SUMMARY

-

Central banks were in focus in July.The Federal Reserve’s meeting minutes indicated increasing likelihood that it would begin balance sheet normalization soon, while the Bank of Canada raised rates for the first time in seven years. Meanwhile, U.S. politics remained in the headlines, with the Russia investigation continuing and the Senate struggling to pass healthcare reform.

-

Global growth data remained steady, but inflation pressures remained subdued. Growth and employment data were robust in the U.S., though softer inflationary trends persisted. In Europe, the euro area grew twice as fast as the UK in the second quarter.

-

Low market volatility continued to fuel risk appetite, driving equities higher and interest rate curves steeper. Emerging market equities in particular registered strong returns in July. Meanwhile, the dollar fell for the fifth month in a row, and yield curves around the world generally steepened.

In the world

Central banks were in focus in July for signs of change to monetary policy. Minutes from the June Fed meeting indicated that several members were increasingly comfortable beginning normalization of the Fed’s balance sheet before the end of the year. Still, while Fed Chair Janet Yellen emphasized in her semiannual testimony to Congress that the fundamental economic backdrop remained robust, she also noted that inflation had been persistently sluggish this year. Meanwhile, the Bank of Canada became the first developed market central bank to follow the Fed in raising rates, its first hike in seven years. Across the Atlantic, though the European Central Bank (ECB) left interest rates and forward guidance all unchanged and avoided talk about tapering asset purchases, German yields generally rose in anticipation of some reduction in ECB support. Even in the midst of usually slower summer months, there was no respite from news out of Washington. Reports that President Trump’s son and key advisors met with a Russia-linked lawyer kept the ongoing Russia investigation in the headlines. The Republican Party’s ongoing challenges in enacting the administration’s policy agenda were also highlighted again when the U.S. Senate voted against the repeal of the healthcare law known as Obamacare.

Global growth data remained steady, but inflation pressures remained subdued. U.S. growth measures were more upbeat this month: Second quarter GDP registered a 2.6% annualized pace, rebounding nicely from a relatively weak first quarter and putting the U.S. on track for 2% annual growth in 2017. The U.S. labor market also surprised to the upside as the unemployment rate ticked down to 4.3% with a larger-than-expected 222,000 jobs added to payrolls. However, the lack of inflationary pressures was notable: Wage growth remained muted, core CPI ticked up only slightly from last month and was again weaker than expectations, and a second monthly decline in retail sales highlighted consumer caution. In Europe, the euro area grew twice as fast as the UK in the second quarter as GDP in the economic block expanded 0.6%, building on growth of 0.5% in the first quarter, while the UK expanded by only 0.3% in the same period. Growth in the services sector buoyed the expansion in the UK, though a contraction in manufacturing and construction, along with a slip in PMI data, could indicate potential post-Brexit weakening.

Low market volatility continued to fuel risk appetite, driving equities higher and interest rate curves steeper. The MSCI World Index rose 2.4% amid a strong start to the second quarter earnings season, taking year-to-date gains to 13.3%. With a robust 6% return in July, emerging market equities (MSCI Emerging Markets Index Daily Net TR) extended their positive run in 2017 to over 25%; Brazilian stocks reacted positively to the conviction of former President Lula on corruption charges, Russia benefitted from higher oil prices, and Chinese equities were supported by better-than-expected second quarter GDP growth. The U.S. dollar fell for the fifth month in a row, as weaker inflation data in the U.S. reduced the odds of a hawkish Fed, and expectations for less supportive monetary policy globally benefitted non-U.S. developed market currencies. The euro continued to gather steam on growth optimism and higher bond yields, and the Canadian dollar strengthened in response to the Bank of Canada’s first rate hike in seven years. In the U.S., yields trended higher early in the month but fell modestly along most of the curve as Fed Chair Janet Yellen struck a cautious tone in comments she made to Congress. Despite some investors banking on change, the U.S. 10-year Treasury yield ended the month just under 2.3%, only a few basis points away from where it finished 2015.

