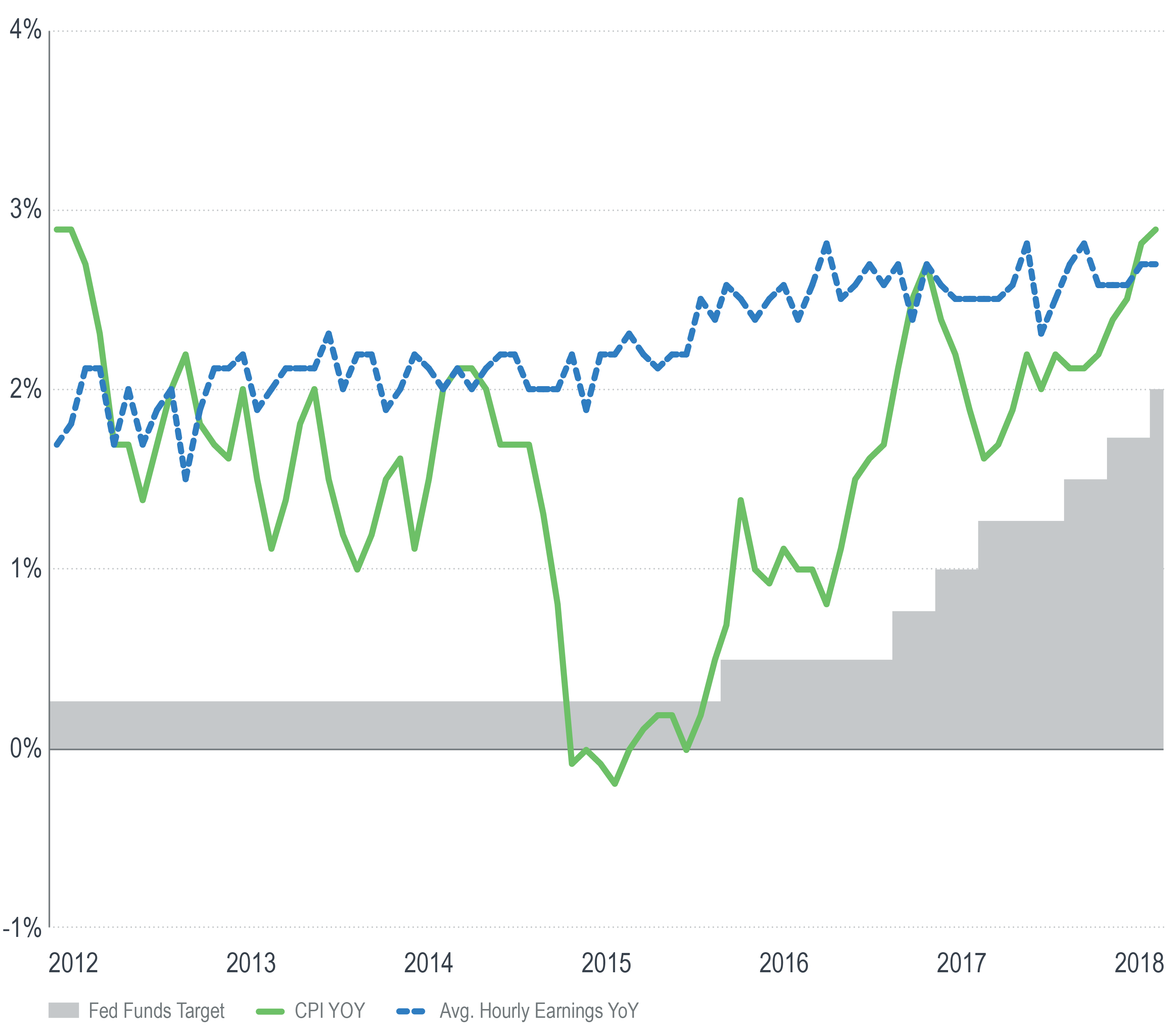

The June release of inflation data from the Bureau of Labor Statistics showed that the consumer price index (CPI) increased by 2.9% over the past 12 months. This is the highest level of inflation since February 2012.

In addition to being higher than the fed funds rate, the rate of inflation now also exceeds the rate of wage growth by the widest margin since 2012.

These signals of mounting inflationary pressure put a bigger focus on monetary policy.

The Fed is now seven rate hikes and tens of $billions into its policy normalization process. In June it raised the Fed funds rate from 1.75% to 2% and further trimmed its balance sheet, bringing the nine-month cumulative reduction to $160 billion.

In one sense this is a meaningful amount of activity; in another, however it’s not. At 2%, the Fed funds rate is still 280 bps below its 20-year pre-crisis average. Moreover, while a $160 billion reduction is large on a nominal basis, it’s still less than 4% of the nearly $4.5 trillion the Fed started with.

With wages and inflation trending higher, investors will be closely watching to see if the Fed’s normalization efforts have been too little and too late to keep inflation in check.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.