Why We Favor Active Management in Emerging Market Bonds

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUMMARY

- Despite evidence in favor of active management, passive management has gained popularity in emerging markets (EM) fixed income recently.

- Active management has a strong track record of actually delivering alpha versus the major EM bond indexes.

- We see many factors unique to emerging markets that bolster the case for active management in the sector. Several are structural and not predicated on a portfolio manager simply making the right call on a particular country.

As in other asset classes, passive management has gained popularity in emerging market (EM) fixed income recently. However, we see many factors unique to emerging markets – several of which are structural and not predicated on a portfolio manager simply making the right “call” on a particular country – that bolster the case for active management in the sector.

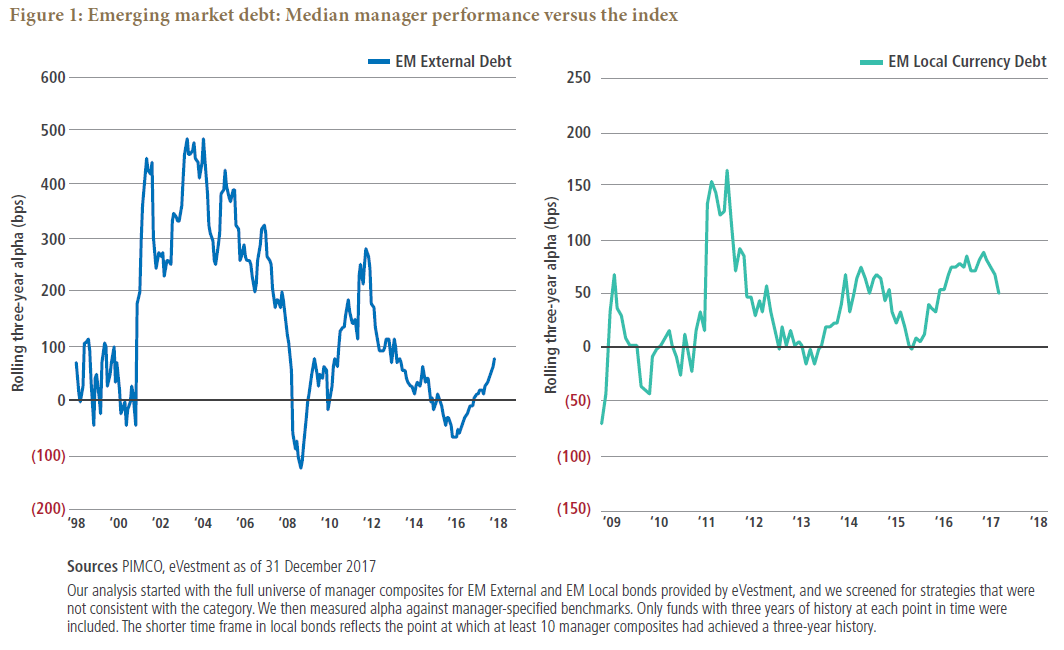

The charts in Figure 1 show a history of rolling three-year alpha for the median manager in EM external debt and EM local currency debt. While periods of underperformance are not unheard of, they tend to be associated with shocks, such as the global financial crisis in 2008-2009, and have historically been followed by meaningful recoveries.

We view this track record as one of the reasons that passive management has been slower to gain a foothold in EM fixed income than in other asset classes and as a strong piece of evidence in the case for active management.

Even if we ascribe some portion of the median manager’s success to luck, we think investors weighing active versus passive approaches should consider the myriad inefficiencies in the EM fixed income opportunity set. Here we examine several that — in our observation — persistently contribute to or detract from manager alpha in both local and hard currency bond investing.

Local EM debt: structural factors

The market-standard benchmark for international investors in local, or domestic, EM fixed income is the JP Morgan GBI-EM Global Diversified Index (GBI-EM GD), which is composed of local-currency-denominated government securities and uses a weighting scheme that limits the allocation of any single country.

We have identified two “structural drags” on performance that are not accounted for by the index and typically detract from investors’ returns.

1. Taxes: A number of EM countries tax foreign investors. The most common are withholding taxes on coupons and capital gains taxes on bond price appreciation. Colombia, for example, applies a 14% tax on coupons paid to foreign investors. To discourage hot-money flows, some countries use complex tax rules: sliding scales based on the time securities are held; requirements to set aside some portion of inbound capital on an unremunerated basis; and outright levies on inflows, which represent an immediate haircut to the investment. All of these taxes effectively reduce returns to investors.