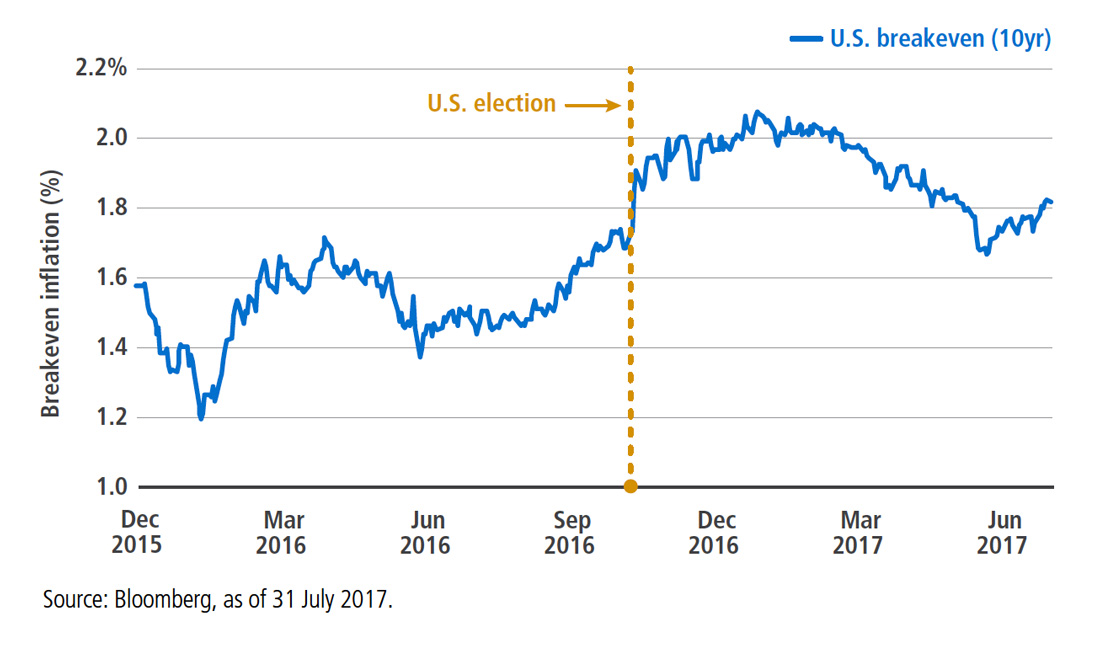

Round Trip

In the U.S., the 10-year breakeven inflation rate – the difference between nominal and real yields and a measure of inflation expectations – rose in July for the first time in five months. The month began with the breakeven rate at 1.74%, about the same level it had been just prior to the U.S. election. President Trump’s surprise victory had propelled the rate to as high as 2.08% on the back of expectations for fiscal stimulus and its likely inflationary effect. The subsequent slide in the breakeven rate had been a result of various factors including falling oil prices and underwhelming inflation data, but diminishing expectations for the extent of fiscal stimulus, if any, also contributed. July’s increase in breakevens to 1.82% was helped by oil prices rising again, but stimulus expectations, inflation data and Fed policy all will continue to be factors in the direction of breakeven rate moves.

