Rhyme or Reason

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsChange can be disconcerting, and if there’s one thing we can probably all agree on, it’s that change has come to the investment markets this year. Familiar calm markets characterized by steady gains month after month have been replaced by markets that are jolted by violent moves up and down – sometimes within the same day. For all of 2017 there were eight days with moves of more than 1% up or down in the S&P 500 Index. During just the first quarter of 2018 there have been twenty-three. In 2018 there have been six days with moves of more than 2%, five down and one up; in 2017 there were none.

Gyrations in stock prices may not be a top of the mind concern for many people, given that a recent Gallup poll1 found that only 54% of Americans own any stocks – either directly or indirectly. Still, if you’re reading this, it’s probably safe to assume that the prospects for investment returns are important to you.

As investment managers, we are often asked our opinion about what the future holds for the economy and investments. While that’s the question we’re asked, we suspect what people really want to know is what the future holds for them, and for their plans to meet their important financial needs and goals.

Some goals require the accumulation of capital, some require a reliable supply of current income, and many require a measure of both. For some goals, the important time frame is right now. There’s a large expense looming – perhaps the purchase of a home, or the start of college education expenses. Some goals may be 5 to 10 years down the road, and some may still be decades away. Some will require lump sum outlays, and some – like retirement – may involve outflows that stretch over 20 years or more. (According to the U.S. Department of Health and Human Services, the average life expectancy at age 65 is 20.6 years for females and 18.0 years for males.2)

As much as we would like to believe otherwise, none of us know exactly how the future will unfold – although we all may have our predictions, forecasts, estimates, and guesses. After all, we still have to make our plans based on something. But as Mark Twain once quipped, “The future doesn’t repeat itself. At best, it rhymes.” Still if you’re trying to plan for your future, you may want to consider what the past has to tell you.

We understand that history can’t give us a precise timetable about what’s going to happen, or when. We do believe, however that the lessons of history can teach us about what can happen, and how we should think about the kinds of decisions we are making about our actions today.

Let’s listen in on what history is whispering to investors with varying needs and time horizons about the economy, the stock market, and bonds.

The Economy

The National Bureau of Economic Research (NBER) is charged with determining whether the U.S. economy is in an expansion or recession. A recession is defined as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales”. The Great Depression is referenced in NBER reports, but there’s no definition of what constitutes a depression. (A rather grim quip says that a recession is when your neighbors lose their jobs – and a depression is when you lose yours.)

According to the NBER, since 1929 the U.S. economy has been through 14 recessions (including the Great Depression). This is an average of one recession about every 5 ¾ years. From the time a recession begins until it reaches its lowest point has averaged just over 13 months. It has taken an average of 57 months of recovery, or nearly 5 years, for the economy to climb back to a new peak.

Recessions tend to be hard on home prices, consumer spending, company profits, stock prices, job security, and

paychecks. Lending standards also tend to become stricter as loan defaults rise, making it harder to qualify for credit and mortgages.

The most recent “Great Recession” ended in June 2009. Many folks still seem to be clawing back from that decline. Based on past expansions, the current recovery should have ended sometime back in 2015, so the current recovery is breaking records for longevity, if not for strength. They say records are made to be broken, so the expansion could continue indefinitely, but history suggests that one of these days it will definitely end.

Someone making plans for five years from now may want to figure out how they are going to keep those plans on track while going through the next recession. Someone planning for goals 15 to 20 years out may want to plan on getting through two or three.

We constantly monitor a wide variety of economic data as part of our investment process in an effort to assess how the portfolios under our management should respond as the economy cycles through expansions and recessions.

The Stock Market

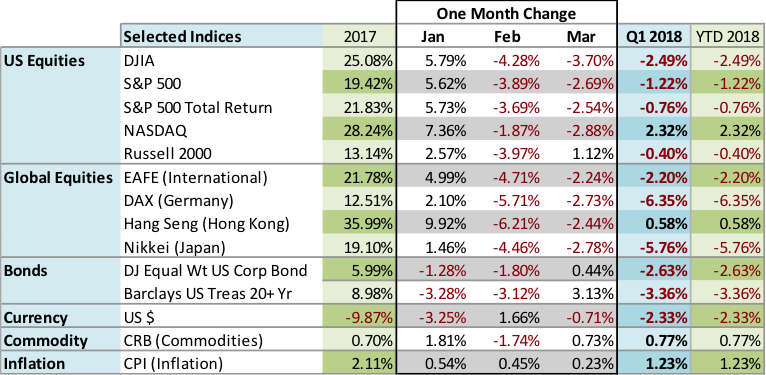

On March 9, 2009, the S&P 500 Index closed at 676.53. On January 26 of this year, it closed at an all-time high of 2872.87 – a gain of nearly 325%, not including dividends. By February 8, just 9 trading days later, it had fallen by more than 10% to 2581.

