SUMMARY

- Policy Antidotes to Rising Drug Prices

- The Nature of Spanish Recovery

- North Korea Isn’t Worthy of Overreaction

I was very disappointed at the recent health care fiasco. No, I’m not referring to the failure of Congress to replace or reinforce the Affordable Care Act (ACA). The fiasco I am talking about was my daughter’s earring mishap. She and a friend apparently improvised new openings in their lobes without professional supervision. A few weeks later, I came home to find her in pain from a faux rhinestone stud that had become embedded in the improperly sized hole. It took a trip to the clinic to unearth the darn thing.

The evening’s entertainment didn’t end there. To guard against infection, she was directed to take an antibiotic, which we had to acquire from a local pharmacy. Given my luck that day, it wasn’t surprising that a long line of folks were waiting for their prescriptions. The whole affair took nearly three hours of my life, which I will never get back.

In retrospect, one aspect of that sad episode should not have come as a surprise. America consumes a lot of pharmaceuticals (I’m referring here to the legal kind), so a long line at the dispensary is not uncommon. Given our demographics and the structure of the U.S. medical industry, it’s likely that those lines will be getting even longer in the years ahead. That trend, combined with other health care challenges, could test finances in both the public and private sectors.

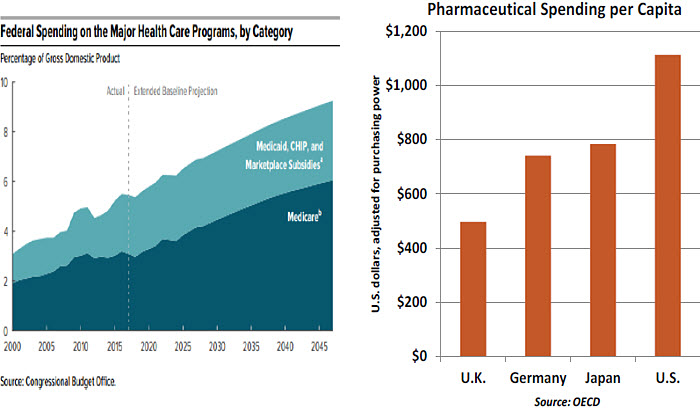

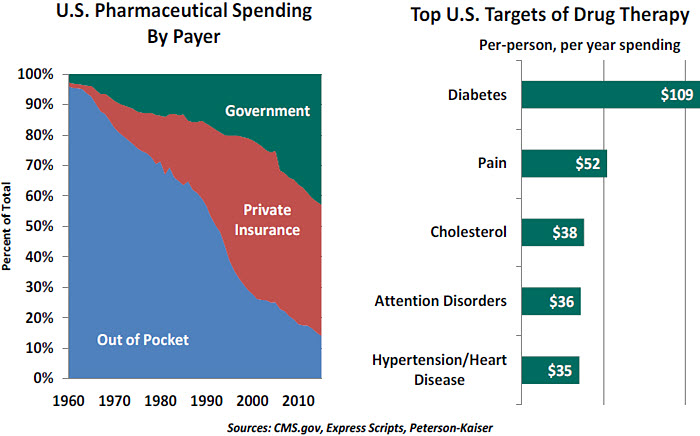

We wrote a piece last fall entitled “U.S. Health Care Needs Major Surgery.” It detailed a system where costs are spiraling while patient outcomes are falling behind those of other countries. A significant and growing fraction of those costs are paid by the Federal government.

Pharmaceutical costs represent about 10% of total U.S. health care expenditures, or about $325 billion each year. The Center for Medicare and Medicaid Services (CMS) projects that the value of prescriptions consumed will increase by 6.3% annually over the next decade, well above the expected rate of general inflation and household income growth. The gap between U.S. per-capita pharmaceutical spending and the comparable level in other countries will almost certainly get even wider than it is today.

Some of the escalation is due to the aging of the Baby Boom generation. But costs per patient per year for medication are also rising rapidly. Policy makers are anxious to bend this cost curve, an effort which has support from 64% of Democrats and 60% of Republicans.

There are potential remedies under consideration. Unfortunately, none of them will be easy to achieve.

- Pharmaceutical companies are introducing new medications to address ailments from hepatitis to cancer at an impressive rate. The good news is that these drugs offer hope and relief to patients suffering from these conditions. The bad news is that they often aren’t curative, while they often are very expensive. One particular medication costs nearly $100,000 for a 12-week course of treatment. These novel formulations account for a significant portion of the recent increase in drug costs.

