In the world A sharp rise in geopolitical tensions and continued political turmoil characterized the month of August. North Korea conducted a series of missile tests before threatening the U.S. territory of Guam and a nearby U.S. air base. President Trump then threatened the reclusive nation with “fire and fury like the world has never seen,” prompting Pyongyang to respond with one of its most provocative actions: flying a missile directly over Japan’s northern island of Hokkaido. In a rare sign of global solidarity, the UN Security Council unanimously passed a resolution imposing new sanctions on North Korea, targeting the nation’s primary exports of coal, iron, lead and seafood. Separately, the U.S. placed fresh sanctions on Russia and Iran, and froze the assets of Venezuelan President Nicolás Maduro amid the country’s growing political unrest. In the U.S., fresh controversies hampered the Trump administration’s policy agenda further: President Trump’s approval ratings dipped to new lows following criticism over his response to a white supremacist rally in Virginia; chief strategist Steve Bannon became the latest departure from the administration; and a long list of CEOs resigned from the business advisory council, which subsequently disbanded.

Global growth data surprised to the upside, but inflation pressures remained subdued. U.S. growth measures were more upbeat than previously reported: The latest estimate for GDP growth in Q2 showed the economy expanding at a 3.0% annualized pace, better than the previous estimate of 2.6% and the strongest growth in two years as household spending and investment improved. The U.S. labor market also gained more than expected, with 237,000 jobs added. However, the lack of inflationary pressures was notable: Wage growth remained muted and core CPI disappointed. The dichotomy of a strong economy and subdued inflation was also apparent in Japan. Preliminary April-June GDP registered a 4.0% annualized pace, well above the market’s expectation of 2.5%, as strong private spending propelled Japan to its sixth straight quarter of growth and the longest expansion streak since 2006. But the region’s benchmark price gauge rose only 0.5% year-over-year for July, well below the Bank of Japan’s 2% inflation target. While central bankers gathered in Jackson Hole for the annual Economic Policy Symposium, Federal Reserve Chair Janet Yellen and European Central Bank (ECB) President Mario Draghi steered clear of immediate policy issues, instead opting to discuss financial regulation and free trade.

