Many investors who thought worrying about inflation was “so 20th century” may now be seeing reasons to reconsider: The business cycle in the U.S. is mature, output gaps have closed, trade frictions are mounting and populism is on the rise. While PIMCO’s base case is for U.S. inflation to continue climbing toward the central bank target, the risk of an overshoot has grown, and inflation is picking up in several other key markets, such as China, Japan and India.

We are transitioning from an environment where deflation posed a significant risk and rising inflation was good for markets, to one where low and stable inflation is preferable (and an upside surprise would not be welcome).

In such an environment, commodities and other real assets tend to shine and may once again play an important diversifying role for investors.

Is it time to reconsider commodity allocations?

We see some compelling reasons why, after a challenging few years, commodities could play a bigger role in investor portfolios in 2018 and beyond.

First, commodities historically have tended to do well in the later stages of a business cycle. Unlike equities, which often anticipate changes in growth and earnings, commodities are more rooted in the present and tend to perform well once capacity constraints are already developing.

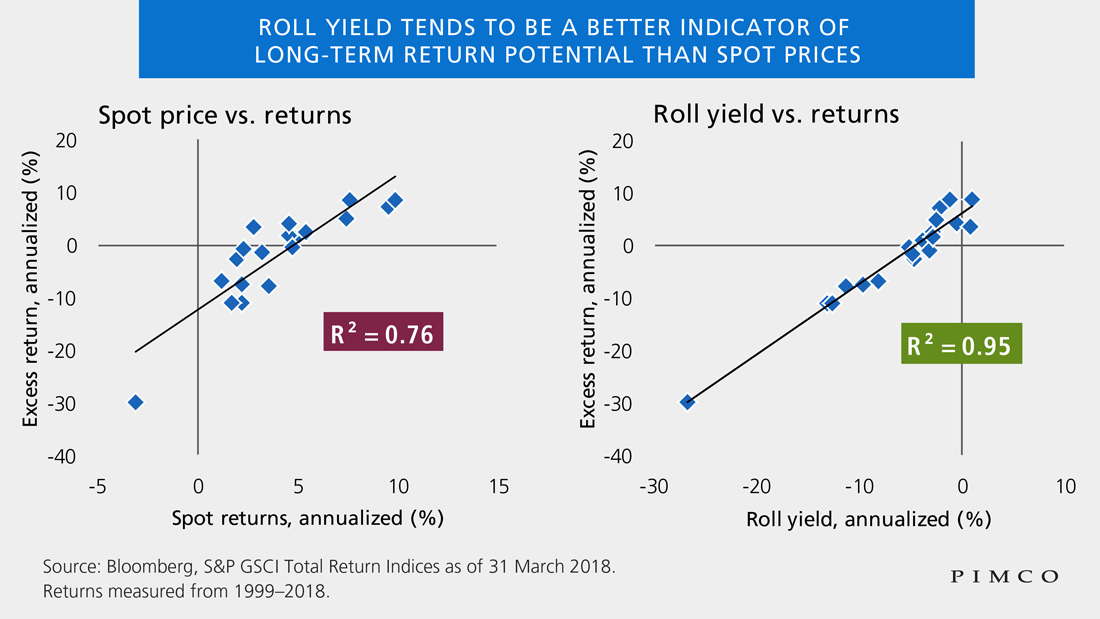

Second, the crude oil futures curve today is decisively in backwardation, which generally leads to positive “roll yield” (derived from rolling a higher-priced short-term contract into a lower-priced longer-term contract). Indeed, roll yields across major commodity indexes are positive (or nearly so), and a number of studies show roll yield on futures contracts may be the best predictor of long-term commodity returns (see chart below). Moreover, crude oil returns tend to be positive even in the short term when the curve is in backwardation.

In this situation, after adding in the yield or carry from the underlying collateral portfolios, investors may be rewarded for holding an asset that diversifies from bond and equity market risk. And we note that investors are not confined to major published commodity indexes. Various “smart beta” commodities strategies exist that are designed to increase actual and estimated return potential over published conventional cap-weighted indexes.