The period since the financial crisis has been unprecedented in both the duration of the bull market but also the extreme low levels of volatility. As John Authers of the Financial Times recently pointed out, 2017 was the ‘most serenely positive year for world markets in history’.

The MSCI World index delivered a positive return every month of the year for the first time ever, while the MSCI EAFE index gained ground in ten out twelve months and returned -0.18% and -0.04% in the other two, for a compounded annual return of +25.0% in US dollars.

Chart 1: MSCI EAFE MONTHLY RETURNS (%) 2017

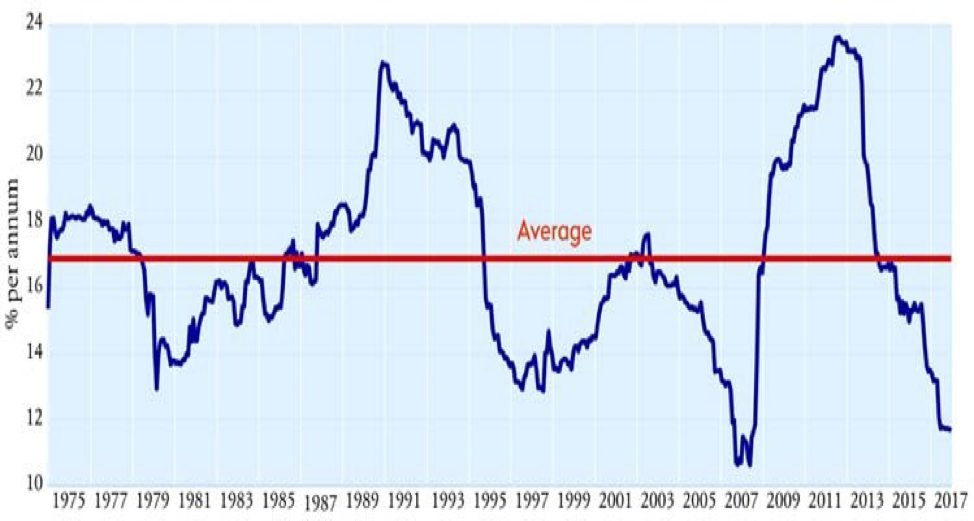

Chart 2: MSCI EAFE VOLATILITY- ROLLING 5-YEAR: 1975-2017

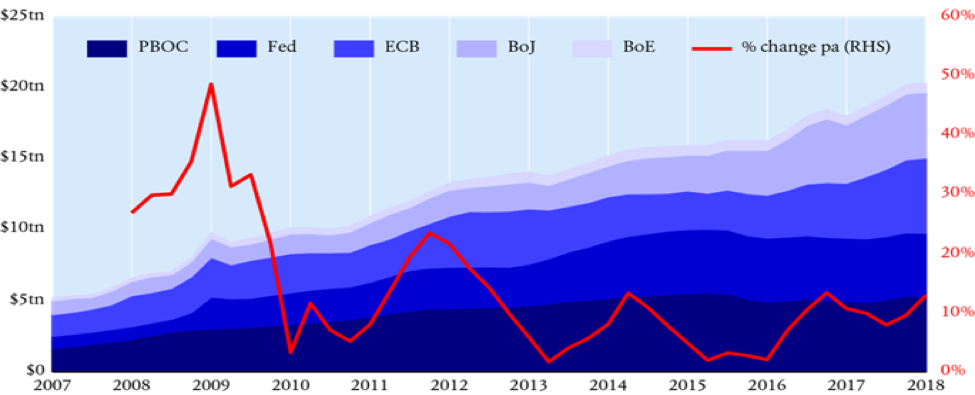

As chart 2 shows, central bank balance sheets have expanded to three times their size before the global financial crisis and are in aggregate still anticipated to expand in 2018. It is probable that they will contract at some point in the coming years and it is unclear what the consequences will be. We do however envisage that even a gradual shift to a more normal interest rate environment will over time lead to rising volatility and fairer pricing of risk.