In the markets

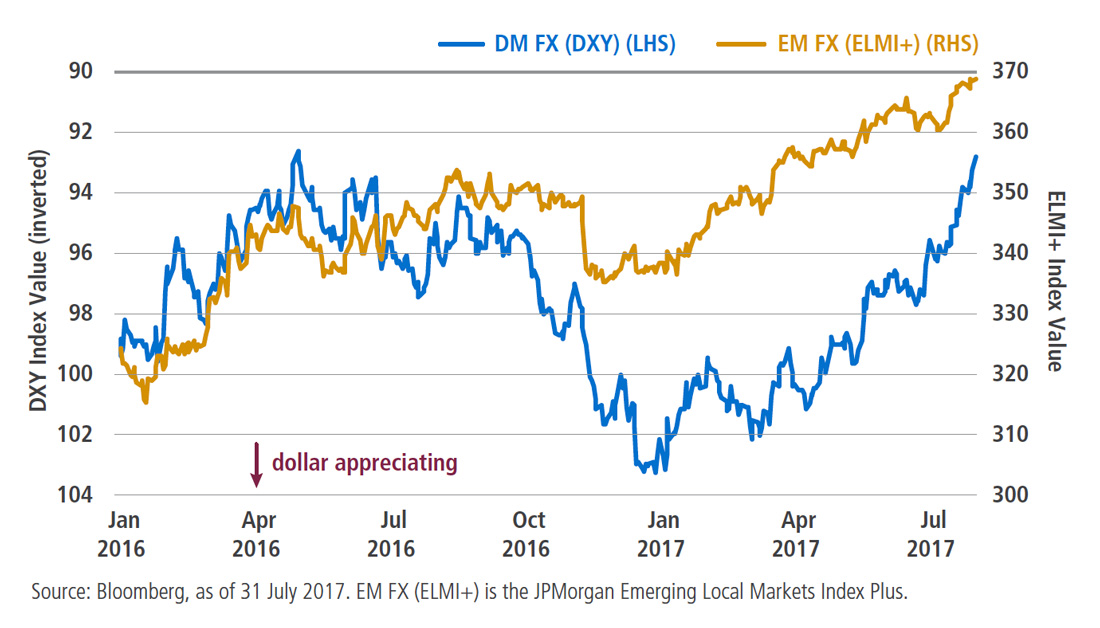

International Factors at Play in the USD’s Recent Moves

The U.S. dollar fell again in July against other developed market currencies (as captured by the DXY Index), touching 13-month lows in its fifth consecutive monthly decline. Fed Chair Yellen’s more cautious testimony and soft inflation data contributed to the dollar’s decline, but developments internationally, including the perception of less accommodative global central banks, also added to other currencies’ appreciation against the greenback. In particular, the euro gained 3.6% on the month, the yen nearly 2%, and the pound 1.5%. Emerging market currencies also saw gains against the dollar, as captured by JPMorgan’s emerging markets currency index (ELMI+). Index gains were generally broad-based, helped in particular by Asian and Latin American currencies.

EQUITIES

Low financial volatility and robust risk appetite drove developed market stocks1 to return 2.4% in July. In the U.S.2, equities returned 2.1% amid a strong start to the second quarter earnings season, led by technology and financial companies. However, European stocks3 fell 0.4% as investors feared that a stronger euro might hamper corporate profit growth. Japanese equities4 fell 0.5% after the yen strengthened and Prime Minister Shinzo Abe’s ruling party faced an upset in Tokyo’s assembly election.

In emerging markets5, stocks benefitted from relatively stable global market conditions and a strong technical backdrop, returning 6.0%. In Brazil6, stocks rose 4.8% as investors cheered the conviction of former President Luiz Inacio Lula da Silva on corruption charges. Chinese equities7 returned 3.7% after the National Bureau of Statistics reported better-than-expected second quarter GDP growth. In India8, positive sentiment and ample liquidity drove stocks up 5.4% to record highs, while Russian stocks9 rose 4.8% on higher oil prices.

