Unicorn Growth Blurs the Lines Between Private and Public Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPrivate capital will continue to be the financing source of choice for tech-driven unicorns for the foreseeable future.

Key Takeaways

- An abundance of private capital continues to fuel the surging digital economy, allowing fast growing tech companies to not only avoid the public markets, but also to provide liquidity to their employees and early investors through an expanding secondary market.

- Despite an impressive resurgence in initial public offerings, the vast majority of companies that have achieved unicorn status remain private, and when they do go public, retail investors are usually forced to pay a significant premium over the previous private round valuation.

- At an estimated $2.8 trillion in aggregate value and spanning multiple sectors, the growing mass of unicorns is redefining the private markets. Investors who want access to the digital economy know they need to tap the private markets, and increasingly, newcomers are doing that through secondaries.

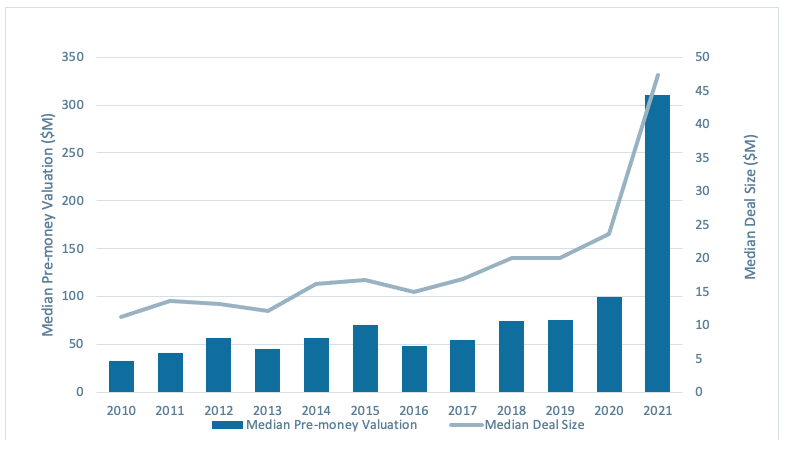

The average private capital-backed tech company that listed in the United States in the first quarter of this year did so at a valuation 2.63 times greater than in its previous private financing round, which occurred just under 16 months earlier, on average.1 This equates to an annualized valuation growth rate of 71%. At the same time, deal sizes have increased sharply (see Exhibit 1), and many unicorns have been doubling in value from one private round of financing to the next – in some cases, within six months. Some notable examples are: Klarna, a Swedish payments company; Canva, an Australian graphic design platform; Instacart, a U.S. grocery delivery company; and Bolt, an Estonian ride-hailing platform.2

One factor contributing to this seemingly circular market effect is the growing volume of secondary transactions in the shares of unicorns – private tech-enabled companies with valuations of $1 billion or greater. As hundreds of unicorns grow older and larger, the need to provide liquidity to long-time employees and early investors has intensified.

Moreover, with primary funding rounds frequently oversubscribed, investors who have been shut out are purchasing shares through secondary sales, often at a significant premium to the previous primary round.3 In fact, an increasing number of large unicorns are now planning programmatic secondary offerings, allowing employees to receive some proceeds and enabling new investors to come in and experience the next phase of growth.4

The valuations of these unicorns are often heavily influenced by comparable public companies. Nasdaq Private Market, in its mid-year 2021 market review, reported a record volume of secondary transactions in the first half of this year, with the number of deals in the $10 million to $50 million range tripling and those north of $100 million more than doubling from the same period in 2020. With no shortage of private capital demand to meet this growing supply, and private shareholders increasingly conducting their own price discovery through intermediaries, valuations are rising rapidly.

EXHIBIT 1: Deal sizes and valuations for private growth companies up sharply in 2021

Median valuations and deal sizes for growth equity and late-stage venture funds globally

Source: PitchBook. Data as of August 6, 2021. For illustrative purposes only.

Elevated valuations are not deterring investment

The global pandemic, which management consultant McKinsey & Co. estimates has accelerated many tech-enabled business models by as much as three to four years, is also a driving force behind this surge in valuations. And while comparable public market values have always been a factor in how private companies are priced, the active IPO market over the past year has been rippling back into private markets to the degree that even experienced growth equity investors are finding it difficult to deploy their dry powder.

