The bond market is challenging the Fed to a game of chicken.

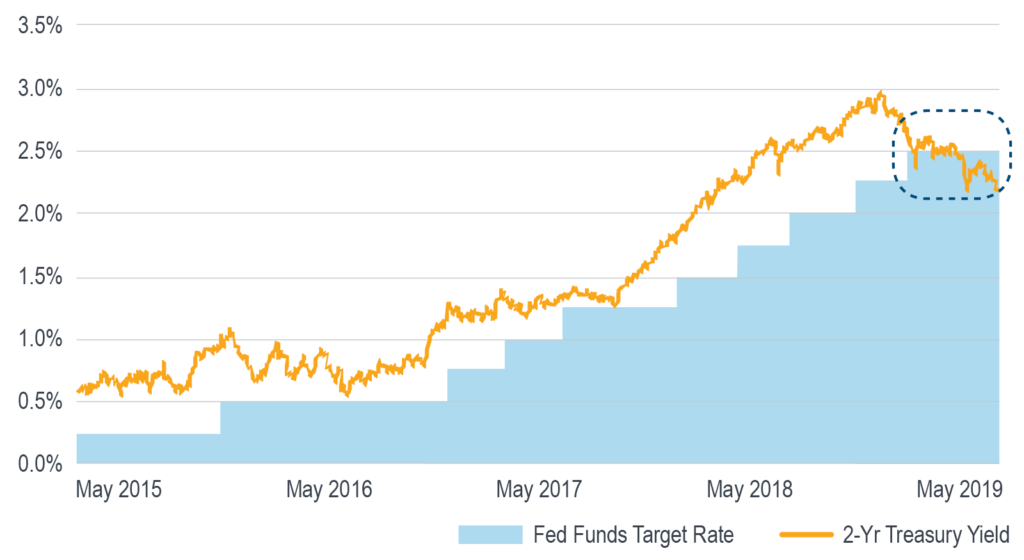

After seven years of keeping the fed funds rate near zero, the Fed embarked on a rate-hiking cycle at the end of 2015, raising the fed funds target rate nine times in three years, from 0.25% to 2.50%.

Over that period, the yield on the 2-yr Treasury always closed above the target rate. It came close to breaking below it in July 2016 and again in September 2017, but quickly reverted higher both times.

The last day of 2018 was the first time that the 2-yr yield breached the fed funds target rate since 2013. Since then it has trended lower and, as of May 15, 2019, has been below the target rate for 50 consecutive trading days.

In addition to the picture painted by the fed funds futures market, this low 2-yr yield level is another strong indicator of the market’s expectation for a fed rate cut before the end of 2019.

If this development is noteworthy without any additional context, the concurrent factors opposing it make it downright odd.

At an early-May press conference, Fed Chairman Powell noted, “We do think our policy stance is appropriate right now. We don’t see a strong case for moving in either direction.”

The following week, the release of CPI data showed that annual inflation had risen to 2.0%.

Nevertheless, (presumably in response to the deteriorating trade talks between the US and China), the 2-yr Treasury yield closed 30 bps below the target rate on May 15.

Assuming an overnight rate can’t long remain above a 2-year rate, it will be interesting to watch in the coming weeks and months whether it will be the Fed or the bond market that will be first to give in.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.