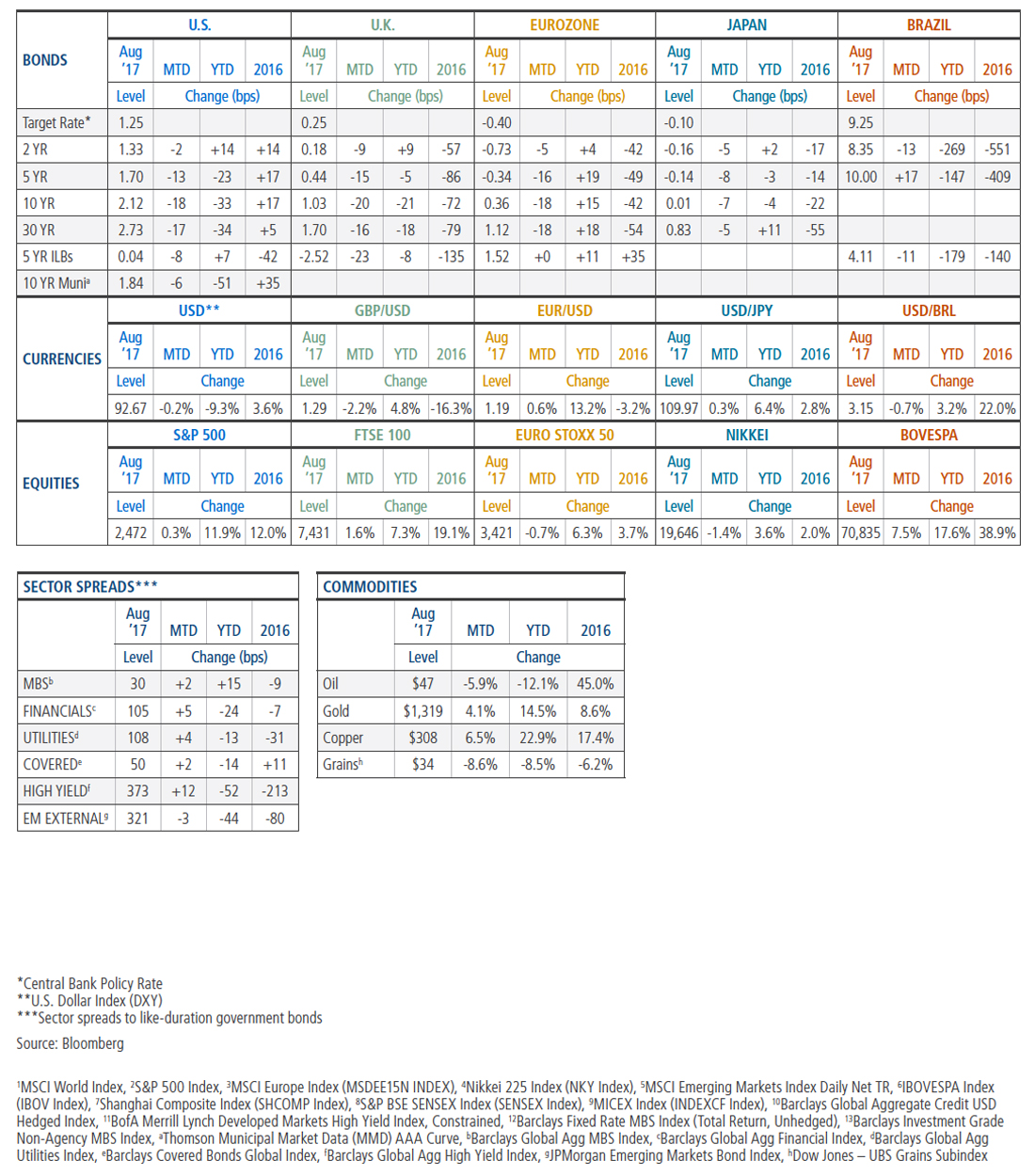

Markets appeared to roll with the punches despite increasing geopolitical volatility. Concern over rising global tensions and political dysfunction in the U.S. seeped into the markets. The S&P 500 fell 1.8% mid-month, and the VIX – a widely cited volatility measure – touched its highest level of the year. Still, markets weren’t on the ropes long: The Dow Jones Industrial Average managed to reach new all-time highs, and the S&P 500 rallied to end the month in positive territory on the tails of strong Q2 earnings. In Europe, equity markets were less optimistic and tumbled for the third month in a row. ECB President Draghi opted not to acknowledge the recent strength in the euro at the central bankers’ gathering in Jackson Hole, supporting the perception that a potential shift toward less accommodation was underway. The euro surged 0.6% on Draghi’s lack of comment and as North Korea jitters prompted investors into “safe-haven” currencies, including the Japanese yen and Swiss franc. Global yields also rallied amid the heightened uncertainty; the U.S. 10-year yield fell 18 basis points (bps) to 2.12%, putting it 33 bps lower on the year, and the yield curve flattened as the spread between 10-year and two-year yields narrowed to its lowest point this year.

Growth Shines Through U.S. real gross domestic product (GDP) expanded at a 3.0% seasonally adjusted annual rate in the second quarter of 2017, eclipsing the previous estimate of 2.6%. The higher-than-expected growth rate marked the strongest expansion in over two years, and was supported by robust consumer spending and private business investment. Consumer confidence in July increased to its second highest level since December 2000, suggesting that consumption may remain healthy into the third quarter. And labor market strength continues to provide additional support to the economy: Employers added 237,000 workers to their payrolls in July, far surpassing estimates of 185,000.