We would argue that both the elongated period of market appreciation and the low volatility are, to a large extent, a result of the ultra-loose monetary policies that have been pursued globally. This sustained period of negative real interest rates has undoubtedly created many distortions, not least in equity markets.

We are now in the early stages of these policies being unwound with the U.S. Federal Reserve already having terminated its purchases of government bonds and starting to reduce the size of its balance sheet and the ECB likely to follow suit at some point in 2018. Even so we are still a long way from interest rates being at a level commensurate with economic activity.

Chart 3: CENTRAL BANK BALANCE SHEETS: 2007-2017

ACTIVE MANAGERS STRUGGLE TO DIFFERENTIATE THEMSELVES IN BECALMED MARKETS

Against this backdrop of continuous market appreciation and low volatility it is clear that there has been an increased focus in the investment community on passive and also ‘smart’ beta strategies. In contrast, more traditional active investment strategies have struggled to make their case. This should not be surprising. Achieving attractive absolute returns from passive investing is easy when markets just continue to gradually move higher.

In contrast, active managers often find this kind of market environment more challenging, tending to add more value in periods of either greater volatility or market declines. As such, in justifying a passive investment at this stage of the market cycle, there is an implicit assumption that the current benign environment will continue.

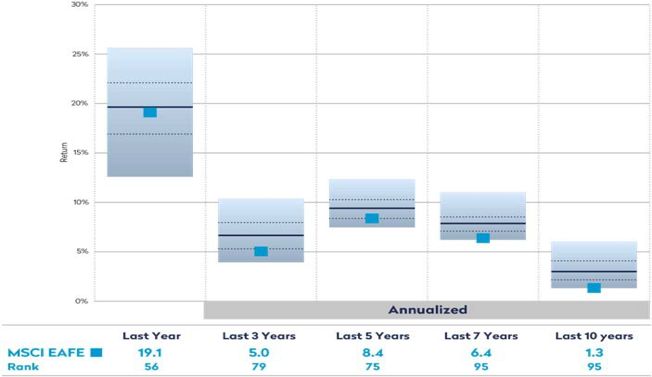

A recent survey of the investment universe offered us compelling evidence that active management is able to add value over a full market cycle in international equity markets. The median manager in the Intersec universe has delivered 150bps per annum of excess return over 7 and 10 years (gross of fees), which translates to meaningful outperformance of the MSCI EAFE index after fees. Furthermore, well over three-quarters of the universe has delivered above benchmark returns over these time periods.

While we accept that there are always going to be challenges in selecting managers with the capabilities to outperform a benchmark on a forward-looking basis, with such a large portion of the universe adding value over a sufficiently long-time horizon, in actual fact the chances of selecting an outperforming manager are high.

Chart 3: DISPERSION OF RETURNS WITHIN INTERNATIONAL EQUITY UNIVERSE

Source: Intersec

As with many industries, probably the most dramatic change in the investment world in the last five to ten years has been technological development. This has supported the growth in quantitative and high-frequency strategies that trade on multiple minute pricing discrepancies, as well as indexing, tracker, ETF and ‘smart’ beta products that generally rely on huge computer processing power to process large amounts of data quickly.

The ever-widening range of strategies available to investors creates an interesting competitive challenge to more traditional asset managers relying on in-depth fundamental analysis, although we see no reason that the two cannot co-exist.

These newer, technology centric products do allow investors to decompose risk and pick and choose the exposures they wish to take more carefully than in the past, but in reality, these strategies should be evaluated in much the same way as traditional active strategies as they still involve the discretion of an investment manager in constructing a portfolio of exposures, even if it is then implemented systematically.

Also, use of such strategies still requires an asset allocation decision to be made and there is no guarantee that this will deliver returns in excess of a broad market benchmark on a forward-looking basis. Historic simulated models for these strategies are often very different to the forward-looking returns actually achieved over a sustained period. As discussed extensively by Research Affiliates1, one of the leaders in the field, it is questionable whether the sources of excess return that many of these products are aiming to tap will be sustainable in the medium to long term.