Shocking? Maybe, for anyone accustomed to the kind of calm, steady climb stocks had been experiencing over the last few years. But history suggests declines in stock indices of 10% or more are part of the price for holding stocks as markets fall. Since January 2000 there have been at least 15 instances of the S&P 500 Index dropping 10% or more from its previous high – an average of about once every 15 months. We can also find 5 declines of more than 20% over that same period – an average of once every 3.8 years. There have even been two cases of declines in the neighborhood of 50%: -49.15% from March 24, 2000 to October 9, 2002, and a whopping -56.78% from October 9, 2007 to March 9, 2009. How many plans will hold up through a loss of around half of the nest egg every 9 ½ years or so?

Of course, history also tells us that the market has always come back from its big declines, but it can take a while. After the 2000 – 2002 decline attributed to the bursting of the “dot com” bubble, it took the S&P 500 Index more than 4 ½ years to get back to where it started. It took just over 4 years for the S&P 500 to recover from the 2007 – 2009 crash precipitated by the collapse of the housing market. Spending year after year just recovering lost funds can wreak havoc on the timing of future goals, and may force significant lifestyle compromises in others.

Attempting to avoid the big declines in the first place is a driving principle of our investment philosophy. Not only do we use a robust screening and ranking process to select stocks, but each stock held in our actively managed portfolios is subject to a daily risk management review. Stocks are a useful vehicle for meeting future goals, but we believe conserving capital during market declines is critical to investors trying to accumulate wealth or generate income.

Interest Rates and Bonds

For what seems like a very long time, because it has been a very long time, bonds have enjoyed a tailwind. Falling yields lead to higher bond prices, as existing high rate bonds become more attractive than the new lower rate versions. On September 30, 1981, the yield on the benchmark 10-year U.S. Treasury note hit 15.84%. From that high, the yields spent nearly 36 years in a persistent, if uneven, march lower, reaching a low of 1.36% on July 8, 2016.

This past March the Federal Reserve hiked interest rates for the sixth time. As the Fed continues its program of raising interest rates, the 1.36% yields of a few years ago are quickly receding into history. The yield on the 10-year Treasury bumped up against 3% in February, and closed the quarter at 2.74%. While these yields are still low by historical standards, the tailwinds of yesteryear may be tomorrow’s headwinds for bond prices if interest rates continue to move higher.

In a world of low yields, investors have sought to fill the income gap with high yield bonds, or “junk bonds”. As appealing as the high rates on junk bonds may be, history suggests these investments should be marked “handle with care”. On May 29, 2007, high yield bonds3 offered a yield of 7.45% compared to yields of 4.88% on the 10-year Treasury or 4.90% on the 2-year Treasury. By December of 2008, a little more than a year and a half later, the high yield index had lost 34.50% of its value – a high price to pay for an extra 2 ½% in yield.

Finding ways to provide high current income from bonds is important. Protecting the investment capital that’s producing that income – the value of the account – is just as important. We rely on the bond models we have developed to adjust the credit quality, duration, and market segment of portfolio bond holdings as we look for attractive levels of income consistent with the risks income investors face.

A Multiple-Choice History Test

So, what should we do with all this information about the past? There are several approaches we could take:

a) We could decide that the future will differ from the past so much that the “lessons of history” have nothing to teach us. This is a very popular view that we have heard many times before. There was the “New Paradigm” of the internet that would change the economy and markets forever. The internet has certainly changed things, but it didn’t prevent the “dot com” stock market bust. There was the rush into real estate, because “they aren’t making any more land.” True, no more land was created, but the housing collapse triggered the banking crisis that plunged the global economy into the deepest recession since the 1930s anyway. Today investors are pouring money in unprecedented amounts into passive index funds, in what looks very similar to crowded trades of the past. What could go wrong?

b) We could accept that we may be able to learn from history, but that if trouble ever comes again we’ll be able to see it coming in plenty of time to avoid it. After all, the economy has been expanding for years, recent dips in stock prices have turned out to be buying opportunities, and if things really start to fall apart then we’ll do something about it. Of course, the track record of investors making sound, unemotional decisions about their investments “on the fly” has not been good. Yesterday’s investors somehow managed to miss or dismiss the warning signs that today seem obvious to us in retrospect. Is there evidence to suggest that next time will be different?

c) Another possible way to proceed is to simply “grin and bear it”; allow any future calamities to do what they will to our investments – and to our financial plans. During our careers as investment managers and advisors, we have met precious few real-life people who were able to follow through on this kind of passive, buy and hold approach as they watched their account values plummet.

d) None of the above.

