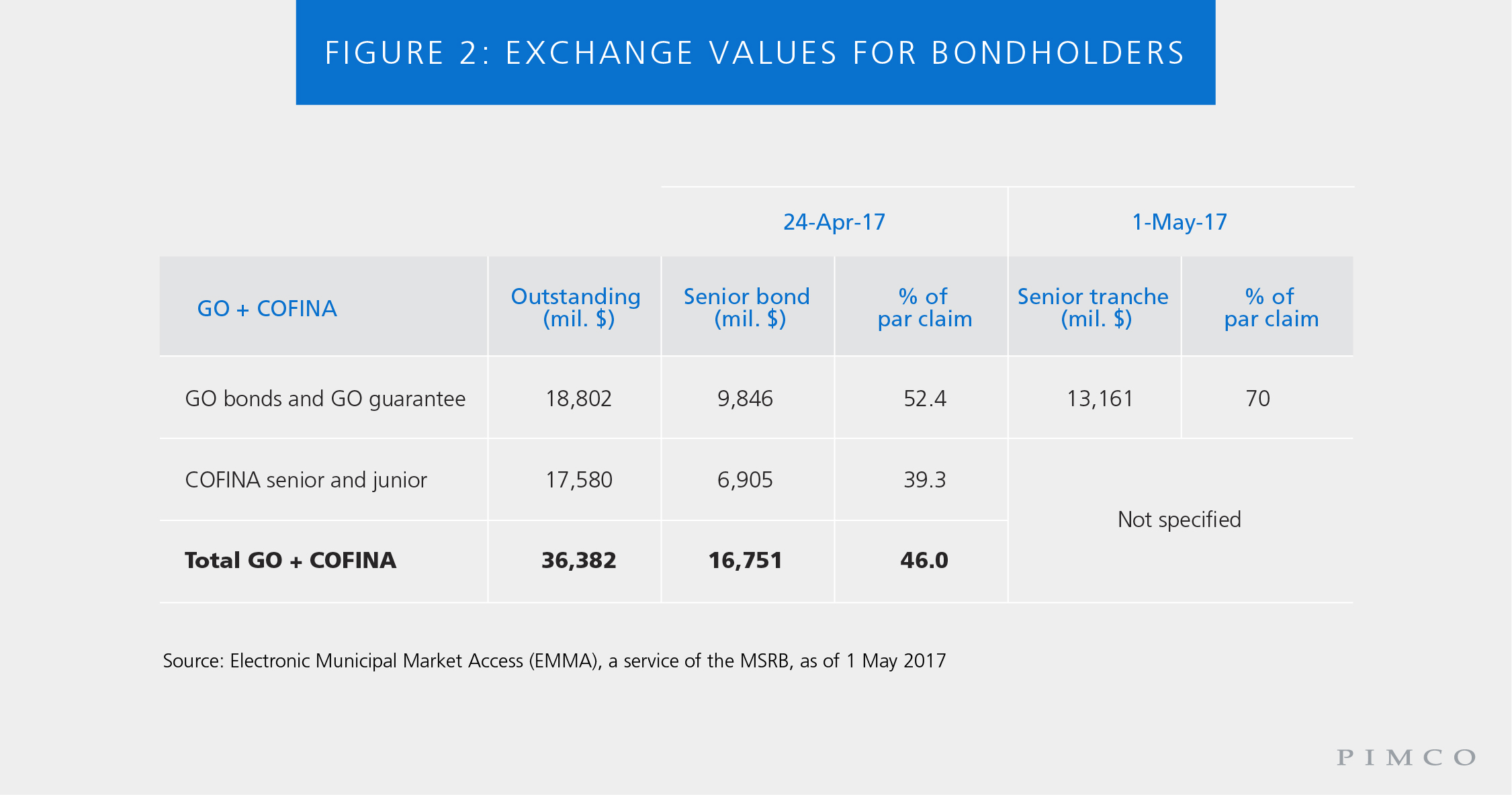

Perhaps most important, the proposals reveal harsh terms for creditors (see Figure 2), including low exchange ratios for a new class of senior notes. The most recent proposal offered GO bondholders an exchange of 70 cents on the dollar for a senior note and a coupon of 5%; however, the recovery value will also depend on the “exit yield” the market uses to discount post-restructuring cash flows, which we believe will be highly punitive. The new security will thus likely trade at a much deeper discount dollar price relative to the exchange offer, reflecting a discount rate of a distressed instrument, notwithstanding the continued involvement of the oversight board. Additionally, we expect a higher discount rate on the subordinated note given the uncertainty of the residual cash flow.

Puerto Rico will likely regain market access once its debt stock is sustainable. Creditors have expressed concern about the fiscal plan’s inclusion of a “reconciliation adjustment” in the fiscal plan and, specifically, whether this item renders the fiscal plan non-compliant with PROMESA. We agree this item is unusual, but it may allow the island to withstand future budget shocks.

In addition, all things being equal, the greater the haircut to debt, the more likely Puerto Rico’s fiscal plan will be sustainable. The exchange ratios in Governor Ricardo Rossello’s 24 April debt restructuring proposal implied a substantial reduction of the ratio of debt to gross national product (GNP). Paradoxically, the lower the level of post-restructuring debt, the sooner Puerto Rico likely will access capital markets at reasonable interest rates.

What’s ahead?

A key step occurred on Friday with the appointment of Judge Laura Swain of the District Court for the Southern District of New York, a former federal bankruptcy judge, to oversee Title III cases. However, it is unclear at this stage whether these cases will be heard in San Juan or New York City. The duration of a full workout under Title III also remains uncertain, but given the complexities, we expect it could take considerably longer than most municipal bankruptcies.

In addition, Puerto Rico recently passed the Fiscal Plan Compliance Law (House Bill 938), which gives the island the ability to claw back funds from COFINA to “cover an occasional significant cash flow deficiency to comply with the Government’s fiscal plan.”2 COFINA has continued to pay debt service, but the passage of this legislation throws considerable doubt on future coupon payments (we note that the board certified a Title III filing for COFINA on Friday).

Puerto Rico still has a long way to go, and the Title III process is sure to contain surprises. But to quote Churchill again, “This is not the end. It is not even the beginning of the end” – and PIMCO will be watching as events unfold to gauge the commonwealth’s potential to exit the distressed debt market and return to the municipal bond market.

Sean McCarthy is PIMCO’s head of municipal credit research and a regular contributor to the PIMCO blog.

1 Non-municipal-focused portfolios managed by PIMCO may have held or continue to hold Puerto Rico municipal bonds that have been economically and legally defeased by U.S. Treasuries.

2 See Appendix I to the Puerto Rico Sales Tax Financing Corporation Annual Financial Information and Operating Data Report, which can be found on the FAFAA website: http://www.aafaf.pr.gov/documents.html

© PIMCO

© PIMCO

Read more commentaries by PIMCO