In the markets

Euro Eclipses the U.S. Dollar Since touching a decade low at $1.04 on 20 December 2016, the euro has staged an impressive rally in 2017, appreciating over 14% against the U.S. dollar. While the general weakness in the dollar year-to-date is partly to blame, much of the euro’s strength stems from the expectation that the European Central Bank (ECB) will soon scale back its quantitative easing program. In fact, an especially large move occurred after ECB President Mario Draghi chose not to address the euro’s recent strength during his speech at Jackson Hole. However, the stronger euro may complicate the ECB’s plan by putting downward pressure on import prices and in turn eurozone inflation, which is already well below the central bank’s target of just under 2.0%.

EQUITIES Developed market stocks1 returned 0.1% as escalating tension between the U.S. and North Korea spurred a flight to quality overall. In the U.S.2, continued strength in the domestic economy boosted stocks to a 0.3% return after a weak start to the month. European stocks3 slumped 0.8%, marking their third consecutive month of decline; European Central Bank (ECB) President Mario Draghi failed to address recent strength in the euro, which may hamper future corporate profits. Japanese equities4 fell 1.3% amid North Korea jitters.

In emerging markets5, stocks benefitted from relatively stable global market conditions and a strong technical backdrop to return 2.2%. In Brazil6, stocks rallied 7.5% after the government announced plans to privatize state assets, including the country’s largest utility, Centrais Elétricas Brasileira (Eletrobrás). Chinese equities7 returned 2.8% on investor optimism over strong corporate earnings. Rising tension with North Korea weighed on India’s markets8, and stocks fell 2.3%. Russian stocks9 notched their best month in 2017, returning 5.3% amid strong corporate profits and expectations of an interest rate cut.

DEVELOPED MARKET DEBT Heightened geopolitical tensions with North Korea, a flurry of trade sanctions from the U.S. and continued political turmoil in the U.S. drove developed market bond yields generally lower last month. More staff departures in the Trump administration as well as looming deadlines for government funding and the debt ceiling weighed on investor sentiment. The U.S. 10-year Treasury yield ended the month at 2.12%, nearly 20 basis points (bps) lower on the month and 33 bps lower for the year as the yield curve flattened. In the eurozone, the German bund 10-year rate fell 18 bps, and yields in Japan also moved lower.

INFLATION-LINKED DEBT Global inflation-linked bonds (ILBs) advanced across most major markets in August. Real interest rates generally declined due to the risk-off sentiment triggered by tension between North Korea and the U.S. and lower expectations for tightening from major central banks. Within the U.S. TIPS market, breakeven inflation rates generally fell after the Consumer Price Index proved weaker-than-expected for the fifth month in a row. U.K. index-linked gilts posted strong gains and significantly outpaced comparable nominal gilts. The Bank of England left rates unchanged and downgraded its growth forecasts in its August quarterly inflation report, which pushed gilt yields lower. U.K. breakeven inflation rates steadily rose on the back of currency weakness, a higher-than-expected Retail Price Index and persistent demand from pension investors.

CREDIT Global investment grade credit10 spreads widened 5 bps, underperforming like-duration government bonds by -0.33%, due in part to higher-than-average supply in the U.S. Recent spread volatility in spite of persistent strong demand for newly issued investment grade corporate bonds indicated that spreads may be reaching fair value; yet inflows into high-grade retail funds and ETFs suggested that investors’ appetite for income remained strong.

Global high yield prices11 ended the month slightly in the black. Prices had softened earlier on tensions with North Korea, terrorist attacks in Barcelona and fallout from a contentious press conference with U.S. President Donald Trump after a protest turned violent in Charlottesville. High yield spreads, however, widened 25 bps for the month, with yields about 10 bps higher and five- and 10-year government rates about 15 bps lower.

EMERGING MARKET DEBT Returns for emerging market (EM) debt were positive in August: Spread tightening drove performance in external debt, and falling index yields drove performance in local currency debt. Argentine hard currency debt was a notable outperformer, as President Mauricio Macri’s Propuesta Republicana party (PRO) surpassed expectations in legislative primary elections. The primary results could pave the way for a strong performance by the PRO in the October general elections, ultimately improving the prospects for Macri to successfully enact his reform agenda. South African local debt also posted strong performance: Inflation expectations fell more than expected for the second straight month, outstripping the political noise surrounding embattled President Jacob Zuma. Fund flows into emerging market debt continued to be robust, providing an additional tailwind for performance.