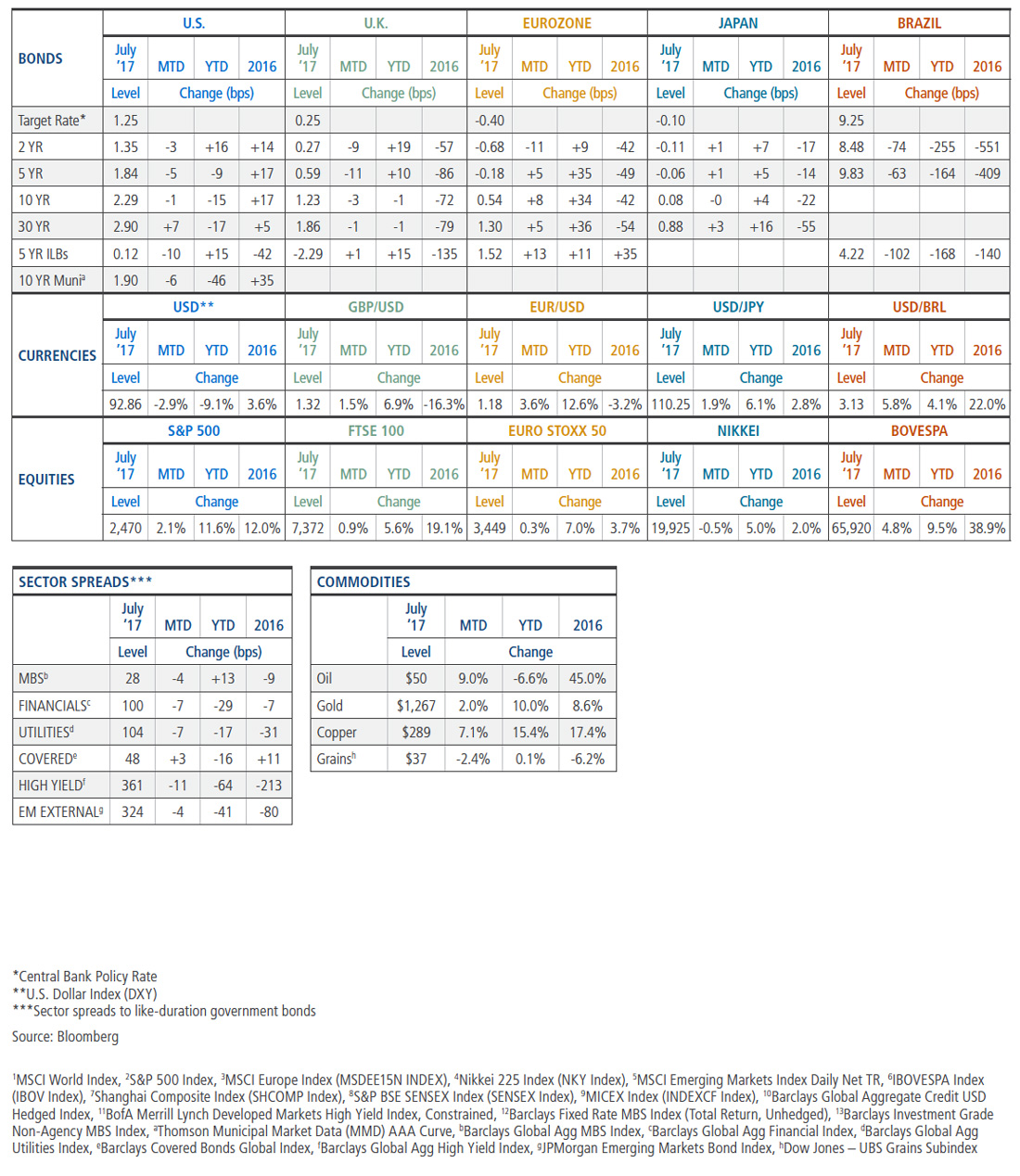

DEVELOPED MARKET DEBT

Yield curves generally steepened over the month on expectations that central banks globally were becoming less accommodative. In the eurozone, ECB president Mario Draghi attempted to clarify comments made in June that had initially sparked a sovereign bond sell-off, but German 10-year rates still ended July higher. Meanwhile, the Bank of Canada moved its policy rate higher for the first time in seven years, causing Canadian rates to rise, and the 10-year ended the month 32 basis points (bps) higher. In the U.S., yields rose early in the month but fell modestly along most of the curve as Federal Reserve Chair Janet Yellen struck a cautious tone in comments she made to Congress. The U.S. 10-year Treasury yield ended the month just under 2.3% – only a few basis points away from where it finished 2015.

INFLATION-LINKED DEBT

Global inflation-linked bond markets (ILBs) posted gains across most countries, and breakeven inflation levels generally rebounded after months of weakness amid a surge in oil prices. U.S. TIPS outpaced nominal Treasuries for the month, aided by energy market gains, despite a fourth consecutive downside surprise to the Consumer Price Index (CPI) and historically weak demand in the 10-year TIPS auction. In the U.K., inflation readings came in well below consensus forecasts; the Retail Price Index (RPI) fell to 3.5% year-over-year from 3.7% previously. The weakness in U.K. inflation, along with continued appreciation of the British pound, led index-linked gilts to sharply underperform their nominal counterparts. Within emerging markets, front-end Brazilian breakeven inflation rates spiked higher following the announcement of a larger-than-expected fuel tax hike; longer-term inflation expectations were flat to slightly lower.

