For February 2018, the SPDR S&P 500 ETF (SPY), which tracks the S&P 500 Index had $18 billion in net outflows. It was the biggest outflow in dollar terms since the financial crisis.

Investor complacency may be a root cause.

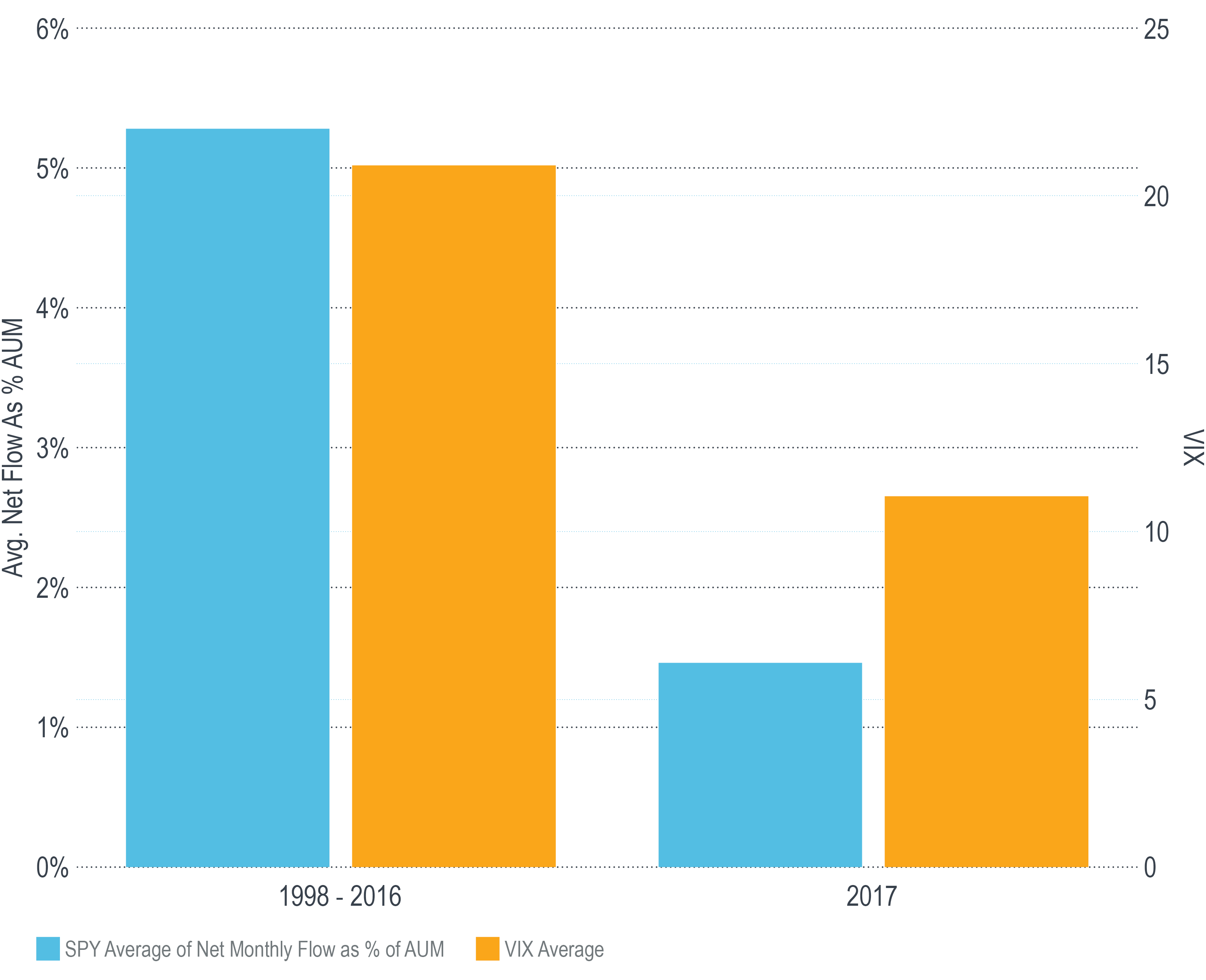

From 1998 to 2016, the average monthly net flow as percentage of SPY’s AUM was 5.28% compared to 1.46% in 2017. Passive investing may have become a winning strategy last year because of the financial environment:

- Low interest rates: Historically low bond yields gave greater appeal to equities.

- Low volatility: Calm markets gave investors greater confidence to passively invest in the market as a whole rather than actively managing their exposure to risk.

This year, the Fed is expected to raise its overnight rate three or even four times, potentially pushing the longer end of the curve higher. In the absence of EPS growth, higher discount rates will put downward pressure on valuations, leaving higher-yielding bonds all the more attractive.

If February did indeed mark a secular shift back to higher volatility, investors may do well to invest actively and be more vigilant in managing portfolio risk.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.

For financial professional use only.