Chart of the week: 03/11/2019 – 03/15/2019

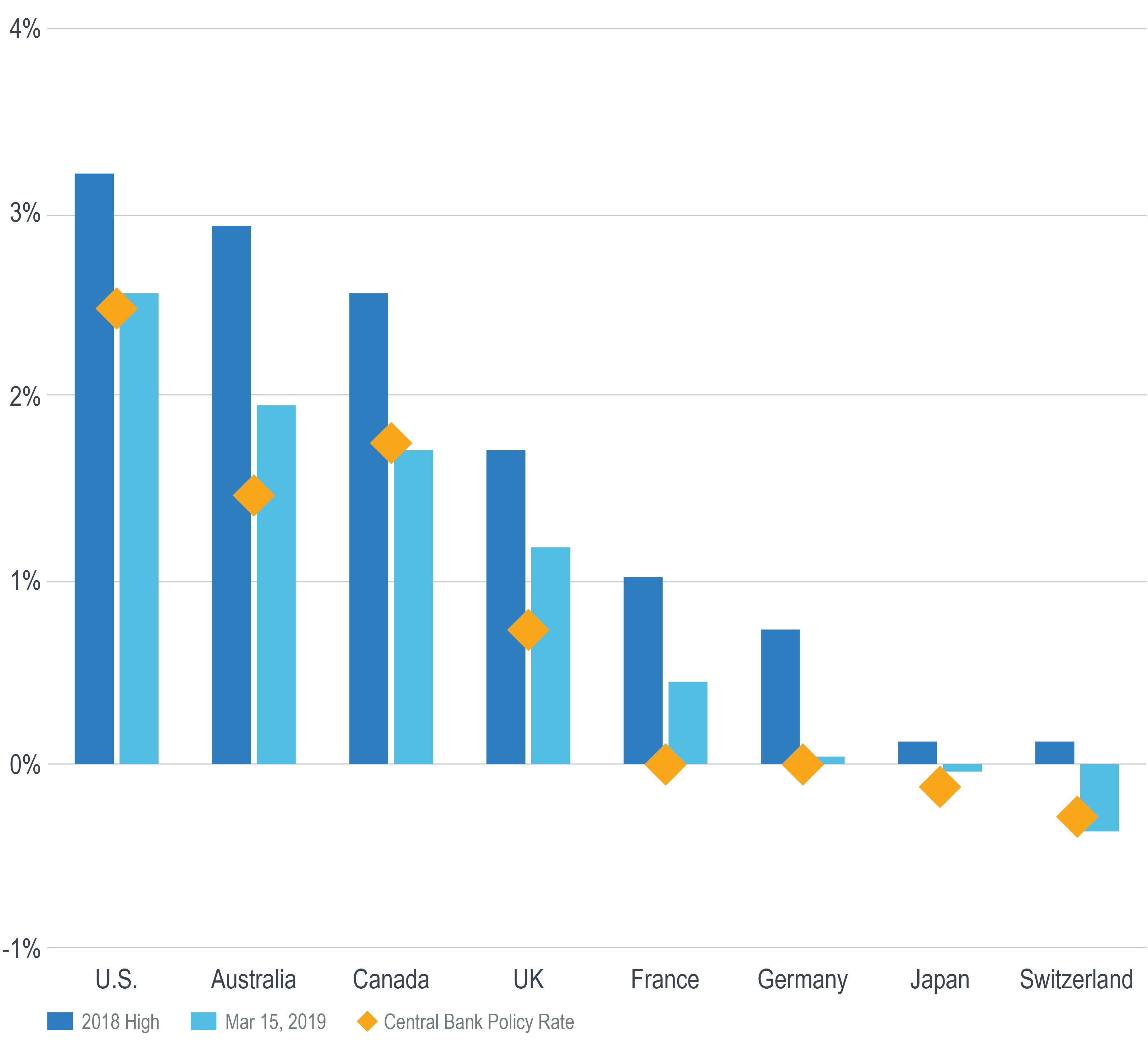

Developed Market Sovereign 10-Yr Yields

Extraordinary policy measures are proving extraordinarily difficult to undo.

It may be no coincidence that as two of the world’s biggest central banks have made dovish policy shifts, interest rates have also declined.

On November 28, 2018, Fed Chairman Powell altered the Fed’s forward guidance on rates from being, “a long way from neutral…probably,” on October 3, to “just below neutral.” These comments were formalized in the Fed’s January meeting statement and minutes.

On March 7, 2019, the European Central Bank announced plans to make new cheap loans available for banks. This comes just three months after announcing that it would end its bond buying program.

As of the end of 2018, data from Bloomberg indicate that assets at the central banks for the countries in the chart now stand at a combined $15.9 trillion USD, approximately $54 billion more than the amount from 12 months ago, notwithstanding the nearly $500 billion by which the Fed has already reduced the size of its balance sheet.

The Bank of Japan’s balance sheet is now larger than its annual GDP; for the group as a whole, combined central bank assets represent about 40% of their combined nominal GDP.

In addition to the Fed floating the idea of “completing the normalization of the size of its balance sheet,” the fed funds futures market now shows a 33% chance of a rate cut by the end of 2019, vs. 0% of a rate hike.

If these policy reversals suggest anything, it may at the very least be that reliance upon the exceptional policy measures implemented in the wake of the financial crisis is proving more difficult to undo than initially expected.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.