Capping these costs, or limiting access to the drugs, would soften the blow. But pharmaceutical companies contend that an inability to recoup costs would discourage innovative research. (The United States does a substantial fraction of the world’s pharmaceutical development.) And it is difficult for societies to balance the costs and benefits of applying new treatments.

-

- To provide incentives for research, the U.S. government allows drug companies to offer new products for several years before generic alternatives can be marketed. Periodically, though, manufacturers try to preserve their window of exclusivity by making minor changes to the chemistry or purpose of the medicine. Making generics available earlier and more readily would reduce collective costs.

-

- Medicare Part D added a prescription drug benefit for participants just over 10 years ago. The program has proven popular, but the law prohibits the Federal government from negotiating lower drug prices for Medicare recipients. Essentially, the largest insurer in the country does not have the ability to leverage the buying power of a rapidly growing 40-million-patient pool. Removing this restriction could create considerable economies.

- Drugs taken to treat chronic conditions generate immense annual costs. The conditions they address, such as diabetes and heart disease, have both genetic and behavioral roots. Programs aimed at improving collective wellness (through diet and exercise) could reduce the need for these medications.

-

- The cost of a given drug is much lower in Canada than it is in the United States, because the Canadian government is a single payer. If U.S. patients could “re-import” medications, it would save a lot of money. But current law requires the Secretary of Health and Human Services (HHS) to guarantee that imported drugs would cause no risk

to public safety. HHS leadership has, to this point, been reluctant to offer such a certification.

While none of these steps will be easy to implement, all deserve evaluation. Unfortunately, the summer’s discussion of the ACA crowded out consideration of broader health care issues. Coverage and care for the roughly 20 million people covered by the ACA are very important. But a total of 330 million Americans are in need of better and more economical health care. Congressional debate needs to take much wider perspective on the topic.

Now that her injury has healed, my daughter has been making noise about re-piercing her ear. I have a very narrow view of that idea, and there will be no debate.

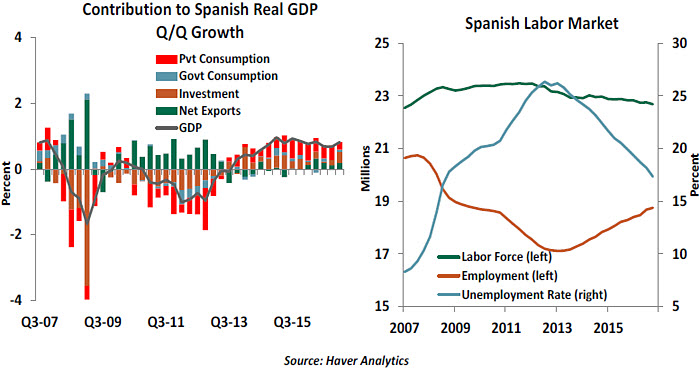

Spain, With Glass Half FullSpain typifies the turnaround of the European economy over the last year. After experiencing a severe double dip recession between 2008 and 2014, the Spanish economy has been growing at better than a 3% annual pace since 2015. Not only is the rate similar to the pre-crisis boom years, it is much higher than the rest of the eurozone.

The structure of this growth has been heartening, with pre-crisis credit- and construction-fueled growth replaced by something more sustainable: a combination of consumption, investment and exports. This has earned Spain plaudits from the International Monetary Fund (IMF), which noted last month both the broad-based nature of the economic recovery, and the ongoing repair of the financial sector.

What has driven this growth? Spain underwent a period of significant wage suppression, with real wages contracting at an average annual rate of 0.2% between 2012 and 2016. Lower production costs have translated into both higher exports and a substitution in Spanish consumption of domestically produced goods for imports. This gain in competitiveness has been accompanied by a reallocation of resources toward the export sector. All of this has altered Spain’s external profile, with the country’s current account balance going from a pre-crisis deficit of about 10% to a small surplus now.

Furthermore, the Spanish banking system has been much more forthcoming when it comes to implementing reforms. While vulnerabilities persist, the financial sector and private balance sheets are stronger than they were previously. Credit flow, while slow, has been improving.

The flipside is that the weight of post-crisis economic adjustment has fallen almost entirely on the shoulders of the Spanish workforce. Unemployment remains uncomfortably high at more than 17%. Among the unemployed, more than 40% have been out of work for two years or more. Even within those who have jobs, temporary workers account for about a quarter of the workforce. The labor market has a long way to go before qualifying as healthy.

Spanish real gross domestic product (GDP) has finally surpassed its mid-2008 level, but 10% fewer people are employed today. Structural reform (in the auto sector, among others) has improved productivity but slowed the pace of re-hiring. Hourly earnings remain below their levels of 10 years ago.