Amounts vary depending on the investor’s domicile, but for the jurisdictions in which PIMCO’s investment products are domiciled, we estimate between 13 basis points (bps) and 40 bps of annual “drag” from taxes merely from holding the securities in the index. While some passive strategies make no attempt to mitigate these drags, others actually lower the bar by adjusting their targets based on the estimated tax burden. For example, the Bloomberg Barclays Emerging Markets Local Currency Core Government Bond Index currently deducts 36 bps per year to approximate the tax impact on performance. Either way, the net effect is that passive investors are locking in some level of underperformance versus the beta, or index, their asset allocation decision was likely anchored on.

While we have yet to see any active fund adopt a tax-adjusted benchmark, active managers can take advantage of tools that provide more tax-efficient exposure, such as replicating cash bond exposures synthetically through credit-linked notes or combinations of other offshore instruments. Although these may not fully offset taxes, we think they are a more favorable option than simply incurring local taxes.

2. Transaction costs: The diversification methodology in the JP Morgan GBI-EM Global Diversified Index redistributes weight from countries that would otherwise exceed 10% to the smaller countries in the index. While this is arguably a better approach than having, say, one-third of the index exposed to a single sovereign, it results in a monthly rebalancing exercise that produces turnover. Importantly, this turnover will be required of any portfolio – active or passive – that seeks to keep its positioning constant relative to the index. Further, during the monthly rebalancing, the index also takes on new eligible bonds and drops those that no longer fit the criteria (for example, removing those with less than 13 months to maturity), thus adding to the turnover.

For a rules-based pure passive approach where the goal is to hew as closely to the index as possible, this likely means trading many bonds at the month-end rebalancing, irrespective of current liquidity conditions. By contrast, the active manager has the luxury of deciding on the optimal time to trade, and can even anticipate what passive participants will be doing, potentially using this information to advantage.

Local debt: opportunities for added return

In addition to minimizing or taking advantage of structural issues, we have identified four compelling opportunities for active managers to generate alpha that go beyond simply over- or underweighting a given currency or bond market.

Capital preservation: Despite widespread agreement on the benefits of floating exchange rates, a number of EM countries have resorted to capital controls during times of economic stress. For example, in 2015, conversion of the Nigerian naira became increasingly difficult as the country’s international reserves dwindled and authorities sought to protect their liquidity. Ultimately, capital controls were employed, the country was removed from the JP Morgan GBI-EM GD Index and foreign investors’ holdings were trapped onshore. Active managers can potentially mitigate this risk by assessing the likelihood of capital controls, making use of offshore instruments such as nondeliverable currency forwards and nondeliverable interest rate swaps, or avoiding a market altogether. Moreover, careful analysis can allow an active manager to move proactively, unlike the passive bondholder who typically maintains exposure as long as the index does, which may be too late to divest. (In the case of Nigeria, PIMCO moved exposures offshore months before the country’s removal from the index).

Market depth (or lack of it): No domestic emerging bond market matches the depth and efficiency of the U.S. Treasury market. Liquidity is much less uniformly distributed along domestic curves in EM for many reasons; in general, these markets are less mature, and the size of each bond on offer differs. An active manager, who has a patient pool of capital to deploy, can optimize security selection decisions and find many opportunities for less liquid – and potentially higher-yielding – bonds within local markets, which are likely to be small but consistent contributors to alpha.

Off-index opportunities: By construct, the JP Morgan GBI-EM GD Index screens markets for ease of entry and egress, currency convertibility and clearly understood auction, repo, settlement and custody mechanisms. In practice, this has limited the index to 18 countries (neither China nor India is among them), a marked contrast to the external debt index, which is now made up of 67 countries. For a manager willing to do the operational legwork to secure access to these markets – in addition to their investment process – taking a more expansive view of the opportunity set can potentially pay off. In 2017, for example, the Czech Republic outperformed the broader index by nearly 6% between its inclusion in the index in May and year-end. In addition, the ability to move between nominal and inflation-linked bonds, which do not feature in the index, may provide more opportunities for alpha.

Currency and rate exposures: Separating currency and interest rate risk is squarely in the domain of active management. While common macro factors underpin both, the valuation metrics and performance drivers can diverge meaningfully. In fact, over the 15 full years of available data, the divergence between performance of the bond and currency components of the JP Morgan GBI-EM GD Index has averaged over 9% per year. Thus, the ability to distinguish between the two – perhaps even overweighting one and underweighting the other within the same portfolio – can potentially be a significant source of alpha.

External EM debt: finding opportunities for value

In EM external debt, which is denominated in hard currencies and more widely held by global investors, passive investing that tracks an index forgoes many opportunities to add value, while active managers can exploit market (and index) inefficiencies and other opportunities to capture potential value.