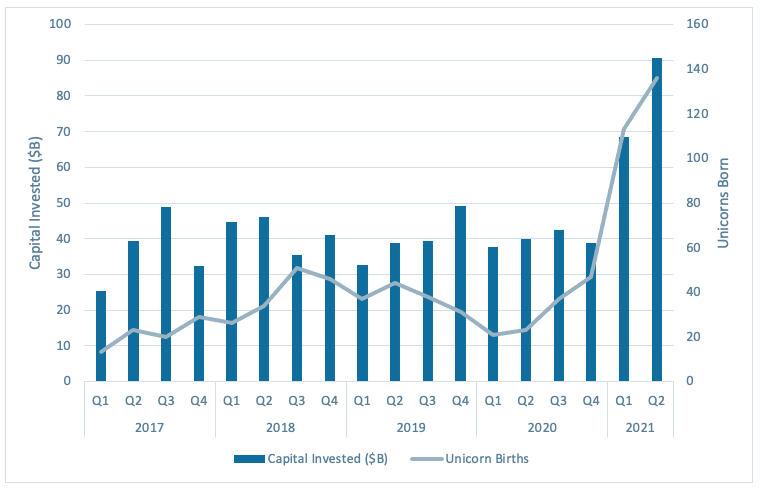

Yet, despite these challenges, the pace of investment has not slowed. On the contrary, more capital was deployed by growth equity and late-stage venture funds in the first half of 2021 ($159.2 billion) than in the whole of 2020 ($158.6 billion) (see Exhibit 2).5

EXHIBIT 2: Private growth financing creates and sustains unicorns

Capital invested by growth equity and late-stage venture funds vs. unicorns created

Source: PitchBook, CBInsights. For illustrative purposes only. Past performance is not indicative of future results.

Significant new capital for growth deals

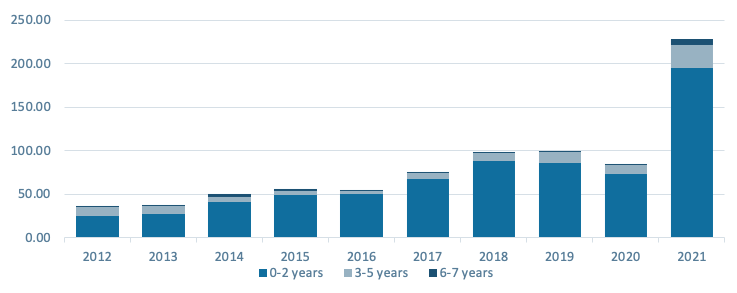

At the same time, these private funds have continued to rake in record amounts of money, raising almost as much in the first half of 2021 ($139 billion) as they did in all of 2020 ($149 billion).6 In addition to PitchBook’s estimate of $232 billion in dry powder within growth equity and venture firms (see Exhibit 3), there is ample capital held by non-traditional investors eager to gain a foothold in this market.7 Investment firms such as Tiger Global Management are deploying capital with unprecedented speed, placing less focus on entry valuation and more on securing index-like exposure to outperformers that can drive outsized returns. A recent report from Goldman Sachs found that hedge funds invested an incremental $153 billion into private companies in the first half of this year, compared with $96 billion in all of 2020.8

EXHIBIT 3: Early-stage dry powder surged in 2021

Growth equity and late-stage venture fund dry powder, by age of fund

Source: PitchBook, as of August 2, 2021. For illustrative purposes only. Past performance is not indicative of future results.

This record level of dry powder combined with the knock-on effect of the strong IPO market are clearly having a pronounced impact on the valuations of these high-growth private companies, particularly the larger, highest profile names. Yet, while private valuations seem to be soaring to unprecedented levels, the spread between public and private valuations has remained remarkably wide – again, 2.63 times on average in the first quarter (see Exhibit 4).

EXHIBIT 4: The spread between private and public valuations remains large

Data for Q1 2021 privately backed tech IPOs

Source: PitchBook, CapitalIQ. For illustrative purposes only. Includes all tech IPOs backed by PE or VC firms in Q1 2021 for which data is publicly available (19 out of a total 34). Last Private Valuation is post-money valuation at last financing round involving equity issuance or last investment into the company. Excludes SPACs. Past performance is not indicative of future results.