MORTGAGE-BACKED SECURITIES Agency MBS12 returned 0.73% and underperformed like-duration Treasuries by 12 bps, as the flattening in the U.S. yield curve weighed on higher coupon MBS despite relatively low volatility. Overall, Ginnie Mae MBS underperformed conventional MBS, 30-year MBS marginally outperformed 15-year MBS, and lower-coupon conventional MBS outperformed higher-coupon conventional MBS. Investors firmly anticipated that the Federal Reserve’s balance sheet reduction would be announced in September, but the pace of this tapering was expected to be “gradual and predictable,” as the Fed suggested in May. Gross MBS issuance increased 7% from July, while a gradual summer slowdown in housing turnover caused prepayment speeds to fall 8%. Non-agency MBS prices rose moderately, and spreads relative to swap rates tightened amid continued strength in the U.S. housing market. Non-agency commercial MBS13 returned 1.17% and outperformed like-duration Treasuries by 19 bps.

MUNICIPAL BONDS Municipal bonds posted positive returns in August, with the Bloomberg Barclays Municipal Bond Index returning 0.76%. Muni rates moved lower across the yield curve but underperformed “safe-haven” Treasuries amid rising geopolitical tensions. August issuance at $29 billion was nearly 40% lower year-over-year and was outpaced by the dollar value of maturing bonds for the third month in a row; this negative net supply has been a favorable technical tailwind through the summer. Demand remained firm; inflows to municipal bond mutual funds were nearly $2 billion during the month, bringing year-to-date inflows to $8.9

CURRENCIES Geopolitics and central banks influenced most currency moves in August. The yen, often viewed as a “safe-haven” currency, fluctuated as geopolitical tension oscillated throughout the month. The U.S. dollar was relatively volatile but ultimately ended the month flat, supported by stronger-than-expected economic data. Central bankers’ comments (or lack thereof) motivated some currency moves: The euro continued to rally as the ECB president notably did not comment on recent euro strength at the annual economic symposium in Jackson Hole. Statements from officials at the central banks of Australia and New Zealand regarding the potential damage from domestic currency strength on their respective economies pushed the Australian and New Zealand dollars down. The British pound fell 2.2% over the month in response to the BoE keeping rates on hold and downgrading its growth forecasts.

COMMODITIES Varied performance in individual commodity markets left the sector as a whole roughly flat for the month. In the oil markets, Brent’s early losses were offset by a late-month recovery in prices, which started to reflect the tightening in global inventories over the year. WTI, however, noticeably underperformed Brent; the arrival of Hurricane Harvey forced the shutdown of many Gulf Coast refineries and created the risk of an inventory buildup at Cushing. Products (including gasoline) outperformed crude oil as a result of the refinery slowdowns and closures across the region. The agriculture sector suffered a broad-based sell-off amid generally supportive weather during an important stage in the crop development cycle. Industrial metals generally rose on the continued expansion in Chinese manufacturing and a generally positive outlook for global growth. In precious metals, gold gained partly due to “safe-haven” demand.

FOOTNOTES:1MSCI World Index, 2S&P 500 Index, 3MSCI Europe Index (MSDEE15N INDEX), 4Nikkei 225 Index (NKY Index), 5MSCI Emerging Markets Index Daily Net TR, 6IBOVESPA Index (IBOV Index), 7Shanghai Composite Index (SHCOMP Index), 8S&P BSE SENSEX Index (SENSEX Index), 9MICEX Index (INDEXCF Index), 10Barclays Global Aggregate Credit USD Hedged Index, 11BofA Merrill Lynch Developed Markets High Yield Index, Constrained, 12Barclays Fixed Rate MBS Index (Total Return, Unhedged), 13Barclays Investment Grade Non-Agency MBS Index

Outlook**

Based on PIMCO’s cyclical outlook from March 2017 and subsequent updates (May 2017)

PIMCO expects the eight-year-old global economic expansion will continue to strengthen and broaden for the remainder of 2017, driving global GDP growth to 2.75%–3.25% from 2.6% in 2016 and boosting CPI inflation to 2.0%–2.5%. Our outlook reflects several positive factors: generally supportive fiscal policies (or expectations of them) in most developed market economies, easier financial conditions since the start of the year, positive animal spirits as indicated by consumer and business confidence data, and a rebound in global trade.

