Chart of the week: 09/30/2019 – 10/04/2019

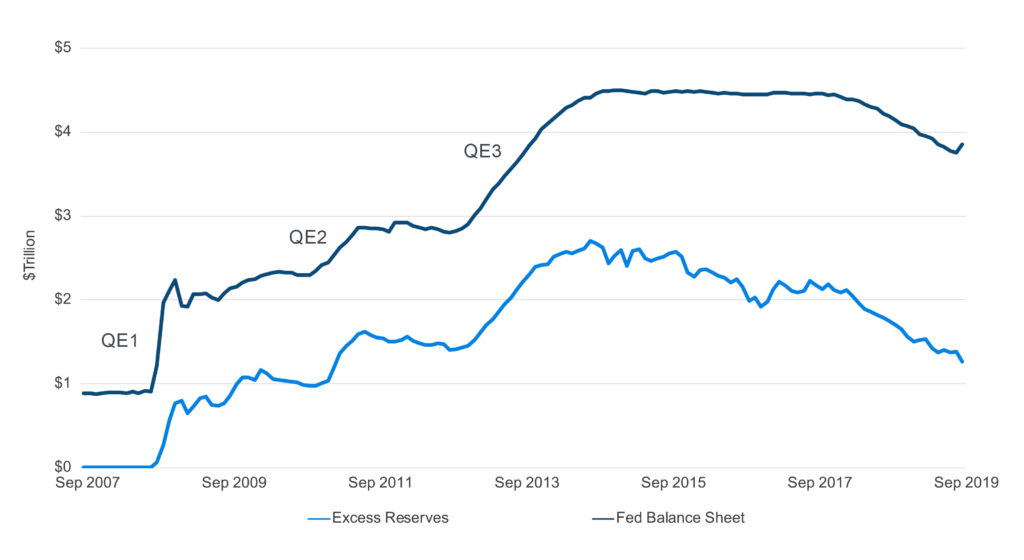

Size of Fed Balance Sheet and Excess Reserves

Thought the Fed was done growing its balance sheet? Think again.

In his September 2019 press conference, commenting on the Fed’s balance sheet policy, Chairman Powell noted,

“[G]oing forward, we’re going to be very closely monitoring market developments and assessing their implications for the appropriate level of reserves, and we’re going to be assessing, you know, the question of when it will be appropriate to resume the organic growth of our balance sheet… it is certainly possible that we will need to resume the organic growth of the balance sheet earlier than we thought. That’s always been a possibility, and it certainly is now. Again, we’ll be looking at this carefully in coming days, and taking it up at the next meeting.”

In February 2019, we commented in these pages that it seemed likely that the Fed, being committed to operating in an “abundant reserves regime,” would eventually need to resume its balance sheet expansion.

The very next month in March 2019, the Fed revised its Balance Sheet Normalization Principles and Plans, stating, that when reserve balances decline “to a level consistent with efficient and effective implementation of monetary policy,”…“the Committee will begin increasing its securities holdings…to maintain an appropriate level of reserves in the system.”

In this context, however, balance sheet growth will be different in purpose and in practice from the balance sheet growth associated with quantitative easing (QE).

Importantly, the Fed will not be growing its balance sheet for the purpose of generating downward pressure on longer-term rates or to shorten the maturities of banks’ holdings. Rather, balance sheet growth will be for the purpose of maintaining the reserve buffer (i.e. an amount in excess of the aggregate demand for reserves) that enables the Fed to control the fed funds rate through its administered rates.

Accordingly, in practice, there is not likely to be a prescribed monthly purchase amount, as was the practice during the rounds of QE. Instead, the Fed will likely make purchases in response to changes in demand for reserves, in order to maintain a buffer size that the Fed deems sufficient.

While different from QE in purpose and practice, it seems reasonable to ask whether or not this form of balance sheet growth will be different in its effect.

Even while the Fed was letting its $4 trillion balance sheet shrink, it remained a significant source of demand for bonds and continued to generate downward pressure on interest rates. Concluding its balance sheet runoff and resuming balance sheet growth will only see the Fed once again grow, both as a source of demand for bonds and in its overall influence in the financial system.