While it is never easy to call market peaks, we believe that most evidence certainly indicates that at current valuations we may be much closer to a market peak than a trough. A passive strategy does provide certainty of the relative return outcome in relation to a benchmark, but we believe this is often not going to be the most favorable absolute return outcome.

Source: MSCI, Mondrian Investment Partners.

1 E.g. How Can “Smart Beta” Go Horribly Wrong? Rob Arnott et al, Research Affiliates February 2016

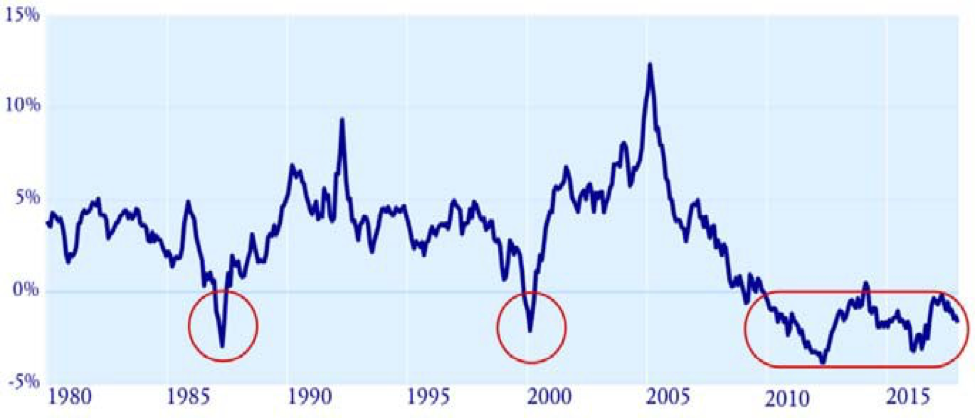

CHART 5. MSCI EAFE VALUE ROLLING 5-YEAR ANNUALIZED RETURN RELATIVE TO MSCI EAFE GROWTH: 1980-2017

With indexation, when you guarantee the market return in a rising market, you also guarantee it in a market correction. Conversely, a market correction is the environment where Mondrian portfolios have historically added most value through downside protection characteristics provided by the focus on dividends and a thorough analysis of worst case scenarios.

OPPORTUNITIES FOR DISCIPLINED ACTIVE MANAGERS IN INTERNATIONAL EQUITY

In summary, we believe that the evidence continues to point towards there being ample mispricing opportunities in international markets to justify an active investment strategy. The multi-dimensional nature of the opportunity set - the wide range of markets, currencies and stocks, as well as the diverse investor base with diverging objectives – could make for a rich opportunity set in the international equity universe with great potential for securities to be mispriced from a long-term perspective.

The intrinsic value of an equity security arises from the long-term stream of income it is expected to generate for an investor. Even after allowing for the deleterious effect of inflation on the present value of future income, more than 80% of the value of almost all equity securities comes from income anticipated to be received more than three years in the future.

At any point in time, the current market price for a security reflects a weighted assessment of a range of possible future outcomes made by all market participants. As more and more market participants focus on shorter-term pricing anomalies, or in the case of index funds do not care about pricing anomalies at all, so this implies a relatively smaller proportion of investors trying to value this long-term income stream and thereby set a “fair market price”.

Against this backdrop, we believe that there has been no fundamental change in the potential for securities to be mispriced over a medium to long time horizon, whether this is due to a misunderstanding of the business outlook or of the risk associated with a given investment, or by simply not allocating the time or discipline to understanding longer-term issues.

Such analysis requires a detailed understanding of the idiosyncrasies of not only a company but also the industry and geopolitical environment in which they operate. That can come only with a thorough and disciplined consideration of a range of different information sources.

Mondrian Investment Partners Limited is a London based firm with over $60 billion in assets under management as of December 31, 2017. We are an employee owned business with over 80 partners. Our client base is mainly institutional and global in nature.

Mondrian Investment Partners Limited is Authorised and Regulated by the Financial Conduct Authority.

© Mondrian Investment Partners

______________________________________________________________________________

Read more commentaries by Mondrian Investment Partners