COVID-19: A Positive Tipping Point for Some Brazilian Banks?

The coronavirus pandemic is hurting Brazilian banks in the near term, but is the outlook entirely grim? Franklin Templeton Emerging Markets Equity’s Gustavo Stenzel explains why certain banks could emerge from the outbreak stronger relative to a new pack of financial technology competitors.

Bank stocks globally have been weak as economic activity collapsed amid the COVID-19 pandemic. Expectations of slowing loan growth, falling margins and rising bad debts have hurt near-term earnings forecasts. Many countries have also called upon banks to support borrowers through measures such as loan moratoriums—where repayments are paused—and more. Banks have understandably come under increased scrutiny during this time.

Shares of Brazilian banks have also corrected sharply. Without question, the pandemic will weigh on their businesses in the short term. However, we believe the selloff in bank shares has been excessive, and we see a low probability of a systemic banking crisis in Brazil. We believe select Brazilian banks with strong fundamentals should emerge with the upper hand over untested financial technology (fintech) competitors that could struggle to stay afloat.

Brazilian Banks Were Generally in Good Shape Prior to the Pandemic

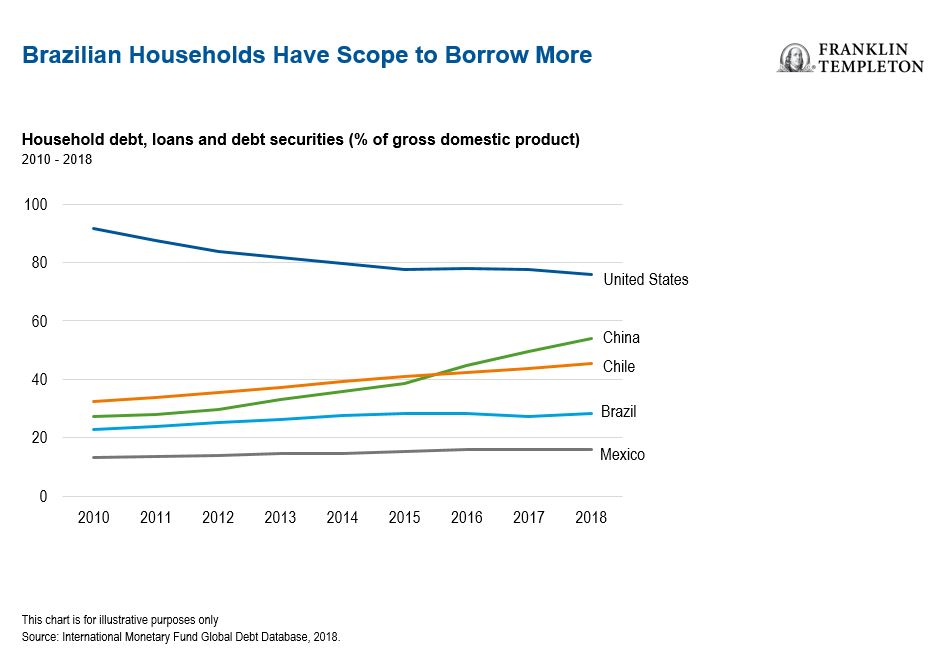

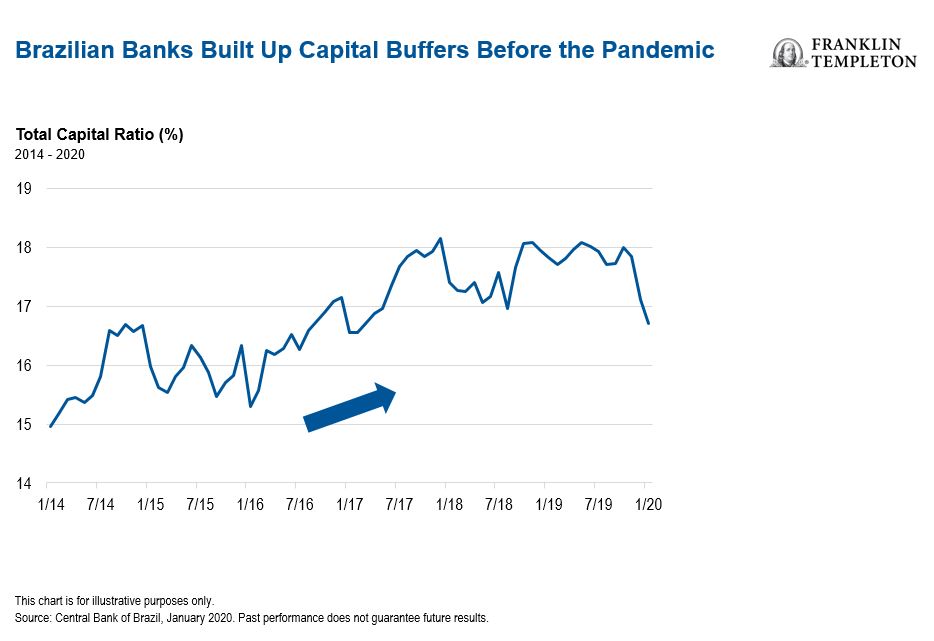

Banks in Brazil largely entered this challenging period better capitalized than during the last crisis the country faced. A domestic recession that unfolded five to six years ago had pushed them to de-risk their balance sheets. Companies and consumers also avoided excessive borrowing as the economy stayed tepid. Given these prior adjustments, we believe Brazilian banks are in generally good shape to endure the current uncertainty.

Before the pandemic, potential disruption from new fintech competitors had undercut investor sentiment toward Brazilian banks. Generous funding from technology investors fostered a fintech boom in Brazil and enabled many start-ups to vie for users with zero- or low-fee business models. Regulators also lowered operating barriers for fintech companies to compete against incumbent banks. Among prominent challengers is digital bank Nubank, which made waves with its app-based credit card with lower interest rates and no annual fees, as well as XP, an online broker. Some niche competition will continue, but we believe there is plenty of room for the whole pie to grow. Key sectors remain extremely underpenetrated, which is the case for mortgages with only 9% of gross domestic product in loans to that segment, compared to over 70% in the United States or United Kingdom. Strong balance sheets that can be leveraged up and access and trust of the client are key advantages for the big banks. Although newcomers are looking forward to the open-banking initiative that will allow access to the client’s credit data, trust will continue to be an important advantage. An example of that is the acceleration of XP’s growth after Itau became part of the key shareholders.