Potency of the Fed Put: Then and Now

This reloaded Fed is a shadow of its former self.

After using much of its available ammo to fight off the 2008 financial crisis and recession, the Fed has spent the past few years trying to reload to be ready for the next ones. But the policy normalization process that the Fed embarked on at the end of 2015 appears to have come an end.

Coming out of its March meeting, in addition to communicating a posture of patience in making future rate adjustments, the Fed also announced that it will end its balance sheet run off later this year.

Whether or not the Fed actually considers policy to be normalized isn’t entirely clear; but for now, the policy normalization process is done.

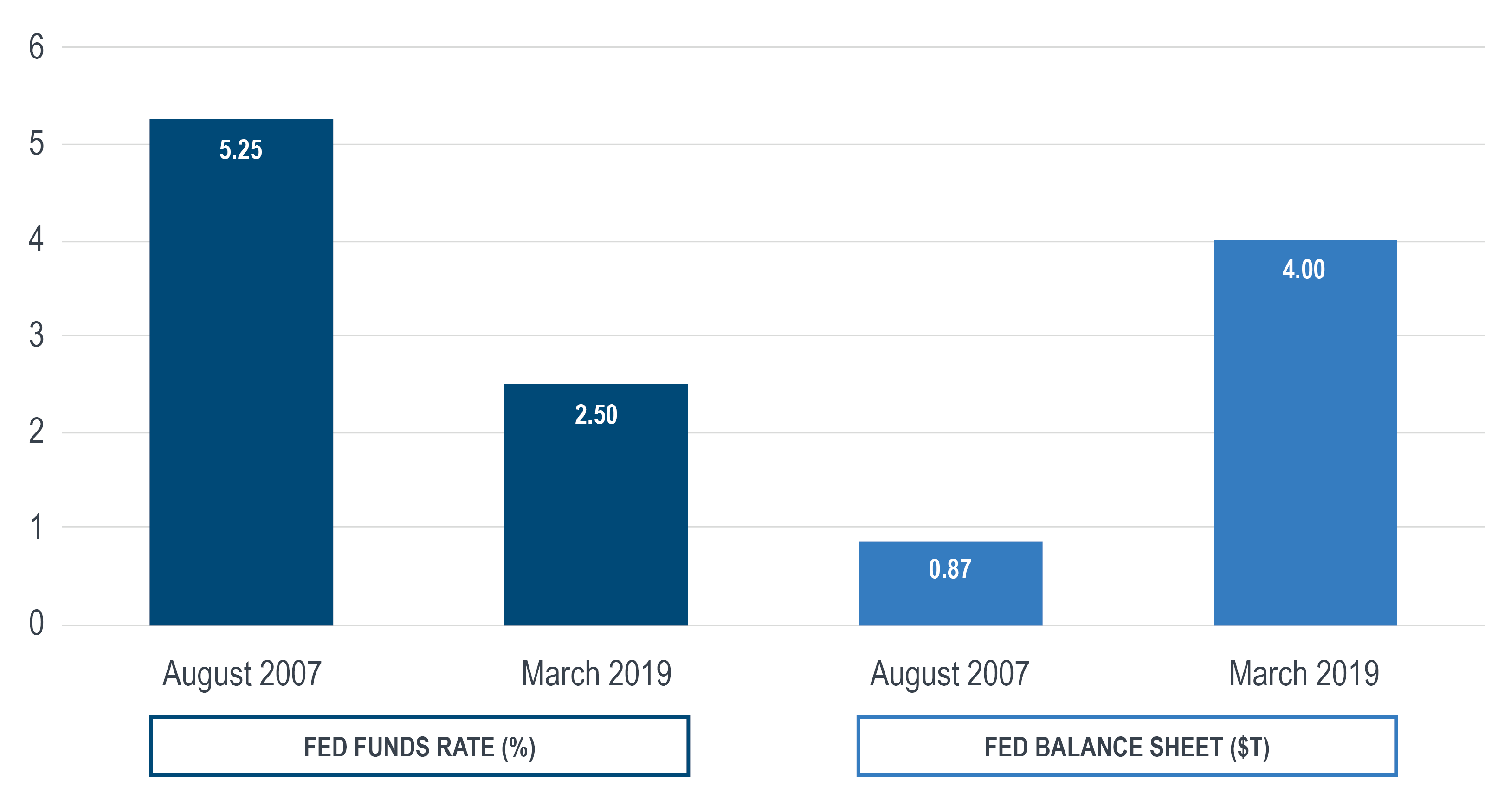

Confirmation of its dovish stance sent markets higher. After all, a 2.5% fed funds rate and a $4 trillion balance sheet are, by historical standards, highly accommodative.

The circumstance, however, does make one wonder: is the economy still so weak as to need so much monetary accommodation, or is the notion of ‘neutral’ policy simply lower in the post crisis era?

In any event, investors applauded the announcement, pushing equity markets sharply higher the following day. If the reasons to be bullish were self-evident, reasons for concern may not have been so readily apparent.

One risk of the current policy stance is that it leaves the Fed with much less firepower to respond to the next crisis. In 2007, the fed funds rate was more than double what it is today, while the size of the balance sheet was less than one-quarter of today’s size.

This has at least two significant implications:

1. Relative to 2007, the Fed today has fewer available rate cuts at its disposal before reaching zero.

2. Today the Fed’s $4 trillion balance sheet, including $1.6 trillion in excess reserves, suggests that QE, as a means of injecting liquidity, won’t have the same potency that it did at the start of QE in 2008.

Combined, these conditions suggest that the Fed’s ability to act as the market’s ‘back stop’ or ‘put option’ against the next downturn is substantially diminished.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.