In the U.S., we see growth above-trend at 2%‒2.5% in 2017 as business investment recovers, particularly in the energy sector, and consumer spending is supported by a further decline in unemployment, high consumer confidence and expectations of personal income tax cuts ahead. We forecast core inflation to hover sideways this year at 1.75%–2.25%, owing to some softer trends of late. With policy normalization under way, we expect the Fed to embark on reducing its balance sheet by gradually tapering its reinvestments in a predictable and transparent manner.

For the eurozone, we expect growth will be in a range of 1.75%‒2.25% in 2017, revised higher from our forecast in March to reflect the stronger momentum this year. While political uncertainty remains ahead of elections in Germany and potentially Italy, the likelihood of disruptive populist outcomes has diminished. In addition, both fiscal and monetary policy are expansionary, and the recovery in global trade growth supports exports and investment. We anticipate core inflation remaining well short of the European Central Bank’s (ECB) “below but close to 2%” objective, but the solid growth momentum will likely allow the ECB to taper and eventually end its purchases next year.

In the U.K., we expect growth to be in the range of 1.5%–2.0%despite Brexit, reflecting robust momentum, higher government spending and a positive contribution from net trade on the back of the 15% drop in the pound in 2016. We forecast CPI inflation to exceed the Bank of England’s 2% target but expect the Bank to leave policy rates unchanged this year.

Japan’s strong private demand and export growth should support GDP growth of 1.0%‒1.5% in 2017 while inflation remains significantly below the 2% target. The Bank of Japan is likely to keep targeting the overnight rate at –0.1% and the 10-year bond yield at 0% and thus continue its standing invitation to the government to engage in additional fiscal expansion, which we expect to happen later this year.

China’s public sector credit bubble and private sector capital outflows will likely remain under control, and we expect growth in a 6.25%‒6.75% range in 2017 as policymakers prioritize financial stability over economic stimulus ahead of the 19th National Party Congress in the fourth quarter. Any trade war with the U.S. will likely involve words rather than action, and we expect the yuan to depreciate gradually against the U.S. dollar.

In emerging markets, we expect moderate growth in Brazil and Russia in 2017 as they emerge from recession. With inflation dropping, both countries’ central banks have room to cut rates further. We expect Mexico’s growth to be 2.75%-3.25% with the potential for Banxico to adopt an easier policy stance if inflationary pressures abate.

** Note that PIMCO’s next cyclical forum is in September 2017 and all published forecasts for growth and inflation will be re-evaluated then.

In sight

China To Line Up Leadership On October 18, China will begin its 19th National Congress of the Communist Party. The Congress – held once every five years – serves as the selection ground for the party’s new leaders who will likely become the most powerful government officials in the one-party state. President Xi Jinping is widely expected not only to retain his role as head of the party, but also to succeed in filling the ranks of the Politburo and its powerful seven-member Standing Committee with his deputies. This would strengthen his already firm grasp on power and solidify his position as China’s “core” leader for the foreseeable future. In the lead-up to the Congress, Chinese policymakers have sought to prioritize economic stability over growth in an effort to avoid adverse market events that could roil Xi’s political strategy. As he takes on more centralized control, Xi will be held increasingly responsible for the state of China’s economy. As a result, policymakers will likely maintain the current mix of relatively tight monetary policy and coordinated regulation in the months immediately following the Congress.

Appendix

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominatedand/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax; a strategy concentrating in a single or limited number of states is subject to greater risk of adverse economic conditions and regulatory changes. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation- Protected Securities (TIPS) are ILBs issued by the U.S. government. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. It is not possible to invest directly in an unmanaged index.