One factor likely contributing to this public-private spread seems to be a basic supply-demand imbalance. As of September 30, the aggregate value of unicorns reached an estimated $2.8 trillion,9 but public exposure to this market remains relatively limited. Despite the impressive increase in the number of public offerings this year – 76 tech IPOs through July 31, compared with 44 in all of 202010 – the number of unicorns going public is still only a small fraction of the total. Of the 896 companies that have achieved unicorn status globally in the last five years, 761, or 85%, remained private as of the end of the third quarter.11

At a macro level, a sustained environment of low interest rates and low inflation has created a risk-on environment that has favored growth investments (both public and private), which tend to trade more on future earnings prospects than current financial metrics. This, of course, means that during periods of heightened inflationary expectations the inverse will occur, and markets will discount the value of future earnings at a higher interest rate.

Not surprisingly, all these factors have driven up IPO pricing to levels not seen since the year 2000, before the dot-com crash, with the median price-to-sales ratio of tech stocks at listing reaching 14.6 times as of the end of July.12 The total value of IPOs globally in the first half of 2021 reached $334 billion, compared with $248 billion for all of 2020.13 Though these data points may invite worrying comparisons with the dot-com bubble, this time it is fundamentally different.14 Most unicorns achieving high valuations today have more sustainable business models, often with strong recurring revenue.

A New Era in Private Markets?

As the number and the size of unicorns continue to rise – with many of them eclipsing $10 billion in value and a smaller number surpassing $50 billion – we may be entering a new era for the private capital markets.

For the past two decades, venture and growth equity have been the dominant source of capital fueling the software-as-a-service (SaaS) movement and the digital economy. With ample capital to continue funding both their growth and liquidity needs, most of these companies will remain private – which makes sense when you consider the inherent benefits of being private. The entrepreneurs and executives running these businesses can continue to focus on their long-term strategic goals without the distraction of quarterly earnings calls and without having to disclose financial information and key performance indicators to competitors.

Growth landscape offers reasons for caution

Regardless of how this dynamic plays out, investors need to be particularly diligent in evaluating any growth equity investment opportunity and should also remain mindful of the risk of inflation.

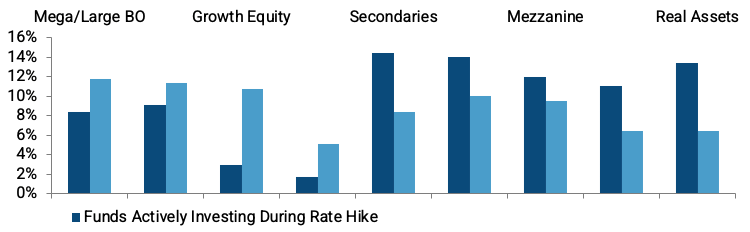

A rise in interest rates could conceivably spur a broad rotation out of growth and, potentially, sharply reset both public and private valuations. This would not just crimp private fund returns generated from IPO exits, but also lead to reductions in the fair value of portfolio companies. According to data from Hamilton Lane,15 rising interest rates have negatively impacted returns from growth-focused private funds – specifically those in venture and growth equity (see Exhibit 5).

EXHIBIT 5: Returns from growth-focused funds have suffered during periods of rising rates

Median net internal rate of return, vintages 1985-2010

Source: Hamilton Lane Fund Investment Database. As of July 2021. For illustrative purposes only. Past performance is not indicative of future results.

Expansion of unicorn space to help drive investor access

Despite valid concerns about asset bubbles and inflation, private capital has solidified its role as the primary financing engine behind the ever-expanding universe of tech-driven companies that are transforming almost every industry. In short, late-stage venture capital and growth equity have become synonymous with the digital economy and are becoming more accessible to individual investors. To be sure, many unicorns, particularly those that have grown so large that they have become almost too big to be acquired, will eventually go public to provide an exit path for their institutional investors.

But the unrelenting pace of unicorn “births” and the continued evolution of the secondary market – with several major platforms competing to deliver scalable liquidity solutions16 – are irreversible and will likely expand access to unicorns to a much broader base of investors.

