Last March, we wrote a piece entitled “Equity Repricing Under a New Administration: A Tail Risk Scenario.” We posited that the proposed pro-growth tax and spending policies of the Trump administration, thrust onto an economy nearing full capacity, could lead to a general rise in the inflation rate and ultimately the real rate of interest.

We hypothesized that such a scenario could result in a substantial equity sell-off, as the increase in the real interest rate would exceed the expected growth rate of earnings.

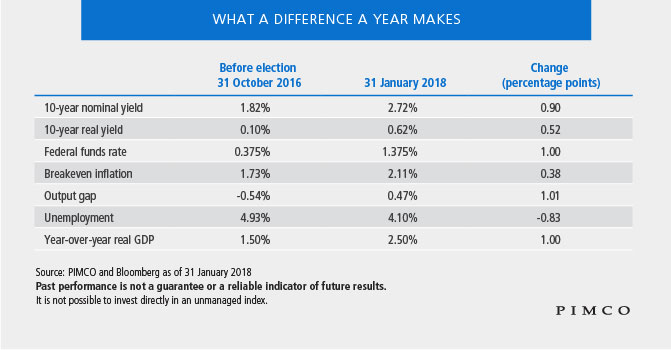

To be sure, neither an eye-popping uptick in inflation nor a dire downturn in equities is PIMCO’s base case. Nor is the recent correction at all comparable to the tail event scenario we outlined.

Still, in addition to a nearly 33% jump in the S&P 500, many other elements of our scenario have fallen into place.

Late-cycle stimulus

In our view, the recent volatility in financial markets results from a toxic cocktail of higher real yields, increased inflationary expectations, and significant short volatility positions, both explicit and implicit. Additionally, the economy is getting a large dose of late-cycle fiscal stimulus to the tune of $1.5 trillion with the Tax Cuts and Jobs Act, passed in late 2017. Furthermore, February’s budget deal increased spending over the statutory budget caps by about $300 billion over two years.

In this context, it may be difficult for an economy operating close to full capacity to avoid significant inflationary pressures. This, in turn, could force the central bank’s hand to raise rates at a faster pace than markets may be anticipating.

A factor that is central to our tail scenario is the real duration of equity markets, which has been pushed up to historically high levels due to declining dividend yields. As a result, should real yields increase faster than the growth rate of earnings, this could portend a major equity correction.

Read our in-depth analysis: “Equity Repricing Under a New Administration: A Tail Risk Scenario, which is intended for professional investors only.

Jamil Baz is a managing director and co-head of PIMCO’s client solutions and analytics team, and Steve Sapra is an executive vice president in the Newport Beach office and head of client solutions and analytics for North America and Asia ex Japan.

© PIMCO

© PIMCO

Read more commentaries by PIMCO