The debate about how to invest in an uncertain world is often framed as being between active versus passive. We believe it would be better to think about the approaches as being between responsive and unresponsive.

We’ve devoted a good part of our company’s history to developing a disciplined, responsive approach to investing that’s intended to take both the rewards of investing – and the risks – into account. It’s an approach we designed with the goal of helping investors grow and protect their serious money – the money they can’t afford to lose.

For nearly 30 years, we have had the good fortune of being trusted by our investors to help them meet their goals, whether that meant providing current income or growth of capital, as we have lived through many of the events described above. Their success stories are the favorite parts of our history. As every passing day writes another page of history, we look forward to helping our current and future investors enjoy many more satisfying chapters.

- Gary E. Stroik

Chief Investment Officer

1http://news.gallup.com/poll/211052/stock-ownership-among-older-higher-income.aspx

2NCHS Data Brief No. 293, December 2017

3Bloomberg Barclays US Corporate High Yield

Past performance does not guarantee future results.

The views presented are those of Gary E. Stroik, and should not be construed as personalized investment advice or a solicitation to purchase or sell securities referenced in the Market Commentary. All economic and performance information is historical and not indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter, will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any discussion or information provided here serves as the receipt of, or as a substitute for, personalized investment advice from WBI Investments or from any other investment professional. To the extent that you have any questions regarding the applicability of any specific issue discussed to your individual situation, you are encouraged to consult with WBI Investments or the professional advisor of your choosing. All information, including that used to compile charts, is obtained from sources believed to be reliable, but WBI Investments does not guarantee its reliability. Sources for price and index information: Bloomberg (unless otherwise indicated). WBI Investments pays a subscription fee for the use of this and other investment and research tools. WBI Investments and Bloomberg are not affiliated companies.

Our current disclosure statement as set forth on Form ADV Part 2 is available for your review upon request.

WBI managed accounts may own assets and follow investment strategies which cause them to differ materially from the composition and performance of the indices or benchmarks shown on performance or other reports. Because the strategies used in the accounts or portfolios involve active management of a potentially wide range of assets, no widely recognized benchmark is likely to be representative of the performance of any managed account. Widely known indices and/or market indices are shown simply as a reference to familiar investment benchmarks, not because they are, or are likely to become, representative of past or expected managed account performance.

Additional risk is associated with international investing, such as currency fluctuation, political and economic uncertainty.

Annualized Rate of Return is the return on an investment over a period other than one year (such as one quarter or two years) multiplied or divided to give a comparable one-year return.

Index Definitions

- The Dow Jones Industrial Average (DJIA or "The Dow") is a price-weighted average of 30 of the largest blue chip issues traded on the New York Stock Exchange.

- The S&P 500 Index includes a representative sample of large-cap U.S. companies in leading industries. The S&P 500 Total Return Index includes the performance effect of the dividends paid by the stocks in the index.

- The NASDAQ Composite Index (NASDAQ) is a market-value weighted index of all common stocks listed on NASDAQ.

- The Russell 2000 Index includes the smallest 2,000 stocks in the Russell 3000 Index (approximately 8% of the total market capitalization of the Russell 3000 Index) of the Russell data series.

- The MSCI EAFE Index (EAFE) is an unmanaged index based on share prices of approximately 1,470 companies listed on stock exchanges around the world. The stocks of twenty countries are included in the index.

- The Hang Seng Index is a capitalization-weighted index of 33 companies that represent approximately 70% of the total market capitalization of the Stock Exchange of Hong Kong.

- Nikkei-225 Stock Average (Nikkei) is a price-weighted index of 225 blue chip Japanese companies listed in the First Section of the Tokyo Stock Exchange.

- The Dow Jones Equal Weight U.S. Issued Corporate Bond Index is an index of 96 bonds issued by leading U.S. companies designed to represent the market performance, on a total-return basis, of investment-grade bonds.

- The Barclays Treasury Bond Index is an unmanaged index that includes public obligations of the U.S. Treasury that have remaining maturities greater than 1 year.

- The U.S. Dollar Index is computed using a trade-weighted geometric average of six currencies. The six currencies and their trade weights are: Euro 57.6%; Japanese Yen 13.6%; UK Pound 11.9%; Canadian Dollar 9.1%; Swedish Krona 4.2%; Swiss Franc 3.6%. These specifications are subject to change.

- The Commodity Research Bureau Index (CRB) provides a broad measure of commodity price trends by averaging prices of seventeen commodities from energy, grain, industrial material, livestock, and precious metal groups.

- The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All