Fiscal Arithmetic and the Global Inflation Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDebt-financed fiscal policy is driving much of today’s high inflation, but as pandemic-era measures fade, central banks will likely return to their key role in managing price levels.

What is driving the stubbornly high inflation evident in most advanced and emerging economies?

The complete answer may depend on where you live. The war in Ukraine pushed energy inflation higher in Europe. Weaker currencies have contributed to higher goods inflation in Japan and the Nordics. And soaring agriculture prices have raised food prices in many regions, particularly emerging markets.

Fiscal Policy and government debt: key inflationary pressures

While the sources of inflation vary, debt-financed fiscal policy is a major driver in many regions. Much of this policy was debated and enacted rapidly in 2020 to directly support households and businesses during the COVID-19 pandemic. As this government-financed funding flowed into the economy, demand for goods and services rose significantly in the following years (in many cases amid supply constraints), and price levels rose.

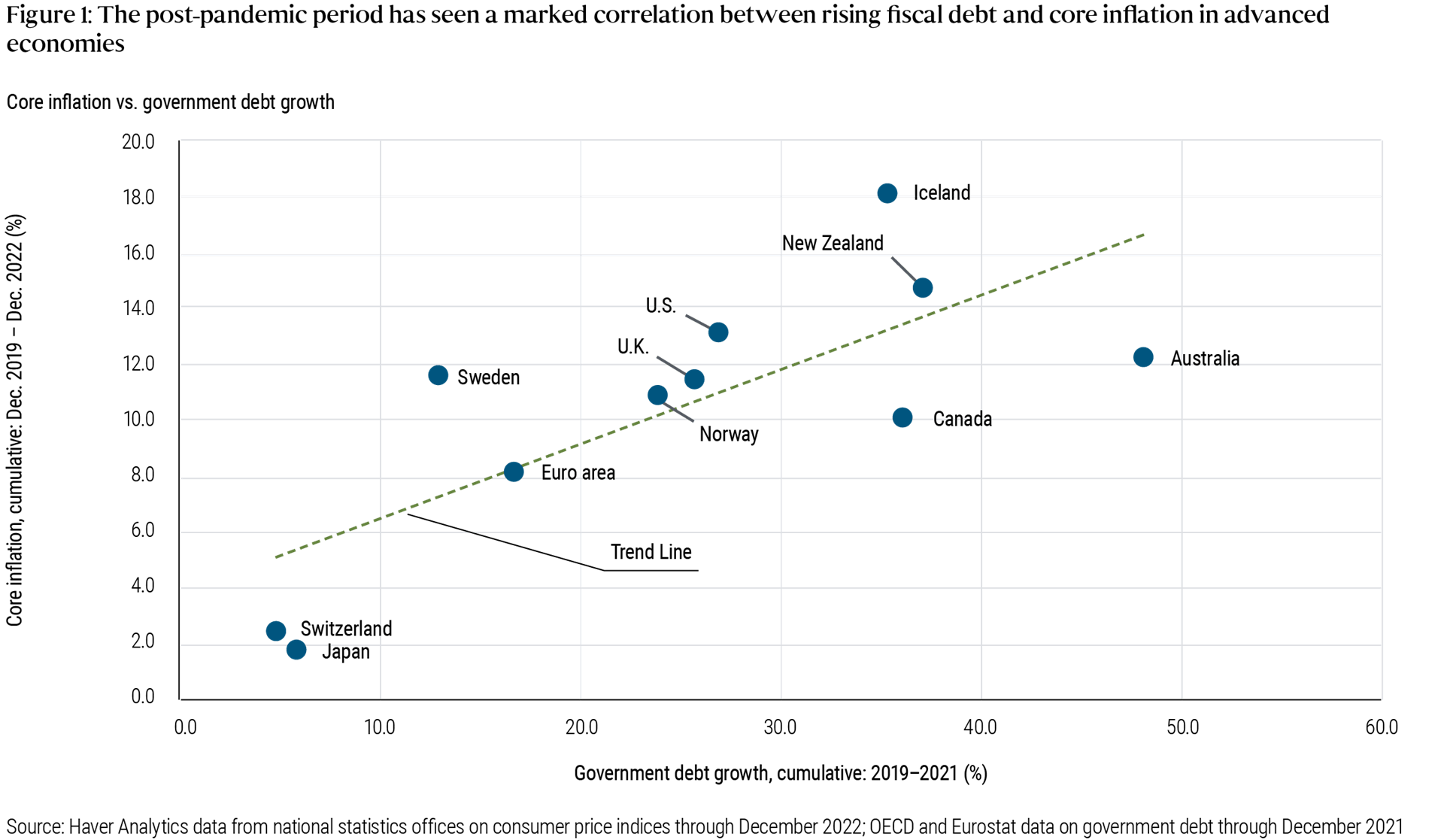

In advanced economies, there’s a significant positive relationship between core inflation and sovereign debt growth since the start of the pandemic (see Figure 1). Different fiscal approaches among these countries likely contributed to the wide variation in their inflation trajectories (we also note there’s typically a lag between enacting policy and seeing its impact in the inflation data). On the one end, New Zealand, the U.K., and the U.S. have seen double-digit core inflation and high government debt growth. On the other end, Japan and Switzerland have seen much smaller increases in both government debt and core prices. The euro area lies in between.

Historical perspective

In certain respects, the fiscal expansions and resulting price level increases this decade resemble the situation during and after the two world wars, as well as the 1918 influenza pandemic. Massive spending especially in wartime drove government debt levels to dramatic highs in many countries – in the U.S., for example, the debt-to-GDP ratio reached 106% in 1946, according to the Congressional Budget Office (CBO). These levels eventually decreased amid a multi-decade postwar economic expansion – including periods of significant inflation.

In 2008, the global financial crisis (GFC) triggered fiscal support to bolster a struggling economic and financial system. But much of this government financing was directed to businesses and (we would argue) came with expectations of future tax hikes or spending cuts to help improve the overall fiscal trajectory.

Today, the global economy is gradually exiting a period of extraordinary fiscal policy interventions, but the pandemic-related deficits are larger than GFC-era deficits and are directed to households along with businesses. And current political sentiment in many countries suggests less appetite to limit the government balance sheet via increased taxes or curtailed spending – suggesting debt levels could keep climbing. This could limit fiscal capacity to address future crises. In the U.S., for example, the debt-to-GDP ratio is approaching its World War II high, and the CBO sees it continuing to rise over the coming decades. (For details, please read PIMCO’s latest Secular Outlook, “The Aftershock Economy.”)

Policy, debt, and Inflation: the changing arithmetic

Central banks responded swiftly to the pandemic-driven economic and market crisis, slashing interest rates and launching quantitative easing (QE) programs that purchased interest-bearing government bonds paid for with new base money. These monetary actions complemented fiscal expansion, and in retrospect, highly accommodative fiscal and monetary stimulus (enacted by policymakers facing a global emergency) likely led to imbalances relative to the post-pandemic aggregate supply of goods and services.

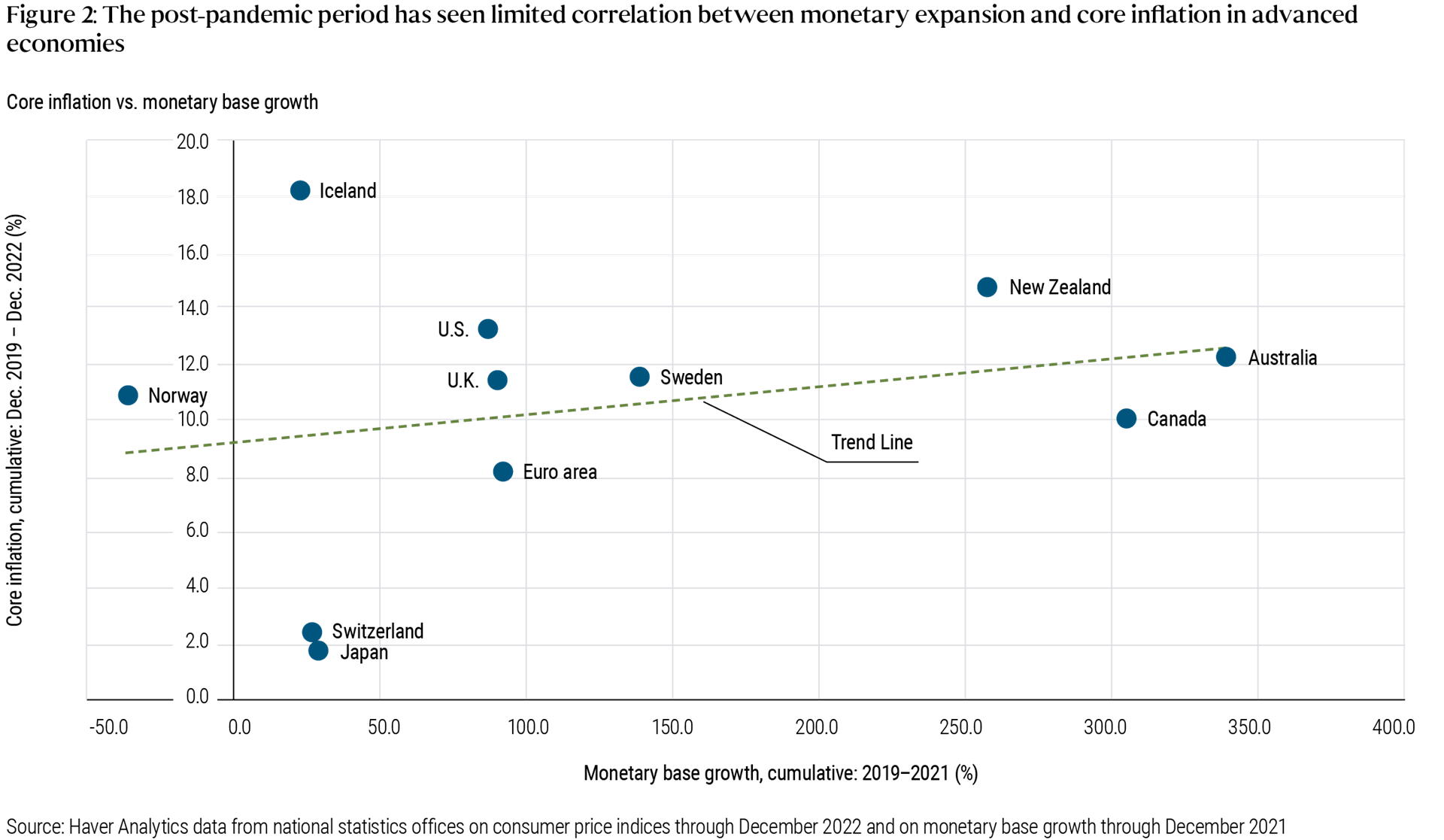

In our view, however, central bank policy – especially QE – likely played more of a supporting role than a leading role in causing spikes in national price levels. Looking across advanced economies, there’s a much weaker relationship between core inflation and growth in the monetary base since the start of the pandemic (see Figure 2) than we observe with growth in government debt, shown in the previous figure.

What explains this more limited apparent contribution to inflation from an expanded monetary base?

At a high level, while fiscal policy determines the number of government liabilities, monetary policy merely changes its composition. Unlike government deficits, quantitative easing does not place net new assets in private hands but swaps one type of asset – fixed-rate interest-bearing government bonds – for another: central bank reserves that pay a floating interest rate that generally hews very close to the return on short-term sovereign assets, such as U.S. Treasury bills.