CREDIT

Investors focused on improving earnings and prospects for global growth, driving equities higher, and global investment grade credit10spreads tightened 5 bps, outperforming like-duration global government bonds by +0.50%. Strong market technicals supported investment grade credit, including continued investor demand for stable yield above global government bonds.

Global high yield bonds11 also rallied, and yields continued their decline, reaching a three-year low in conjunction with a sharp climb in oil prices, benign rates and rallying stocks. Yields declined nearly 25 bps to 4.84% month-over-month and spreads compressed 17 bps to end the month at 343 bps, boosting the return for global high yield by 1.14% in July.

EMERGING MARKET DEBT

Returns for emerging market (EM) debt were positive in July: Spread tightening drove performance in external debt, and falling index yields drove performance in local currency debt. Brazilian local debt was a notable outperformer after the conviction of former President Lula diminished the ability of his opposition party to block the ruling coalition’s reform agenda. Returns rose further when the central bank continued its deep rate-cutting cycle amid falling inflation. Local assets in Hungary, Romania and the Czech Republic outperformed as their currencies appreciated alongside the euro. After stalling in the first half of July, robust fund flows into emerging market debt resumed at the end of the month.

MORTGAGE-BACKED SECURITIES

Agency MBS12 returned 0.45% and outperformed like-duration Treasuries by 24 bps, driven by lower volatility and range-bound interest rates. Overall, Ginnie Mae MBS outperformed conventional MBS, 15-year MBS marginally outperformed 30-year MBS, and higher-coupon conventional MBS outperformed lower-coupon conventional MBS. Of note, in its July meeting, the Fed said it expects to begin tapering its balance sheet “relatively soon,” fueling expectations of unwinding in the autumn. Gross MBS issuance increased 3% from June, while prepayment speeds increased 8% amid summer’s higher housing turnover. Non-agency MBS prices rose moderately, and spreads relative to swap rates generally tightened. Non-agency commercial MBS13 returned 0.76% and outperformed like-duration Treasuries by 39 bps.

MUNICIPAL BONDS

Muni bonds rallied across the yield curve, supported by weaker-than-expected economic data and negative net supply. The Bloomberg Barclays Municipal Bond Index returned 0.81% in July, bringing year-to-date returns to 4.40%. Most notably, Illinois outperformed over the month: All three rating agencies affirmed the state's investment grade ratings after it resolved its budget impasse. Conversely, Puerto Rico bonds continued to suffer the consequences of the island’s ongoing restructuring efforts. After years of negotiation between Puerto Rico’s Electric Power Authority and its creditors, the federal oversight board voted to place the authority into Title III bankruptcy protection. On the policy front, the U.S. government’s failure to repeal and replace the Affordable Care Act removed some near-term concerns regarding healthcare credits, especially in states with expanded Medicaid coverage.

CURRENCIES

Economic and political developments drove the U.S. dollar to new lows in July, its fifth monthly decline in a row. Weak inflation data in the U.S. reduced fears of a hawkish Fed in the near term, while solid economic data in other developed markets supported expectations for tighter monetary policy globally. Notably, the euro continued to gather steam against the dollar as ECB President Mario Draghi refrained from commenting on the currency’s recent strength. Meanwhile, the Bank of Canada became the first G10 central bank to follow the Fed in raising rates, and the Canadian dollar rallied in response. In emerging markets, the Argentine peso fell almost 6% for the month – a fall so rapid that the central bank was forced to intervene.

COMMODITIES

Broad commodities posted positive returns in July. Energy was the top performer: Healthy demand and refinery outages lifted gasoline and other product prices and crude oil followed. Natural gas sold off, however, as production hit year-to-date highs in the absence of any meaningful weather-related demand. Returns in the agriculture sector were muted as gains in the majority of these commodities were offset by a reversal in wheat prices and modest losses in corn. A weaker U.S. dollar and import data from China supported base metals. Nickel outperformed the rest on news from the Philippines suggesting that export curtailments would continue. In precious metals, gold led a rally amid lower real yields.