Including the broad universe of the EM external index: Passive replication of traditional EM external debt indexes faces a dilemma: Of the 67 countries in the widely tracked JP Morgan Emerging Market Bond Index Global or EMBIG, almost two-thirds (42 to be exact) had less than 1% weighting in the index and collectively represented just 15% of the index’s market value (i.e., a 0.34% average weight) as of the end of March 2018. This is a much less liquid part of the EM universe, and taking exposure to it can therefore incur material trading costs, especially during risk-off periods. At the same time, however, this part of the index universe can contribute a not-insignificant share of the EMBIG yield (currently just under 1% of the 6% yield) and has also performed well in rising markets (for example, in 2017 this group returned 12.4% versus 9.3% for the full EMBIG). Performance within the group is widely dispersed: In 2017 the external debt of Bolivia returned 0.47% whereas that of Angola returned 24.2%. So, one passive solution is to exclude many of these smaller names to avoid holding less liquid bonds (which some indexes designed for ETFs do), and an active solution is to consider every one of them, analyze them, including through country visits, and make relative value calls to exploit any inefficiencies.

Avoiding “black holes”: The analog to the risk of capital controls in EM local investing is default risk in EM external debt. While passive strategies generally avoid defaulted securities because they are typically removed from the index, an active manager makes a decision in each case. An active manager may elect to hold exposure to a potential default if the expected recovery value combined with the cost and workload of going through a restructuring process is above current pricing; indeed, EM investors look to the secular maturation of these economies as a source of return (i.e., they expect to earn outsized compensation for the credit risk actually borne). However, in most cases from an active management perspective, the path to successfully generating long-term outperformance comes through sidestepping the “black holes,” because the recovery process is highly uncertain in both timing and value. In any event, an active investor has more options and the potential for harvesting extra value.

Exploiting rules-based (passive) investing: Passive investments in EM external debt can simultaneously reduce value for passive investors and provide opportunity for active strategies. Consider the case of bonds being removed from their index due to a credit downgrade or default. Our portfolio management team has tended to observe that passive strategies divest coincident with index exclusion regardless of whether the bonds have repriced significantly lower or are trading in a very illiquid market. Not only does this lead to a crystallization of losses, but executing the trades so quickly after the exclusion can compound losses by begetting even lower prices. It is worth noting that the impact of this herd behavior has grown with the increase in passive assets under management in EM. Passive investments have grown sufficiently large that an active manager can potentially capitalize on this inefficiency, either by selling in anticipation of the downdraft or by buying attractively priced bonds following it. In effect, this “forced selling” facilitates a transfer of potential value from passive to active managers.

Taking advantage of new-issue concessions: Access to primary markets is a source of added value for active investors. Indexes add new bond issues anywhere from the nearest month-end (at best) to several months out, depending on index rules and the format of the issue. This puts passive strategies at a disadvantage because EM issuers tend to offer better yields on new debt issues than existing bonds in the secondary market (the so-called “new- issue concession”) to attract capital. And the trend of the last 18 months−24 months has been for new EM issues to be well oversubscribed, leaving some investors with fewer bonds than they wanted, which tends to drive up prices for the bonds in the secondary market. By the time the new issue is included in the index, its price has often risen even further due to the additional demand coming from passive investment vehicles buying at month-end when indexes rebalance.

Playing the odds

With any investment, choosing between active and passive management largely comes down to assessing the trade-off between the risk that an investment deviates from its benchmark index (as measured by beta and tracking error) and the expected relative performance (measured by alpha). With a passive strategy, tracking error is generally expected to be very modest and – on the flip side–alpha is generally assumed to be zero (technically, zero less management fees).

In EM, passive investors have likely seen consistent underperformance beyond just fees due to structural factors like taxes and transaction costs. Moreover — of critical importance and different from what we see in some other asset classes — active management has a strong track record of actually delivering alpha versus the major EM bond indexes.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Management risk is the risk that the investment techniques and risk analyses applied by a manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to PIMCO in connection with managing the strategy.

There are several differences between active and passive investing. In general, passive investment strategies are subject to lower fees and expenses which impact performance. Active managers have the potential to generate alpha but can be subject to greater volatility and risk. Alpha is a measure of performance on a risk-adjusted basis calculated by comparing the volatility (price risk) of a portfolio vs. its risk-adjusted performance to a benchmark index; the excess return relative to the benchmark is alpha. Tracking error measures the dispersion or volatility of excess returns relative to a benchmark. An investment portfolio pays transaction costs when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes for taxable accounts. PIMCO does not provide legal or tax advice. Please consult your tax and/or legal counsel for specific tax or legal questions and concerns.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Investors should consult their investment professional prior to making an investment decision.

References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All