Nick is Co-Founder and one of the Managing Partners of iCapital Network, where he is Head of Portfolio Management. Nick spent 11 years at Veronis Suhler Stevenson (VSS), a middle market private equity firm where he was a Managing Director responsible for originating and structuring investment opportunities. At VSS, he specialized in the business information services sector and helped spearhead the firm’s investment strategy in the financial software and data sector, including its investment in Ipreo. Nick was previously an operating advisor to Atlas Advisors, an independent investment bank based in New York. He began his career as a financial journalist for The Boston Business Journal, was a reporter for The Star-Ledger, and a Senior Associate in the New Media Division of Newhouse Newspapers. He holds a BA in economics from Trinity College and FINRA Series 7, 79, and 63 licenses.

IMPORTANT INFORMATION

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as legal, tax or investment advice, a recommendation, or as an offer to sell, a solicitation of an offer to purchase or a recommendation of any interest in any fund or security offered by Institutional Capital Network, Inc. or its affiliates (together “iCapital Network”). Past performance is not indicative of future results. Alternative investments are complex, speculative investment vehicles and are not suitable for all investors. An investment in an alternative investment entails a high degree of risk and no assurance can be given that any alternative investment fund’s investment objectives will be achieved or that investors will receive a return of their capital. The information contained herein is subject to change and is also incomplete. This industry information and its importance is an opinion only and should not be relied upon as the only important information available. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed, and iCapital Network assumes no liability for the information provided.

Products offered by iCapital Network are typically private placements that are sold only to qualified clients of iCapital Network through transactions that are exempt from registration under the Securities Act of 1933 pursuant to Rule 506(b) of Regulation D promulgated thereunder (“Private Placements”). An investment in any product issued pursuant to a Private Placement, such as the funds described, entails a high degree of risk and no assurance can be given that any alternative investment fund’s investment objectives will be achieved or that investors will receive a return of their capital. Further, such investments are not subject to the same levels of regulatory scrutiny as publicly listed investments, and as a result, investors may have access to significantly less information than they can access with respect to publicly listed investments. Prospective investors should also note that investments in the products described involve long lock-ups and do not provide investors with liquidity.

Securities may be offered through iCapital Securities, LLC, a registered broker dealer, member of FINRA and SIPC and subsidiary of Institutional Capital Network, Inc. (d/b/a iCapital Network). These registrations and memberships in no way imply that the SEC, FINRA or SIPC have endorsed the entities, products or services discussed herein. iCapital and iCapital Network are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2021 Institutional Capital Network, Inc. All Rights Reserved.

1 Source: PitchBook, CapitalIQ. For illustrative purposes only. Past performance is not indicative of future results. Includes all tech IPOs backed by PE or VC firms in Q1 2021 for which data is publicly available (19 out of a total 34). Last Private Valuation is post-money valuation at last financing round involving equity issuance or last investment into the company. Excludes SPACs.

2 Source: Reuters, “Klarna funding round makes it Europe's most valuable startup at $31 billion,” March 1, 2021; Print21, “Canva valuation doubles in six months,” September 24, 2021; Fortune, “Insurance startup doubles valuation to $4 billion in 6 months, March 31, 2021.

3 Source: Forbes, “The Rise Of Secondaries In Tech,” September 16, 2021.

4 Source: Financial Times, “Staying private: the booming market for shares in the hottest start-ups,” February 27, 2021.

5 Source: PitchBook, CBInsights. For illustrative purposes only.

6 Source: PitchBook. For illustrative purposes only.

7 Source: PitchBook, “Why nontraditional investors are expected to continue their push into venture,” July 19, 2021.

8 Source: Goldman Sachs, “Hedge Funds and the Convergence of Private and Public Equity Investments,” September 2021.

9 Source: CBInsights. For illustrative purposes only.

10 Source: Jay Ritter, University of Florida. For illustrative purposes only.

11 Source: CBInsights. For illustrative purposes only.

12 Source: Jay Ritter, University of Florida. For illustrative purposes only.

13 Source: PitchBook. For illustrative purposes only.

14 CFA Institute: Enterprising Investor, “Dot-Com Redux: Is This Tech “Bubble” Different?” November 3, 2020.

15 Source: Hamilton Lane Fund Investment Database. As of July 2021. For illustrative purposes only. Past performance is not indicative of future results.

16 Notable examples include Nasdaq Private Market, Forge Global, Zanbato, and EquityZen.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All