Outlook

PIMCO expects the eight-year-old global economic expansion will continue to strengthen and broaden for the remainder of 2017, driving global GDP growth to 2.75%–3.25% from 2.6% in 2016 and boosting CPI inflation to 2.0%–2.5%. Our outlook reflects several positive factors: generally supportive fiscal policies (or expectations of them) in most developed market economies, easier financial conditions since the start of the year, positive animal spirits as indicated by consumer and business confidence data, and a rebound in global trade.

In the U.S., we see growth above-trend at 2%‒2.5% in 2017 as business investment recovers, particularly in the energy sector, and consumer spending is supported by a further decline in unemployment, high consumer confidence and expectations of personal income tax cuts ahead. We forecast core inflation to hover sideways this year at 1.75%–2.25%, owing to some softer trends of late. With policy normalization under way, we expect the Fed to embark on reducing its balance sheet by gradually tapering its reinvestments in a predictable and transparent manner.

For the eurozone, we expect growth will be in a range of 1.75%‒2.25% in 2017, revised higher from our forecast in March to reflect the stronger momentum this year. While political uncertainty remains ahead of elections in Germany and potentially Italy, the likelihood of disruptive populist outcomes has diminished. In addition, both fiscal and monetary policy are expansionary, and the recovery in global trade growth supports exports and investment. We anticipate core inflation remaining well short of the European Central Bank’s (ECB) “below but close to 2%” objective, but the solid growth momentum will likely allow the ECB to taper and eventually end its purchases from early next year.

In the U.K., we expect growth to be in the range of 1.5%–2.0%despite Brexit, reflecting robust momentum, higher government spending and a positive contribution from net trade on the back of the 15% drop in the pound in 2016. We forecast CPI inflation to exceed the Bank of England’s 2% target but expect the Bank to leave policy rates unchanged this year.

Japan’s strong private demand and export growth should support GDP growth of 1.0%‒1.5% in 2017 while inflation remains significantly below the 2% target. The Bank of Japan is likely to keep targeting the overnight rate at –0.1% and the 10-year bond yield at 0% and thus continue its standing invitation to the government to engage in additional fiscal expansion, which we expect to happen later this year.

China’s public sector credit bubble and private sector capital outflows will likely remain under control, and we expect growth in a 6.25%‒6.75% range in 2017 as policymakers prioritize financial stability over economic stimulus ahead of the 19th National Party Congress in the fourth quarter. Any trade war with the U.S. will likely involve words rather than action, and we expect the yuan to depreciate gradually against the U.S. dollar.

In emerging markets, we expect moderate growth in Brazil and Russia in 2017 as they emerge from recession. With inflation dropping, both countries’ central banks have room to cut rates further. We expect Mexico’s growth to be 2.75%-3.25% with the potential for Banxico to adopt an easier policy stance if inflationary pressures abate.

In sight

Last call for Libor?

The UK Financial Conduct Authority (FCA) announced on 27 July that it would no longer support the London Interbank Offered Rate (Libor) after 2021. The now ubiquitous interest rate benchmark first emerged in 1969 as a means to set a variable interest rate that reflected changing market conditions and could be observed among a group of banks. Libor expanded beyond the syndicated loan market and became a key benchmark for pricing derivatives contracts as well as mortgages and student loans.

However, the Libor-fixing scandal that emerged during the financial crisis revealed its limitations: the potential for manipulation and declining transaction volume. While Libor may persist after 2021 under a new regulatory body or member banks, derivative trading linked to other benchmarks will undoubtedly increase. The Alternative Reference Rates Committee (ARRC), a Federal Reserve-sponsored group, recently announced its endorsement of the Board Treasuries Financing Rate (BTFR), a collateralized repurchase (repo) rate, while Europe and Japan are veering towards unsecured rates as alternatives to Libor.

To successfully navigate the changing landscape over the next few years, investors will need to adapt to Libor’s declining prominence and stay informed as other benchmarks gain traction.

Appendix

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax; a strategy concentrating in a single or limited number of states is subject to greater risk of adverse economic conditions and regulatory changes. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation- Protected Securities (TIPS) are ILBs issued by the U.S. government. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO