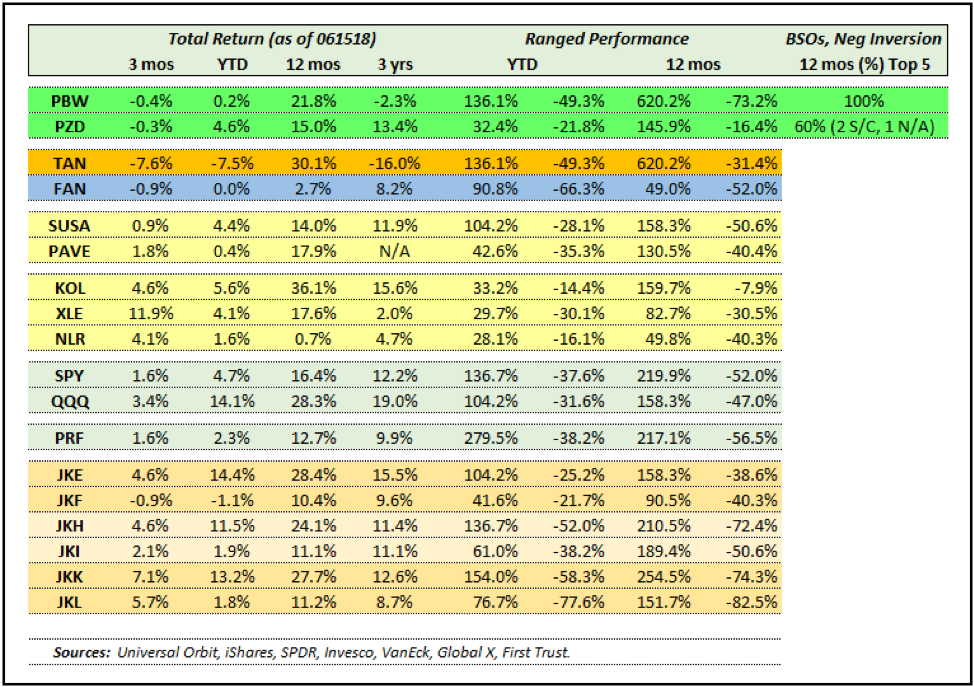

Renewables evolution within the Energy complex represents boom-to-bust then boom again scenario sequencing consistent with subindustry core emergence. Patterned development over the past ten years is indicative of hard forged self-reliance evidenced by direct corporate ownership of wind farms and distributed solar generation located atop major retail stores, both far from government sponsorship of select alternative energy companies at above market rates. Today, climate change skeptics face the certainty of value-based cultural movements.

Survey of US Department of Energy and International Energy Agency publications in this context detail electric generation capacity parameters (Oil&Gas, Coal, Nuclear, Renewables) and power trend growth rates effecting companies populating each Energy producing segment and classification. Current period demand-side Energy equation power consumption dynamics converge to shape investment opportunities among supply-side Energy equation power capacity providers and requisite ecosystems across economic sectors and within industry verticals. Corporate-sponsored Green programs place Apple, Google, Target, Walmart and similar ethos companies at the forefront of US Renewables policy alongside federal tax incentives, state mandates, municipalities and utility companies. Here at the intersection of Renewables, Infrastructure and Environmental, Social and Governance programs lies the tangential path to Alpha.

On a Beta-relative basis, populist trends and momentum strategies in tandem long offered positive realizations yet while macro and sector bets via active management or ETF allocations are relatively straightforward, thematic- and niche-Beta strategies leave Alpha-driving issues such as constituency breadth and corporate profile maskings unreconciled. Product development and newly crafted thematic indexes frequently compound errors by misaligning comparables, increasing susceptibility to performance drags relative to benchmark asset class indexes. Counter-thesis positioning and comparable assignment inaccuracies (e.g. derivatives exposure against long-only benchmarks, government comps for corporate bonds) further hamper attempts for transparency and cloud opportunity costs. Series development of independent benchmark portfolio overlays enhance performance attribution and tests the veracity of fund company marketing campaigns.

Index applications addressing limitations in allocated Beta strategies for integrated Alpha efforts necessitate a realignment of teamed analytical data sets. Quantitative exercises to isolate Value in Growth companies (and Growth in Value) begin by deconstructing relevant Large-Cap companies into modular corporate business segment operations (BSOs), aligning revenue drivers with each other and those from Small- and Mid-Cap competitive peers. Replacing common sector/industry/subindustry index designations with descriptive BSOs is a deliberate first step Beta-capture to an eventual Alpha-screened second cluster. BSOs universally reflect directly the financial impacts of planned product cycle/subcycle positioning and avoid a broad array of component members recurrent in passive indexes, structured thematic portfolios and active index-plus strategies.

Benchmark proxy ETF composite reporting, typically grouped into five generic industries or nondescript third party categorizations, is often inconsistent with middle-down allocated Beta strategies on a relative basis or in standard nine-grid style/size box format. Due diligence at this point creates an opportunity to reconstruct benchmark proxy ETF attributes from the bottom-up, realizing the value-add of BSOs placement into segment/classification industry verticals. BSOs improve situational awareness by pairing forward-looking valuation analytics (i.e. variance of constituency portfolio weights to market capitalization per segment/classification) with competitive market information (functional peers, acquisition candidates) at defined points of inflection.