Public finances also remain a concern. Spanish public debt as a percentage of GDP went from 34% at the start of 2008 to close to 100% right now. This had more to do with the decline in GDP, and an associated decline in tax revenues, than a deliberately expansive fiscal policy stance. Fortunately, yields on 10-year Spanish government bonds have fallen from nearly 7% during the 2012 sovereign crisis to just 1.5% today.

Regardless, Spain has performed the best among the clutch of peripheral eurozone economies that were severely damaged between 2008 and 2012. The Spanish experience shows that economic recovery is possible with a combination of internal devaluation and structural reforms, even within the strict constraint of a monetary union. Continued economic

growth will be critical to sustain the improvement, though, and Spanish policy makers cannot

yet rest too easily.

As other countries in the periphery (such as Italy) contemplate their own economic strategies, the Spanish example provides a useful data point. It hasn’t been the easiest way forward, but there may be no other way.

Peril and PoiseAt any given moment, there are regional hot spots that threaten to become global conflagrations. Fortunately, these threats are most often contained, and when they do escalate, the world’s worst fears aren’t always realized.

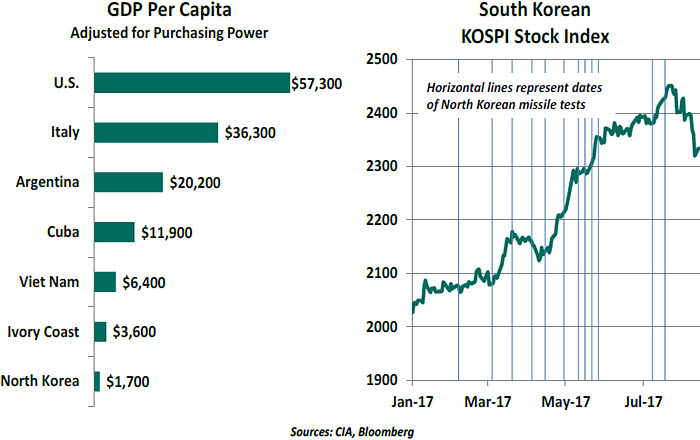

Current tensions between the United States and North Korea have risen to the top of many lists of top concerns. The roots of antipathy between the two are decades old; no peace treaty to end the Korean War was ever signed. Chinese sponsorship of the communist effort was, and is, extensive. But a relatively peaceful (if tense) status quo has been broken by the advancing nuclear weapons program directed by Kim Jong-un. The rhetoric passing back and forth between Washington and Pyongyang recently hasn’t helped calm the situation.

From an economic perspective, North Korea is a basket case. An estimated 40% of its citizens live in poverty; power shortages and drought plague its basic industries. In a bid for relevance, its leadership has placed all of its eggs in the basket of military aggression. Experts suspect that Kim’s gambit is to use his arsenal as leverage to gain economic concessions. A bad outcome cannot be ruled out, but remains unlikely. Reflecting this, South Korean equity prices have rallied this year amid a series of North Korean missile tests.

On a number of occasions over the past two decades, challenging events caused an immediate market retreat, only to see it regain traction in very short order. Our colleague Jim McDonald covers this topic well in his piece “Keep Calm and Carry On.”

One suspects that the limits of China’s support for North Korea are being tested. China’s aid in defusing the situation will be an element of broader discussions with the United States over intellectual property protection, steel tariffs and other touchy economic matters.

Leadership styles on both sides of the impasse are unconventional, and recent rhetoric is not helpful to the cause of compromise. World markets have performed so well, without much volatility, that they may be vulnerable to a correction. But history suggests that situations of this kind rarely create lasting economic consequences.

© Northern Trust

© Northern Trust

Read more commentaries by Northern Trust

Some of the escalation is due to the aging of the Baby Boom generation. But costs per patient per year for medication are also rising rapidly. Policy makers are anxious to bend this cost curve, an effort which has support from 64% of Democrats and 60% of Republicans.

Some of the escalation is due to the aging of the Baby Boom generation. But costs per patient per year for medication are also rising rapidly. Policy makers are anxious to bend this cost curve, an effort which has support from 64% of Democrats and 60% of Republicans.

Regardless, Spain has performed the best among the clutch of peripheral eurozone economies that were severely damaged between 2008 and 2012. The Spanish experience shows that economic recovery is possible with a combination of internal devaluation and structural reforms, even within the strict constraint of a monetary union. Continued economic

Regardless, Spain has performed the best among the clutch of peripheral eurozone economies that were severely damaged between 2008 and 2012. The Spanish experience shows that economic recovery is possible with a combination of internal devaluation and structural reforms, even within the strict constraint of a monetary union. Continued economic