This change in the composition of the debt on the government’s overall balance sheet (i.e., both the treasury and the central bank) is important: Central banks now pay interest on reserve balances. This fundamentally changes the relevant “fiscal arithmetic.” QE does not extinguish debt, nor does it zero out the coupons on that debt: The treasury, via its claim on central bank profits, is still on the hook for the interest payments on the newly created floating-rate reserves. QE has in fact shortened the overall maturity profile of government debt by swapping long-maturity fixed-rate bonds for overnight, floating-rate reserves. And as central banks in the past year-plus have raised interest rates dramatically in an effort to tame inflation, central bank profits on those reserves rapidly eroded, increasing the net cost for the government. Here’s how: Either the central bank remits less in profits to the treasury over time, or (at the Bank of England and the Swedish Riksbank) the central bank crystallizes some of those net present value losses by actively selling bonds in the secondary market, effectively destroying reserves.

In summary, in the current regime where governments essentially are paying interest on reserves (and at a high rate relative to post-GFC recent history), the fiscal authority can no longer enjoy the seeming “free lunch” provided by a central bank that prints zero-interest money to pay for government bonds.

Implications and outlook

So what is next? The fiscal expansions delivered this decade will likely lead to price levels adjusting permanently higher. But this is not the same thing as permanently higher inflation: Our base case is that as temporary pandemic-related deficits gradually normalize, inflation is likely to diminish – and today’s restrictive monetary policies aim to accelerate this process. And unlike in the 1970s, monetary policy credibility appears intact, with medium-term inflation expectations still anchored around central bank targets.

We also recognize a range of potential inflationary pressures over the secular horizon (arising from policy, geopolitics, labor markets, etc.) that pose risks to our base case. Persistently elevated inflation could lead to inflation expectations adapting higher, a risk that central banks are seeking to mitigate via decisive monetary policies.

Although the pandemic-related fiscal deficits were temporary, it will take time for their full effect to filter through to activity and inflation. Prices and wages tend to be sticky and firms are generally slow to adjust their prices. The fiscal deficits have left the private sector with a large savings surplus – and households typically don’t spend all of their excess savings immediately but instead smooth their consumption over time. As a result, although the initial fiscal shock was temporary, we expect it will take time for prices to adjust to the permanently higher level required to offset the fiscal shock.

Once the price level adjustments from the fiscal shocks are absorbed (meaning businesses, policymakers, and consumers have largely accepted and planned for these permanently higher prices), central banks will likely return to their traditional role in directing the future inflation path. We expect them to keep winding down their QE programs, and perhaps a pervasive “QE fatigue” will set in that raises questions about central banks’ ability and appetite for extraordinary policy in the next crisis.

Looking beyond QE, we still believe central banks plan to do whatever it takes to keep inflation expectations anchored at their inflation targets, but those targeting 2% may tolerate “2-point-something” inflation for a while as part of an “opportunistic disinflation” strategy – i.e., they expect a shortfall in aggregate demand during a future recession to return inflation to target from above.

The pandemic serves as an important reminder that it takes two to tango, and that price stability requires not just prudent monetary policy but appropriate fiscal backing too. Higher interest rates have worsened fiscal trajectories, and in the long run, governments may need to adjust future tax and spending plans to avoid a situation in which fiscal dynamics return to the driver’s seat of shaping inflation.

DISCLOSURES

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low-interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk including market, political, regulatory, and natural conditions, and may not be appropriate for all investors. Sovereign securities are generally backed by the issuing government, obligations of U.S. Government agencies and authorities are supported by varying degrees but are generally not backed by the full faith of the U.S. Government; portfolios that invest in such securities are not guaranteed and will fluctuate in value.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries, and institutional investors. Individual investors should contact their own financial professionals to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2023, PIMCO.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All